jaanalisette

When tech stocks soared at the beginning of the year, many investors asked the question: Is it too late to jump in on the recovery rally? Now, it certainly isn’t – with interest rate rises and bank scares putting a damper on investors’ risk appetites, it’s a great time to buy the dips in some fantastic tech companies.

Look no further than Twilio (NYSE:TWLO) for a great buying opportunity. Consistent with my earnings preview in early February, Twilio smashed Q4 results and impressed the Street with an upbeat outlook for FY23 as well as a renewed focus on profitability. Though the stock initially jumped post-earnings, broader market turmoil since then has wiped out all of Twilio’s post-earnings gains, and now the stock is sitting at only up 21% for the year.

I remain very bullish on Twilio, and I am holding onto the stock as a fixture in my portfolio. The first thing investors should know is that as Twilio’s growth recedes (due both to its sheer size now as a company that generates >$1 billion in quarterly revenue, as well as macro pressures), the company is pivoting to focus on profitability.

Alongside its fourth-quarter earnings, the company announced a substantial restructuring. It is now aligning its management structure into two business units, Twilio Communications (led by the company’s former CFO) as well as Twilio Data & Applications. And underneath this large shake-up, the company is also letting go of roughly 17% of its global workforce while still looking to “pursue further expense rationalization.”

The company now expects to be profitable on a pro forma basis in 2023, while also lowering stock-based compensation with an eye to becoming profitable on a GAAP basis in the medium term (2025 to 2027).

We should recall that Twilio sits on a large recurring revenue base, with its technology deeply rooted in clients’ consumer-facing applications. Here is my full bull case for Twilio:

- Universal, horizontal software platform that has limitless opportunities for expansion. Many kinds of applications require the ability to connect with their customers through talk and text, and as more and more of our lives go digital, Twilio’s potential base of customers will continue to widen. Twilio has also been adept at expanding its core product set, adding call-center software capabilities as well as email marketing tools through its acquisition of SendGrid. A recently added product called Twilio Live also introduces live-streaming capabilities for Twilio clients.

- Land and expand; growth alongside the customer base. Twilio is one of the best examples of a “land and expand” software company. Because it prices its services by usage (for example, per messages sent), its revenue grows when the underlying apps it powers do. This gives Twilio a powerful, built-in growth engine.

- Customer diversification. Twilio used to be heavily reliant on large accounts; now, the company’s top 10 customers represent only 13% of revenue, and the company has over 280k total customers.

- Path to profitability. Driven by expanding gross profit dollars per message sent, as well as economies of scale on opex as Twilio continues its organic growth path, the company expects to be above breakeven profitability on a pro forma basis by FY23.

Note as well that Twilio kicked off a $1 billion share buyback program, which at today’s prices covers roughly 9% of the company’s market cap – an excellent opportunity for the company to take advantage of the stock’s recent dip.

Stay long here: There’s plenty of upside for Twilio, especially as the company leans in on its profitability strategy.

