As Jay Powell faced reporters on Wednesday following the US Federal Reserve’s first policy meeting of 2024, his mood was confident.

Hailing “six months of good inflation” and predicting more to come, the Fed chair said: “Let’s be honest: this is a good economy.”

Maybe a little too good. On Friday, markets were stunned by a Bureau of Labor Statistics release that showed the US economy added 353,000 jobs in January — almost double what was expected.

A March cut to interest rates — already described as unlikely by Powell — was instantly ruled out on Wall Street as a result of the blowout employment data.

Central bankers around the world had begun preparing for rate cuts on the back of steadily weakening inflation. But as the US jobs numbers demonstrate, hot labour markets are the biggest potential barrier to them hitting their 2 per cent inflation goals.

Eswar Prasad, an economist at Cornell University, says Friday’s data made declaring victory against inflation “a much more fraught” decision for central banks. “The reality is that, with these pressures, it’s going to be very difficult to keep inflation contained unless productivity growth remains strong.”

This is not to deny how dramatic the improvements in the inflation picture have been. A year ago, the Fed and its counterparts were in the midst of a brutal series of interest-rate increases that some feared would drive economies into recession.

Powell warned in February 2023 that officials still had a “long way to go” as they attempted to quell the “significant hardship” imposed by the highest inflation in 40 years. Since then, inflation has tumbled towards the Fed’s 2 per cent target across an array of different gauges.

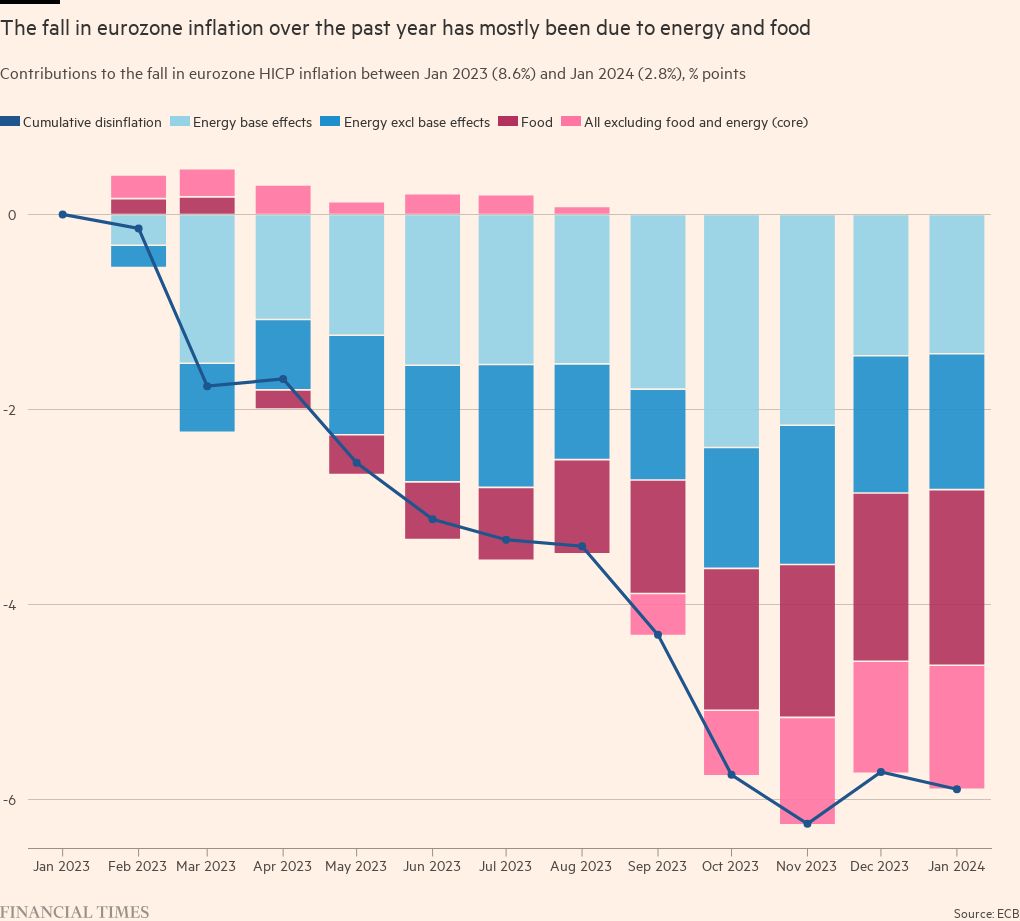

In Frankfurt, Christine Lagarde, president of the European Central Bank, on January 25 sounded similarly positive about the eurozone picture as she declared the “disinflation process” to be at work; headline price growth in the bloc is now 2.8 per cent, not far from the ECB’s 2 per cent target.

