Ralf Hahn/iStock via Getty Images

While I typically avoid ETFs due to the fees, an ETF that has been on my watchlist for more than a year is the ProShares UltraPro QQQ ETF (NASDAQ:TQQQ). I have seen comments asking when I plan to buy, or if I bought any steep declines like the one last fall. I want to talk briefly about some of the characteristics of TQQQ (and other leveraged ETFs) before getting into the largest holdings.

My plan for potentially buying a tiny position of TQQQ would probably have a one to six-month timeframe, basically a short- to medium-term strategy. I would probably be looking for another 20% decline (or more) in the major indices before buying TQQQ. If we see that, combined with a potential return of the Federal Reserve money gun, TQQQ could be an interesting short-term trade.

TQQQ offers more speculative upside than QQQ on a smaller position size, and I would rather buy TQQQ than use leverage to buy QQQ. You pay the ETF management fees, but I think it’s more attractive than borrowing to buy QQQ at current margin rates.

Disclaimer

The risks with TQQQ include beta slippage, but also short-term volatility that can be stomach-turning. For example, a big market decline can cut an investment in TQQQ by 20% or 30% in a week, so investors should go into an investment in TQQQ with eyes wide open to those risks. Investors that are unfamiliar with the potential risks might want to spend a couple of minutes to read what the SEC has to say about leveraged ETFs.

ProShares UltraPro QQQ® (the “Fund”) seeks daily investment results, before fees and expenses, that correspond to three times (3x) the return of the Nasdaq-100® Index (the “Index”) for a single day, not for any other period. A “single day” is measured from the time the Fund calculates its net asset value (“NAV”) to the time of the Fund’s next NAV calculation.

The return of the Fund for periods longer than a single day will be the result of its return for each day compounded over the period. The Fund’s returns for periods longer than a single day will very likely differ in amount, and possibly even direction, from the Fund’s stated multiple (3x) times the return of the Index for the same period. For periods longer than a single day, the Fund will lose money if the Index’s performance is flat, and it is possible that the Fund will lose money even if the level of the Index rises.

Longer holding periods, higher Index volatility, and greater leveraged exposure each exacerbate the impact of compounding on an investor’s returns. During periods of higher Index volatility, the volatility of the Index may affect the Fund’s return as much as or more than the return of the Index.

The Fund presents different risks than other types of funds. The Fund uses leverage and is riskier than similarly benchmarked funds that do not use leverage. The Fund may not be suitable for all investors and should be used only by knowledgeable investors who understand the consequences of seeking daily leveraged (3x) investment results of the Index, including the impact of compounding on Fund performance. Investors in the Fund should actively manage and monitor their investments, as frequently as daily. An investor in the Fund could potentially lose the full value of their investment within a single day.

Inflation & The Next Decade

The biggest problem I see with TQQQ is the concentration in the large tech companies, which is also a problem for Invesco QQQ ETF (QQQ), which TQQQ follows. While that worked great for investors until late 2021, I think markets have begun to shift over the last couple of years. I’m of the opinion that commodities, energy, and companies with real assets will outperform over the next decade. I was watching for inflation starting in 2020 for several reasons, but I think the idea that inflation will come down to where it was over the last decade is wishful thinking.

That doesn’t mean I’m predicting hyperinflation or anything drastic like that, but I think we will see inflation stop and start for years, and I think inflation will probably be 5% or higher for years. That’s just CPI, and if you want to go down the rabbit hole on inflation, you should check out shadowstats.com. Their website tracks inflation using old measurements, which shows how understated CPI is compared to actual inflation. I will do brief overviews of each company in the top 10, but on the whole, I don’t think the largest parts of TQQQ represent attractive risk/reward prospects today.

