Introduction: UK retail sales rebound

Good morning, and welcome to our rolling coverage of business, the financial markets and the economy.

With Britain now in a technical recession, economic data will be closely scrutinised for signs that the downturn could be ending.

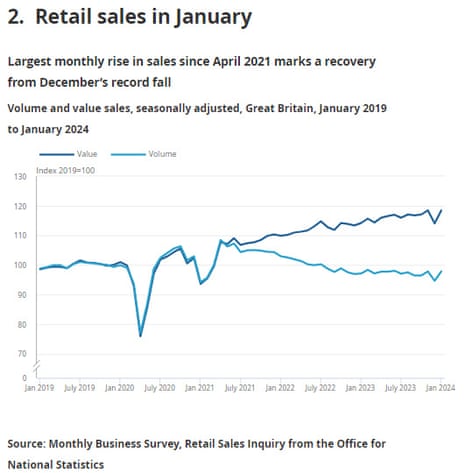

And the latest retail sales figures, just released, show that retail sales across Great Britain grew at the fastest rate since April 2021 last month, as consumers returned to the shops after a pre-Christmas slump.

Retail sales volume rebounded by 3.4% in January, the Office for National Statistics reports. That follows a record 3.3% tumble in retail spending in December, which flashed warning signs over the economy a month ago.

Retail sales volumes (quantity bought) rebounded 3.4% in January 2024, following a record fall of 3.3% in December 2023.

This was the largest monthly rise since April 2021 and returned volumes to November 2023 levels.

â¡ï¸ https://t.co/ipWNHoU3do pic.twitter.com/4d1LyKkEoP

— Office for National Statistics (ONS) (@ONS) February 16, 2024

It could be a sign that the UK economy is picking up â as Bank of England governor Andrew Bailey has suggested â after shrinking in the second half of last year.

The ONS reports that sales volumes in all subsectors, except clothing stores, increased in January.

Food stores such as supermarkets contributing most to the increase, with food stores sales volumes rising by 3.4% over the month.

The ONS says some of the fall in December was because of consumers purchasing Christmas gifts earlier, during the November Black Friday discounts.

But separate ONS polling did find that almost half of adults had expected to spend less on Christmas shopping because of the rising cost of living.

Heather Bovill, deputy director for surveys and economic indicators at the ONS, says:

âAfter a very weak December, retail sales rebounded in January with the largest monthly rise since April 2021. This means that overall sales have now recovered to pre-December levels, although if we look at the broader picture, they are still below where they were pre-pandemic.

âSales increased across nearly all retail sectors, and it was a particularly strong month for supermarkets. Household goods stores, sports shops and department store retailers were amongst those reporting robust trading due to January sales promotions. A fall in prices at the pump also meant a solid month for fuel sales.

âClothing shops were the only area not to see growth this month.â

The agenda

-

7am GMT: UK retail sales for January

-

10.30am GMT: Bank of Russiaâs interest rate decision

-

1.30pm GMT: US PPI index of producer price inflation for January

-

1.30pm GMT: US building permits and housing starts data for January

Key events

Closing post

Time to wrap up after a busy week, in which UK wage growth slowed, inflation remained steady, and the economy fell into recession.

Hereâs today main stories so far:

US consumer confidence has inched a little higher this month.

The University of Michiganâs consumer morale index of consumer sentiment has risen to 79.6, up from 79.0, lifted by a rise in consumer expectations.

Surveys of Consumers director Joanne Hsu explains:

Consumer sentiment was essentially unchanged from January, rising 0.6 index points this month and solidifying the large gains from the past two months.

The fact that sentiment lost no ground this month suggests that consumers continue to feel more assured about the economy, confirming the considerable improvements in December and January across various aspects of the economy. Consumers continued to express confidence that the slowdown in inflation and strength in labor markets would continue.

Five-year expectations for business conditions rose 5% to its highest reading since December 2020. Sentiment is currently about 30% above November 2023 and about 6% below its historical average since monthly data collection began in 1978.