Andrew Bailey, governor of the Bank of England, told reporters in London last Thursday that he was seeing “good news on inflation” after price growth in the UK more halved in the space of six months, to 4 per cent.

The speed of the retreat in inflation over recent months has wrongfooted many rate-setters. Consumer price growth across advanced economies has dropped from more than 7 per cent in 2022 to 4.6 per cent in 2023, according to the IMF.

Forecasts from the fund last week pointed to a further decline to just 2.6 per cent this year — sharply below its previous 3 per cent prediction — with four-fifths of the economies it tracks set to experience lower annual headline and core inflation in 2024.

Mahmood Pradhan, head of global macroeconomics at the Amundi Investment Institute, argues the trend in inflation is now “decisively down and it is just a question of time before we see substantial rate cuts this year”.

He added: “Central bankers out of caution want to wait a bit longer, but I can see the Fed, ECB and Bank of England all cutting in the middle of this year.”

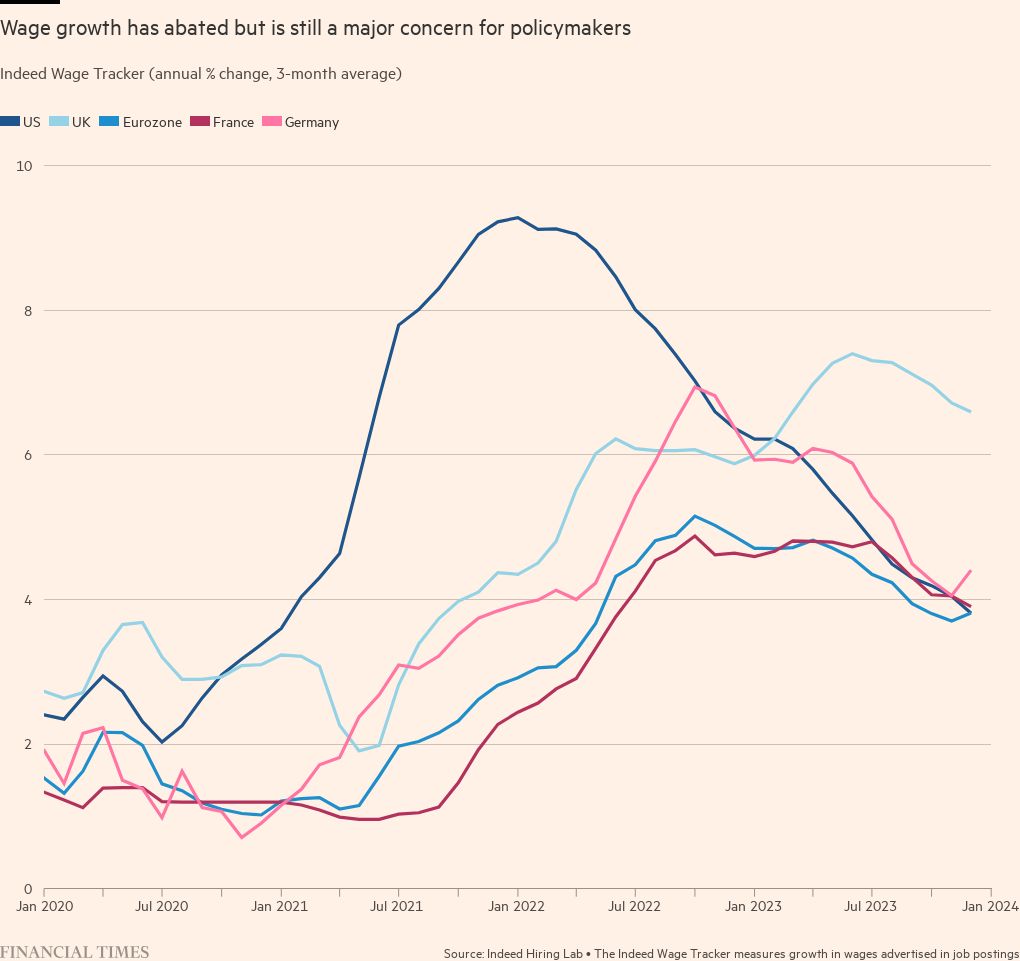

Continued progress in this disinflation story will hinge heavily on the fate of labour markets. While the initial declines in inflation were driven by external factors, progress now depends on the more difficult task of depressing domestically generated price growth. That will be harder if jobs and wage growth stay too robust.

Economists say squeezing out the last vestiges of excess price growth might require policymakers to maintain persistently tough policy that further depresses demand.

It all speaks to a concern that has been haunting central bankers for months: will the “last mile” of the effort to drive price growth down to their 2 per cent targets prove to be the most difficult? If it does, central banks will have to be particularly patient before cutting rates.

Among the major central banks, officials at the Fed have consistently appeared the least concerned about the difficulties of getting through that final stage of the inflation-fighting journey.

Powell himself sounded sceptical about the notion in December. “Inflation keeps coming down,” he said. “It’s so far, so good — although we kind of assume that it will get harder from here. But so far, it hasn’t.”

The Fed’s confidence owes something to both the nature of US inflation and the pace of its descent. While the US was hard hit by Covid-related disruption to supply chains, it did not see the sort of surge in energy prices that drove up prices across Europe following Russia’s invasion of Ukraine. As a result, US inflation never reached double digits, peaking at 9.1 per cent in 2022.