Q4 Download

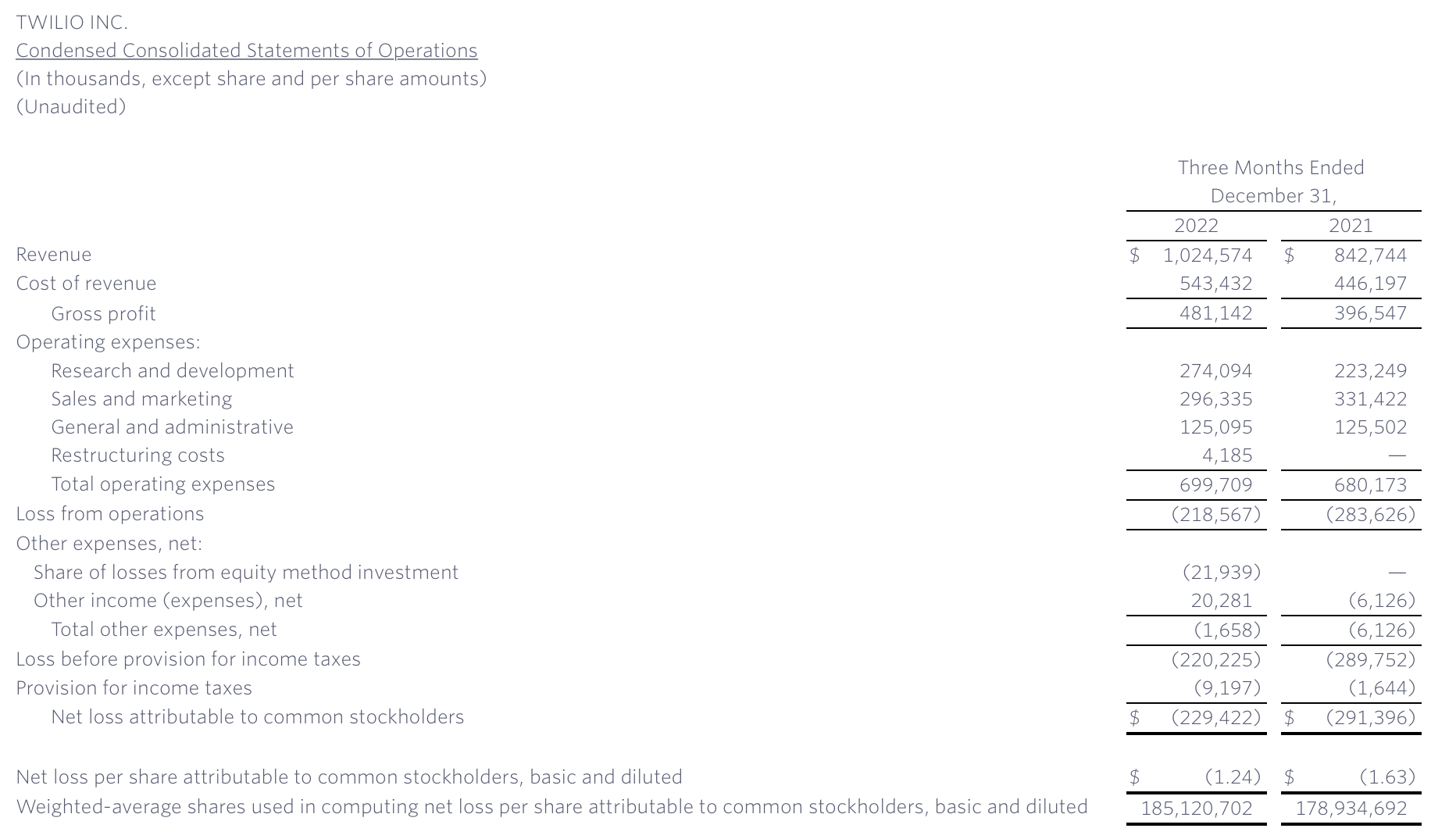

Let’s now cover Twilio’s latest Q4 results in greater detail. The Q4 earnings summary is shown below:

Twilio Q4 results (Twilio Q4 earnings materials)