Goldman Sachs has cut its forecast for European gas prices this year, citing persistently mild weather.

In a new research note, Goldman warn that Europe has not yet solved its energy crisis â it will take one more winter until the risk of extreme gas prices re-emerging has ebbed.

But while increased LNG supply has not yet fully making up for lost Russian imports, that will change from 2025, Goldman says, tilting the markest into oversupply.

The jump in US wholesale inflation last month shows that cooling the pace of prices rises all the way down to target is tricky for central bankers.

Ken Tjonasam, portfolio strategist at fund management firm Global X ,says:

This PPI print further highlights that getting inflation back to the Fedâs 2% target isnât just a walk in the park; itâs the last mile thatâs the toughest.

For Chair Powell and the Fed, this means recalibrating their lens on the economic landscape. The narrative of easing into a rate cut has just hit a snag.â

The drop in the pound following the hotter-than-expected US PPI data is helping to support stocks in London.

The FTSE 100 index is having a fine day, up 110 points or 1.45% at 7707 points. Mining stocks, and Asis-focused financial services group Prudential, are among the top risers, reflecting hopes that China might take fresh measure to support its economy.

US producer price inflation hotter than forecast

Just in: US producers raised their prices at a faster rate than forecast last month, dampening hopes that inflationary pressures were ebbing.

Producer prices rose by 0.3% in January, following a 0.1% drop in the PPI index in December.

This was driven by a 0.6% rise in prices for services, while goods prices fell 0.2%.

On an annual basis, prices were 0.9% higher than a year ago, higher than the 0.6% expected but a little lower than Decemberâs 1%.

Worryingly, core PPI inflation (stripping out foods, energy, and trade services) increased by 2.6% year-on-year.

BREAKING: January PPI inflation hits 0.9%, above expectations of 0.6%.

Core PPI inflation JUMPED to 2.0%, above expectations of 1.6%.

Both CPI and PPI inflation have come in above expectations in January.

Disinflation seems to be slowing.

Can the Fed really pivot here?

— The Kobeissi Letter (@KobeissiLetter) February 16, 2024

This has lifted the dollar, with the pound down half a cent at $1.255.

Bond yields are also rising, as investors dial back hopes of early interest rate cuts.

Ex-Goldman analyst jailed for 22 months for insider trading

A former Goldman Sachs analyst has been jailed for 22 months after being convicted of insider trading and fraud.

Mohammed Zina, 35, was found guilty by a London jury yesterday. He had used information obtained at Goldman Sachs to trade in stocks including semiconductor designer Arm, ahead of its takeover by SoftBank, and pub company Punch Taverns.

Zina had been employed by Goldman Sachs International in its conflicts resolution group in London.

At Southwark Crown Court, Judge Tony Baumgartner told Zina he had thrown away a promising banking career, saying:

âYou betrayed the trust of your employer, as well as cheated honest investors in the shares you traded using inside information you saw at work.

âWhat you did strikes at the very heart of our financial markets and the trust and confidence the public places in them.â

A Goldman Sachs spokesperson said:

âMohammed Zina betrayed the trust we placed in him and his misuse of client information was in direct contradiction of our values. We have zero tolerance for this conduct.â

Zina had made a profit of about £140,000 from the insider trading, financed with loans obtained from Tesco Bank that were meant for home improvements.

As has become traditional, the latest UK retail sales figures show the impact of inflation.

While sales volumes rose by 3.4% in January, shoppers actually spent 3.9% more than in December â meaning they spent more for less.

In the City, shares in NatWest have jumped by over 6% this morning after the bank reported a 20% jump in profits for last year.

They have hit 229.7p, the highest since last October.

Fran Boait, co-executive director at campaign group Positive Money, argues that the popularity of NatWestâs shares today shows the government shouldnât be looking to sell the taxpayerâs stake.

Boait says:

âNatWest represents an enormous missed opportunity by this government.