The nature of its inflation shock also made its reversal more swift. On some measures — including a six-month gauge of core personal consumption expenditures, a measure that Fed officials say offers the best signal of underlying price pressures — inflation is now under 2 per cent.

But worries about an overheating jobs market re-emerged with a vengeance on Friday. In addition to the blowout January numbers, figures for December and November were revised upwards and average hourly earnings increased by 4.5 per cent, according to the labour bureau.

Diane Swonk, US chief economist at KPMG, says unusually low levels of lay-offs and a drop in hours worked suggested that some of the job market’s strength was due to employers “hoarding” labour. Those who struggled to hire workers after Covid lockdowns ended did not want to find themselves in the same position when demand picked up, she explains.

“However, that is still a lot more paychecks to start the year than usual,” she adds. “When taken with the upward revisions to the previous two months and the hotter than expected wage growth, that suggests the labour market may be re-accelerating.”

3.3%Growth rate of the US economy in the fourth quarter

Curt Covington, a senior director at AgAmerica Lending, a credit provider to farmers, says wage pressures remain high in states such as California, where the statewide minimum wage has risen by another 50 cents to $16 an hour this year — up from $12 an hour when the pandemic struck.

“The [production of] certain commodities is very labour driven, speciality crops in particular,” says Covington. “You don’t see much of the increase in labour costs on Midwest crops like corn and beans, but when you get into speciality crops such as some fruits and vegetables, the labour cost has gone up significantly.”

Some economists worry that the deflation in goods prices caused by the easing of supply chain pressures will soon come to an end, making the job of suppressing overall price growth yet harder. This is especially relevant given strong US demand, with the economy expanding at an annualised rate of 3.3 per cent in the fourth quarter.

Pradhan argued that stubbornly high wage growth represents the main question mark for central bankers as they prepare for the “last mile” of the disinflation journey.

But he remains sanguine. US wage growth should prove benign because it is supported by strong productivity growth, he argues. In Europe, weak economic demand should lead to “continued moderation”.

Others note that the situation facing the Fed is very different from the dreaded wage-price spiral seen during the 1970s and early 1980s. “This spell of inflation hasn’t primarily been about demand. It’s been about disruptions to supply chains, labour markets, and spending caused by Covid,” says Claudia Sahm, a former Fed economist and founder of Sahm Consulting.