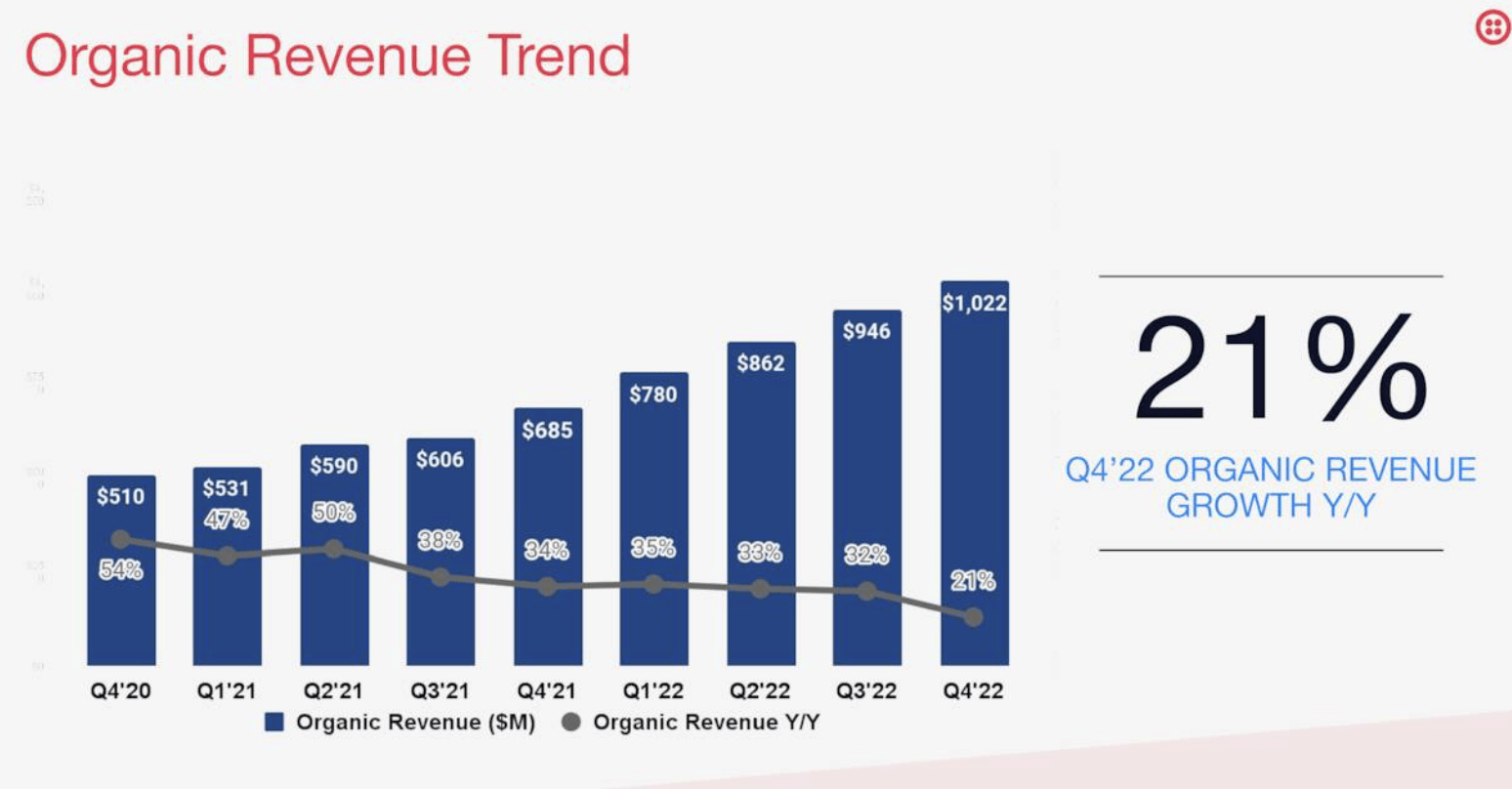

Twilio’s revenue grew 22% y/y to $1.02 billion, beating Wall Street’s expectations of $1.00 billion (+19% y/y) by a three-point margin. Of course, one of the big highlights here is that revenue growth is decelerating sharply from 32% y/y in the prior quarter.

Twilio organic growth (Twilio Q4 earnings materials)

Part of this is driven by lapping last year’s strong post-COVID reopening lifts, which saw an uptick in Twilio customers’ applications (think Uber (UBER)). And part is also driven by macro headwinds, which Twilio noted is causing an elongation of sales cycles (which is similar to commentary that other software companies are providing). Per President Elena Donio’s remarks on the Q4 earnings call:

We feel really good about having built out those teams with the right set of skills and the right capabilities, doing some internal transfers as well as hiring from the outside with the right set of bespoke skills. So, I’m really confident in how that’s turning.