âContinuing to sell off the publicâs shares for a huge loss when the bank is finally posting stronger results perfectly illustrates the short-termism that has come to define our government.

âThe government could also have used its majority stake to ensure NatWest passes higher interest rates onto depositors, which wouldâve pressured other banks to do the same.â

The government acquired its NatWest shares at a price of 500p each, when it bailed out then-Royal Bank of Scotland after the financial crisis.

NatWestâs shares have not traded over 500p since 2010, so the chances of the public making a profit anytime soon seems very thinâ¦.

â¦Especially as the bank has forecast a drop in earnings this year (see 7.38am), with falling interest rates expected to hit profitability.

Energy price cap predicted to fall 15% in April

The cap on UK energy bills is set to fall by 15% when it is next set, analysts at Cornwall Insight say.

Cornwall estimates that the price cap will drop to £1,635 per annum, for a typical household, in April.

This is a fall of 15% (£293) from the current price cap which was set at £1,928 per year from January, and should bring some relief to households struggling to pay their bills.

The cap is set four times a year by the regulator, Ofgem, and sets the maximum price per unit of energy that suppliers can charge (there is no cap on the maximum bill).

Cornwall also expect the cap will fall again in July, followed by a small rise in October.

Dr Craig Lowrey, principal consultant at Cornwall Insight, says:

âForecasts show energy bills returning to their lowest levels in over two years, providing a much-needed respite for a nation struggling with a cost of living crisis.

âFairly healthy gas supply across the Atlantic, coupled with high storage levels in Europe, are helping to keep bills down. But we mustnât get too complacent. Our energy system is still walking a tightrope, and we cannot be sure another political or economic crisis wonât send bills straight back up.

âEven with the drop, prices will remain a struggle for many. We need to remember, bills remain hundreds of pounds above pre-pandemic levels, and if we donât speed up the switch to sustainable energy and cut down on volatile imports, they are likely to stay that way.â

Ofgem reveals new level of energy price cap a week today, taking effect from April.

Cornwall Insight says it’s forecasting cap will be £1,635 (average annual bill) down by 15% – followed by another drop of ~10% in July.

Election-timing-watchers can draw their own conclusions…

— Hugo Gye (@HugoGye) February 16, 2024

Russian central bank holds rates at 16%

Newsflash: Russiaâs central bank has held interest rates at 16%, after five hikes in a row since last summer.

The Bank of Russia says:

Current inflationary pressures have eased compared with the autumn months but remain high. Domestic demand is still outstripping the capabilities to expand the production of goods and services.

A judgement on the sustainable nature of emerging disinflationary trends would be premature. The Bank of Russiaâs monetary policy is set to solidify disinflation processes unfolding in the national economy.

Russiaâs interest rates have been volatile since the full-scale invasion of Ukraine.

The Bank of Russia doubled rates to 20% in March 2022 to support the rouble, but then lowered them through 2022 to 7.5%, before starting to hike in summer 2023:

Noble Francis, economics director at the Construction Products Association, flags that insolvencies among building firms climbed last year:

4,378 UK construction firms went out of business in the year to December 2023. This is 5.1% higher than a year ago & 37.9% higher than in the year to January 2020, pre-pandemic, according to this morning’s Government Insolvency Service data. (1/n)#ukconstruction #ukhousing pic.twitter.com/NzvsHqYMJD

— Noble Francis (@NobleFrancis) February 16, 2024

… UK construction insolvencies were already at their highest levels since the financial crisis at the end of 2022 & have continued to gradually rise since then & UK construction insolvencies are expected to continue to rise further in 2024 H1. (3/n)#ukconstruction #ukhousing pic.twitter.com/d51cXXudqH

— Noble Francis (@NobleFrancis) February 16, 2024

The sharp rise in UK construction insolvencies in the last 2 years was partly due to double-digit falls in activity in the 2 largest construction sectors, private house building & repair, maintenance & improvement (rm&i), plus… (4/n) pic.twitter.com/GqVJFYJ93Z