“Productivity continues to look really good,” she adds. “The US economy can tolerate higher wages.”

At the European Central Bank, rate-setters have made it clear that their key focus in the coming months will be on wage settlements and whether they are compatible with the 2 per cent inflation target.

Back in December, German central bank boss Joachim Nagel warned inflation was “a stubborn, greedy beast” and that bringing it down would require “gritting your teeth and not letting up”. More recently Nagel has sounded somewhat more optimistic, telling an event in Berlin last week that the beast had been “tamed”.

But Lagarde has been warning it is “premature” to even discuss possible interest rate cuts at this stage — critically because of rising wages. The worry at the ECB and elsewhere is that workers will demand big pay rises to restore the purchasing power they lost during the initial spikes in prices. As that increased spending power finds its way into the economy, it triggers a fresh surge in prices.

Eurozone wages rose over 5 per cent last year, close to the annual inflation rate. While recent data shows wage pressure is “already declining”, Lagarde said the ECB still wants to be sure that higher labour costs are “sufficiently absorbed” by companies choosing to reduce their profit margins rather than raising their prices.

Eurozone inflation has fallen steadily from a record 10.6 per cent in late 2022 to below 3 per cent, but Lagarde has expressed concern that one area where prices seem stickier is the services sector, where labour makes up a large share of total costs. Eurozone services prices rose 4 per cent in the year to January for the third consecutive month.

As in the US, those worries are underpinned by the unexpected resilience of the region’s labour market. Eurozone unemployment remained at a record low of 6.4 per cent in December and many companies — particularly in the services sector — are still complaining that labour shortages are the main constraint on production.

6.4%Eurozone unemployment in December, a record low

But as in the US, optimistic economists dismiss the idea that Europe is on the cusp of a wage-price spiral, pointing out that the automatic “indexation” of pay to prices has largely disappeared except for in a few countries, such as Belgium.

A key difference with previous periods of high inflation is that wages seem to be following prices rather than leading them, according to Sven Jari Stehn, chief European economist at Goldman Sachs. “It is natural that when you have a supply shock which pushes up prices, it has a lagging impact on wages, but the risk here isn’t that great,” he says.

Even though labour markets are tight, it may be hard for many companies to pass on higher wage costs because — unlike the US — underlying economies are stagnating. So although unions last week demanded a pay rise of 6 to 7 per cent for German chemical workers, this seems unlikely to trigger a price surge in a sector that suffered an 11 per cent fall in production last year.

“A one-off rise in wages is very different from a spiral,” says Marcel Fratzscher, a former ECB official now running the German Institute for Economic Research in Berlin. “The ECB should look through a one-off adjustment.”

In private, ECB rate-setters say they feeling confident. “We see indicators moving in the right direction,” says one of its governing council members. “Monetary policy is working. Inflation is falling.”

Officials at the Bank of England are not sounding quite that assured — or at least not yet. While Bailey finally opened the door to lower interest rates last week after his policy committee kept rates pegged at 5.25 per cent, the BoE governor appeared to tip-toe around the topic of rate cuts, as if mentioning the idea out loud would prompt unwarranted relief in markets.

While the UK labour market had cooled, it remains “tight by historical standards”, the bank warned, as it continued to highlight indicators of persistent price pressures including wage growth and services inflation. A survey by BoE regional agents showed that pay settlements will fall to an average of 5.4 per cent this year, a figure that is not far below last year’s 6 per cent.

Worries about other “upside risks” to inflation have added to central bankers’ caution. One obvious one stems from the continuing conflicts in the Middle East; the disruption to shipping from attacks by Houthi rebels on vessels in the Red Sea is widely cited as a factor that could push inflation higher than expected. Europe appears particularly exposed given the importance of the trade route for imports from China.

However, rate-setters including Lagarde of the ECB have tended to downplay that issue, pointing out that shipping made up only 1.5 per cent of the total cost of goods. Economists seem to agree. Goldman has estimated the rise in container shipping rates will add only 0.1 percentage points to global inflation.

Even the ECB’s new artificial intelligence-powered model for forecasting inflation shows it is set to fall much closer to 2 per cent by this summer than the central bank forecast only a few weeks ago.