We’ve also talked about some macro headwinds. Those continue in a couple of areas, some lengthening of sales cycles, pushing out of decisions and things like that from time to time. But with all of that in mind, we feel really good about the things we can control. We feel really good about the investments that we’ve made and the trajectory ahead. And we also have really — we still believe and we shouldn’t — we don’t think that this movement across two different business units should say anything different.”

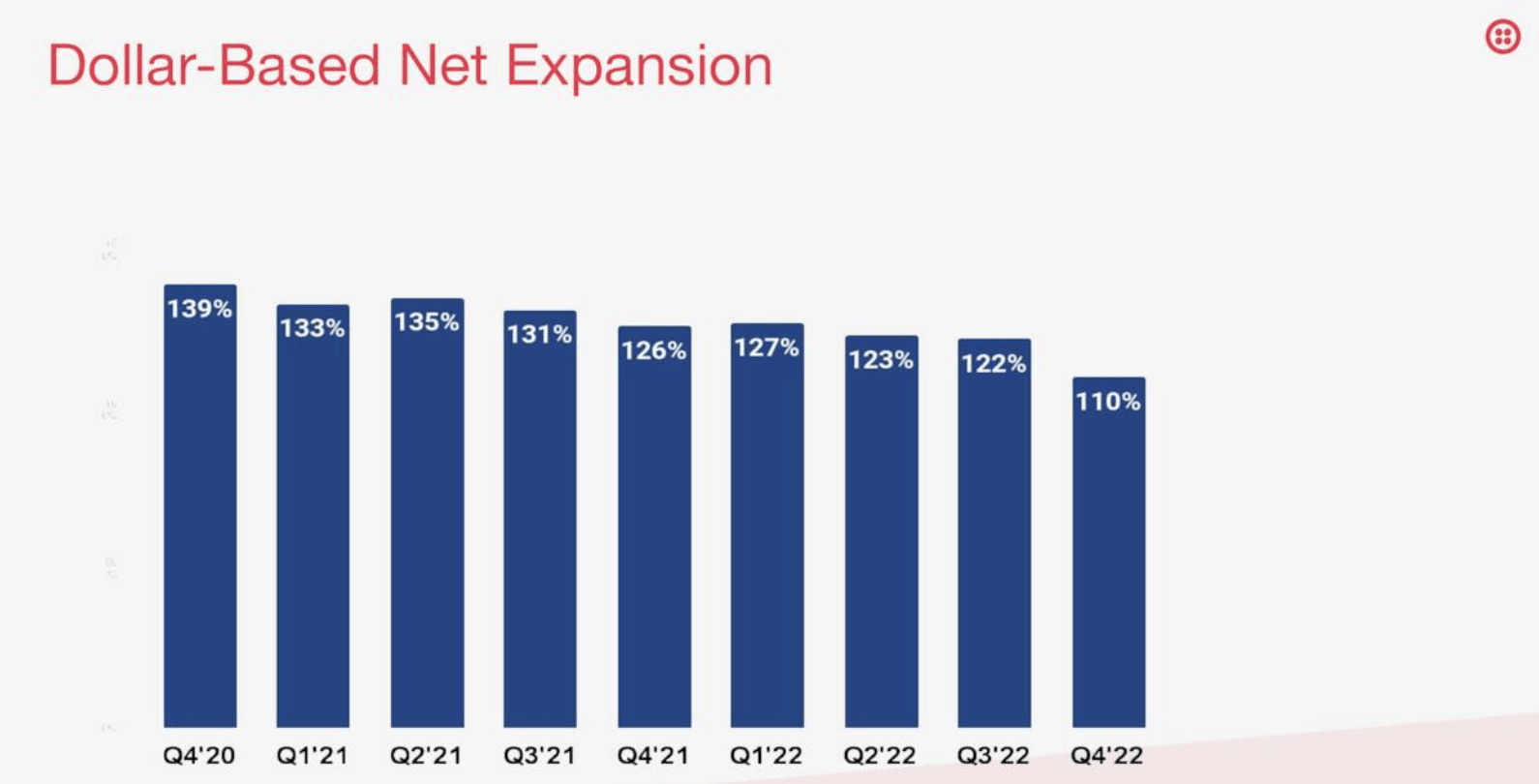

Equally hit hard is the company’s dollar-based net retention rates, which have fallen to 110% – though the company believes that this will pick back up when the economy recovers.

