US banks are becoming increasingly worried about falling commercial property valuations and the risk they pose to lenders’ balance sheets, senior executives said this week.

Office valuations in particular have been pummelled by rising interest rates and many employees’ preference for working from home since the coronavirus pandemic.

However, financial executives sought to reassure investors that they did not foresee significant systemic risk because holdings are broadly distributed among banks and other institutions.

“What happens with commercial real estate, particularly offices” was State Street’s biggest concern, the US custody bank’s chief executive Ron O’Hanley said this week. Not all properties had been hit equally, he added: “Class A is holding up. Rents may be declining but they are not in trouble. Class B and C absolutely are.”

“The question we all have is whether contagion will spread from the office sector,” said Bryan McDonnell, head of PGIM’s real estate debt business, which has $122bn under management. “If you get to a confidence issue then, all of a sudden, people might put all commercial real estate in the same bucket.”

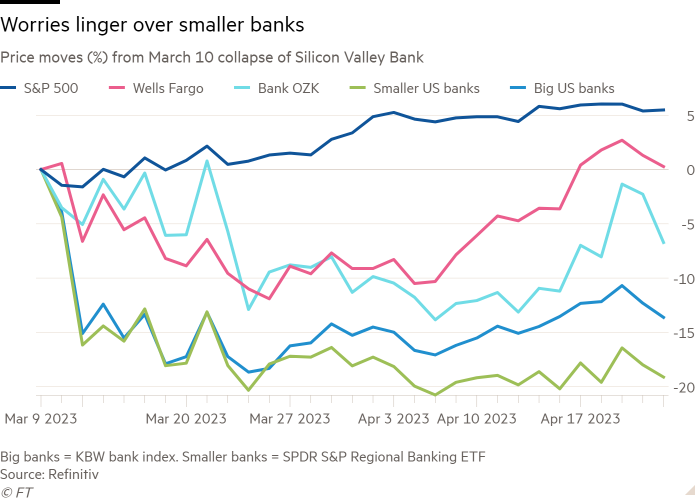

There are signs of the rising stresses in first-quarter bank earnings. Last week Wells Fargo reported that its non-performing commercial real estate loans had jumped nearly 50 per cent since December to $1.5bn. Morgan Stanley cited commercial property and a deteriorating economic outlook as reasons for a sharp rise in its provisioning compared with last year.

“In my view we are not in a banking crisis, but we have had, and may still have, a crisis among some banks,” chief executive James Gorman told analysts on a call.

Commercial real estate loans account for about 40 per cent of smaller banks’ total lending, against about 13 per cent of the books of the biggest lenders.

Arkansas-headquartered Bank OZK, which is heavily exposed to the sector, reported on Friday that it had raised loan provisions by 10 per cent in the first quarter. At $36mn, that marked a tenfold increase over the levels of a year ago.

Almost a third of the $4.5tn in commercial real estate debt comes due before the end of 2025, according to Morgan Stanley analysts, who described that as “front-loaded”.

This week Christopher Ailman, chief investment officer of the $306bn California State Teachers’ Retirement System, told the Financial Times he estimated office values had fallen by about 20 per cent and that he was bracing for steep losses on the fund’s $52bn real estate portfolio.

Investor jitters are increasingly widespread, with almost half those surveyed this month by Bank of America identifying commercial real estate as the most likely source of a systemic credit event.

The sector is causing similar concerns beyond the US, with a top official at the IMF this month describing commercial property as “a point of focus”.

The multilateral lender’s latest financial stability report warned how a toxic combination of falling property values, tighter financial conditions and illiquid markets could result in borrowers struggling to refinance an ever-increasing stock of maturing loans, leading to sharply higher default rates.

Property group Brookfield added to a growing number of high-profile defaults this week by walking away from $161mn of loans tied to a group of mostly suburban office buildings near Washington. In February it handed back the keys to two prime Los Angeles office towers.

Blackstone and Pimco have in recent months also given up on some of their office investments rather than continue with lossmaking bets.

“If you have maturing debt, you can’t carry the existing debt load and you’re not willing to put more money in, then it’s foreclosure,” said Tony Natsis, head of the real estate group at law firm Allen Matkins.

He added, however, that lenders would prefer to modify existing loans: “They’re asking themselves ‘do I really want to take this back in a bad market?’”

In the first three months of this year, office-related deals dropped to their lowest level in more than a decade, according to data from MSCI Real Assets.

Real estate specialists have been at pains to point out that commercial property is a slow-moving, lumpy market and that investors should not expect quick resolutions to troubled situations — or for those difficulties to pile up rapidly as lenders and borrowers try to work through potential solutions.

“The positive here is that large portions of commercial real estate are still performing quite well, like logistics, hotels, rental housing and data centres,” Jonathan Gray, president of Blackstone, the world’s largest property investor with $332bn of real estate assets, said this week.

Gray made his name via Blackstone’s property arm and emphasised how broadly real estate investments were held.

“Commercial real estate is broadly distributed amongst big banks, small banks, insurance companies, government agencies, securitisations and mortgage Reits,” he added. “I don’t think it’s the kind of systemic issue people are saying it is.”

Reporting by Jennifer Hughes, Brooke Masters, Harriet Clarfelt, Madison Darbyshire, Antoine Gara and Stephen Gandel in New York and Colby Smith in Washington

{kind=link}