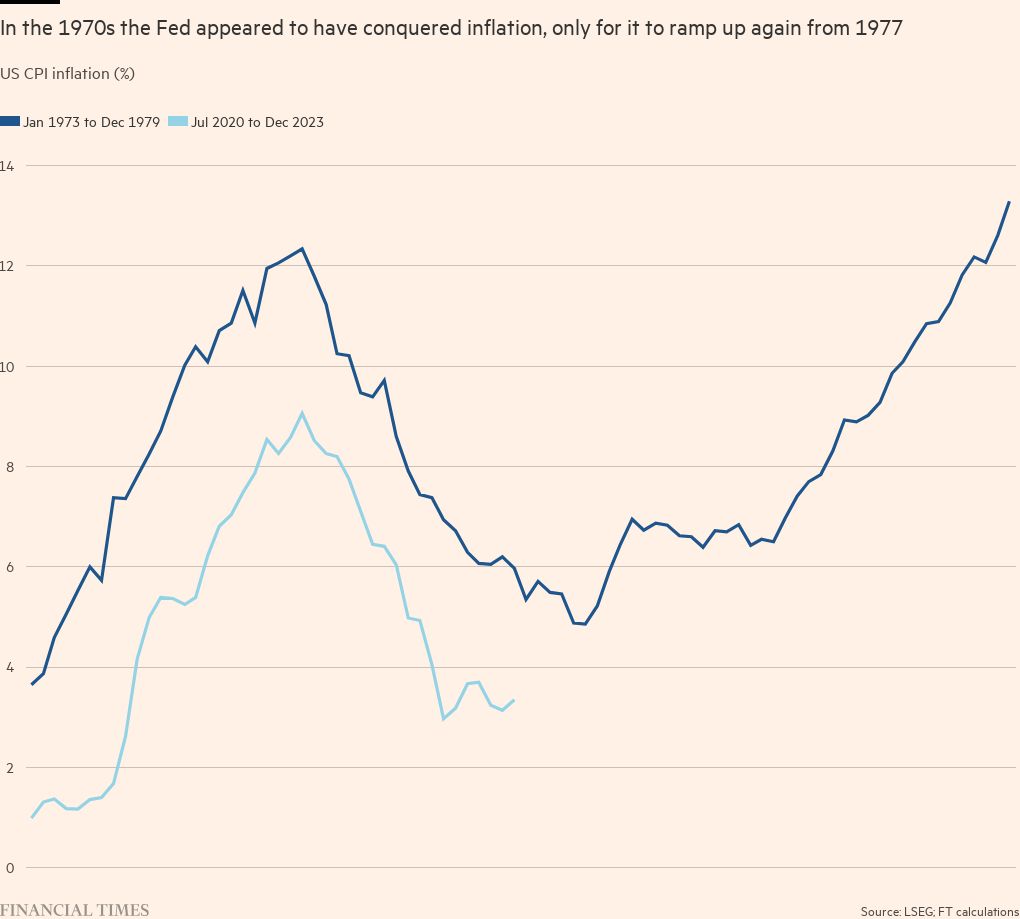

Nevertheless, banks will probably remain wary of jumping too soon and then being forced to abruptly reverse course if inflation takes flight again. The IMF itself warned last year that there is a prodigiously rich history of central banks prematurely declaring victory over inflation.

That includes the US itself, where Federal Reserve chair Arthur Burns was accused of being far too relaxed about price growth in the early 1970s — failing to get to grips with a scourge that plagued the US economy for an entire decade.

The rapid reversal of supply-driven inflation juxtaposed with stubborn domestic price growth leaves central bankers facing a delicate balancing act, says Krishna Guha, a former Federal Reserve official who is now vice-chair of investment bank Evercore-ISI.

“You want to make sure that you don’t jeopardise the soft landing by keeping policy too tight for too long,” he says. “The job isn’t quite done yet, but they are reasonably close — in some cases very close — to having pulled this off.”

Sahm is more confident, saying the market has “had months of good data on prices.”

“This [January] jobs report doesn’t change the fact that it’s going to turn out to be the first mile that was the toughest, not the last.”

Data visualisation by Keith Fray

{kind=link}