Twilio net expansion trends (Twilio Q4 earnings materials)

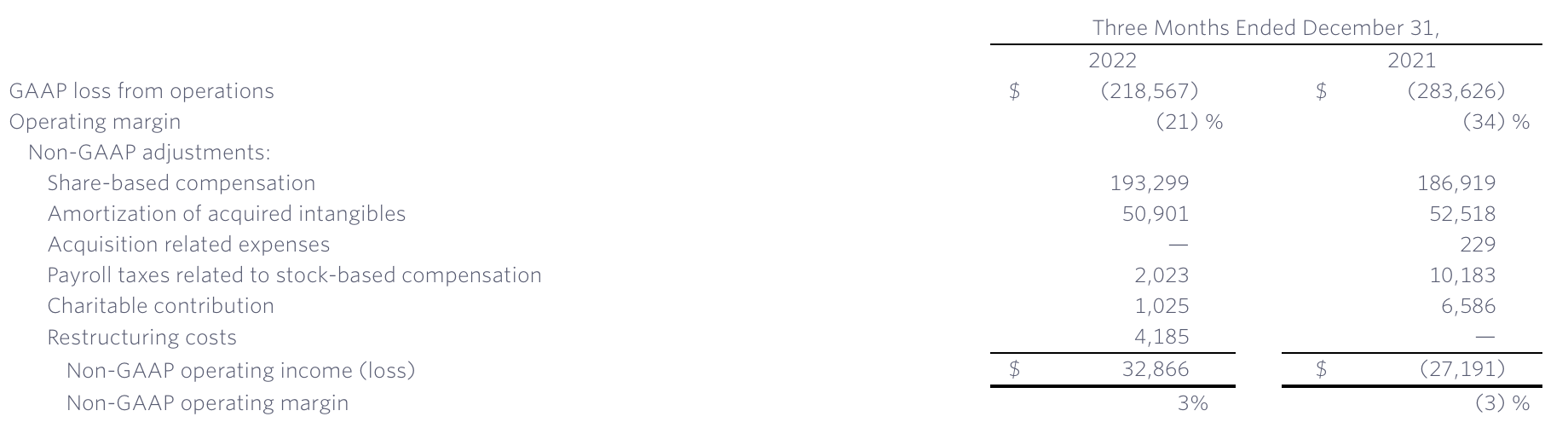

The bright side to focus on, however, is profitability. The company generated a 3% pro forma operating margin in Q4, up six points versus the prior-year Q4.

Twilio operating margins (Twilio Q4 earnings materials)

The company’s pro forma EPS of $0.22 in the quarter also smashed Wall Street’s expectations of an -$0.08 loss.

Valuation and Key Takeaways

Twilio remains, in my view, an excellent value stock. At current share prices near $60, the company trades at a market cap of $11.40 billion. After we net off the $4.15 billion of cash (Twilio will have no issues financing its $1 billion buyback program) against its $0.98 billion of debt, the company’s resulting enterprise value is $8.23 billion.

For the current fiscal year FY23, Wall Street analysts have pegged a revenue consensus of $4.30 billion for the company, representing 13% y/y growth (data from Yahoo Finance). This puts Twilio’s valuation at just 1.9x EV/FY23 revenue.

For a company that is targeting meaningful gains in profitability through large cost reductions (it is guiding to $250-$350 million in pro forma profit in FY23, implying a midpoint pro forma operating margin of ~7% against consensus revenue) and also has substantial cash to finance a large buyback, I think Twilio is quite opportunistically priced. Don’t miss out here.

{kind=link}