— Noble Francis (@NobleFrancis) February 16, 2024

… UK construction firm issues have been exacerbated by cost inflation issues due to high construction materials costs & strong wage rises, particularly given skills shortages, & this hit financial viability, especially for small contractors. (5/n)#ukconstruction #ukhousing pic.twitter.com/TfLjHOSsa9

— Noble Francis (@NobleFrancis) February 16, 2024

The majority of UK construction insolvencies were in specialist sub-contractors, especially firms on fixed-price contracts. 58% of the construction firms (2,545 firms) that went under in the year to December were specialist sub-contractors, which is… (6/n)#ukconstruction pic.twitter.com/TxNoIrSVbJ

— Noble Francis (@NobleFrancis) February 16, 2024

… unsurprising given that major house builder & main contractor business models are based on subcontracting out the majority of the cost, activity & risk to smaller firms that are less able to deal with demand & supply issues given that… (7/n)#ukconstruction #ukhousing pic.twitter.com/6PYxE8XiQ8

— Noble Francis (@NobleFrancis) February 16, 2024

The next few weeks could prove to be challenging for businesses, says Zelf Hussain, Restructuring Partner at PwC UK.

Hussain explains:

âWith the latest GDP figures showing that the UK was in a technical recession at the end of last year,the retail, hospitality and construction sectors continue to bear the brunt of insolvencies.

These industries, traditionally sensitive to shifts in consumer behaviour and economic conditions, remain under significant pressure due to ongoing challenges, including changing consumer priorities and supply chain disruptions – issues which may not be resolved in the first half of this year.â

Insolvencies up 5% year-on-year

Just in: The number of registered company insolvencies in England and Wales jumped 5% on an annual basis last month, although it was lower than in the peak last autumn.

There were 1,769 company failures in January, the Insolvency Service reports, up from 1,685 in January 2023, as companies struggled in the tough economic climate.

The Insolvency Service reports:

The company insolvencies consisted of 339 compulsory liquidations, 1,294 creditorsâ voluntary liquidations (CVLs), 120 administrations and 16 company voluntary arrangements (CVAs). CVL numbers were lower than in January 2023, while compulsory liquidation and administration numbers were higher.

Itâs lower than the 2,470 insolvencies reported in November, though which was the highest since last May.

David Hudson, restructuring advisory partner at FRP, says high interest rates and rising costs are hitting firms:

âA real concern is that current financial distress spreads further. Last yearâs insolvency data shows a large proportion of Creditorâs Voluntary and compulsory liquidations â a sign that many of the closures were among SMEs. Should more mid-market firms start to fail, the impact is likely to have even greater ramifications up and down supply chains. A larger stone ultimately ripples much wider.

âSignificant trading risks abound for the months ahead. Early interest rate cuts still look unlikely, meaning capital and debt costs will remain high for some time yet. And companies, particularly retailers and hospitality firms, will be bracing themselves for the rise in the National Living Wage in April, which could add further strain to already stretched bottom lines.

âThereâs good reason to be optimistic that economic conditions will improve this year, but for now businesses are still driving down a bumpy road.â

Moodyâs Analytics: Expect first UK rate cut in August

Britainâs fall into recession yesterday sparked talk that the Bank of England could lower interest rates sooner than expected, to prod the economy into growth.

But Moodyâs Analytics reckons that borrowers may need to wait six months for a cut.

In a report released last night, their economist Barbara Teixeira Araujo says:

âWhile the GDP figures for the fourth quarter were extremely bad, we havenât changed our outlook for the U.K. economy and for monetary policy. We expect that the economy to hold its ground in 2024 and that the momentum will gradually improve throughout the year. We are pencilling in a 0.3% rise in GDP in 2024, up from 0.1% in 2023.

Regarding the BoE, we think the central bank would rather risk waiting a bit too long than cut a bit too early. We still expect a first rate cut in August.â

The money markets are expecting the first rate cut by June, from 5.25% to 5%, with rates seen at 4.5% by the end of 2024.

{kind=link}