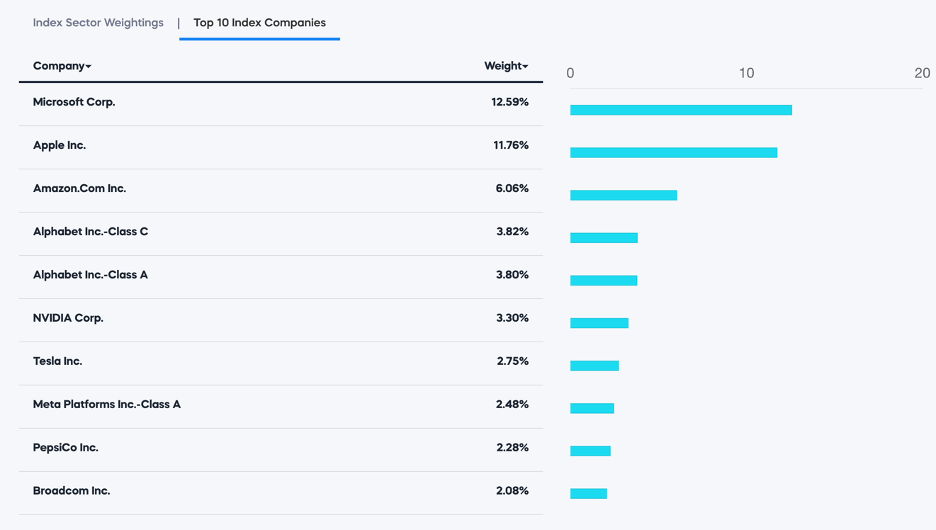

TQQQ Top 10 (proshares.com)

Apple & Microsoft

Like any market cap weighted index or ETF, Apple (AAPL) and Microsoft (MSFT) will make up a large portion of the fund. While this is true for S&P 500 indices like (SPY) or (VOO), these two companies have an even larger weighting in TQQQ. Both have well over 10% weightings, but I’m not going to go into too much detail because I wrote articles on both in the last couple of months (here and here). Apple has a market cap of $2.4T, while Microsoft has a market cap of $1.9T, which will probably be a drag on forward returns. I don’t find either attractive simply due to the valuations, which I talked about in those articles, and I have my doubts on how much either can grow from here. Another thing that I’m not a huge fan of is how both companies continue to buy back large amounts of stock regardless of the valuation.

Amazon

Amazon (AMZN) and its $972B market cap account for another 6% of the ETF. I have been bullish on Amazon because of AWS, but I have been wondering if it might be worth selling my small position in Amazon to buy something else. I still think the company is in a good position with their core businesses, especially AWS, but if the right opportunity comes along, I might part ways with my Amazon shares. Of the largest components of TQQQ, I think Amazon is still the most attractive today.

The Ad Giants – Google & Meta

These two are companies I’m not really interested in owning for several reasons, but I don’t think the coming years are going to be a great environment for advertising businesses like Google (GOOG) (GOOGL) and Meta (META). Google has a P/E of 20.5x and a market cap of $1.2T, and accounts for about 7.5% of TQQQ. I’m curious to see how ChatGPT and other developments, including smaller video platform competitors for YouTube, impact Google’s search engine monopoly, but I don’t think the next decade will be as good for their business as the last one was.

Meta has had a massive run since the beginning of November, and shares now trade at an earnings multiple of 21x. This puts the market cap at $480B and is 2.5% of TQQQ. I have my doubts about the Metaverse strategy, and I have been critical of the company’s buybacks a couple of years ago as the CEO was dumping a huge number of shares. Like Google, I think the next decade will not be like the last one for Meta.

Pie In The Sky Valuations – Nvidia & Tesla

Both these companies have had massive runs to start 2023, and I think the valuation is so rich that I would honestly rather be short these two than own them. I actually bought a put option on Tesla (TSLA) when shares were around $205, so we will see if that pays off. The contract expires near the end of April with a strike of $150. I don’t gamble much, but I watched the absurd move Tesla made to start the year, and it looked like short-covering and speculative buying instead of an actual fundamental improvement in the business. If shares keep dropping, I will probably look to exit the trade in the next couple of weeks.

Nvidia (NVDA) also had its own massive move, including a large jump after earnings. They can talk all they want about AI in their earnings calls, but I don’t see how investors owning Nvidia today generate attractive forward returns. I could be wrong, but unless Nvidia can grow rapidly through the next couple of cycles for the semiconductor industry, buying at the current valuation is not attractive in my opinion. Between the two companies, they account for about 6% of TQQQ, which means there is another sizable chunk of the ETF that find unattractive.

Rounding Out The Top 10 – Pepsi & Broadcom

Pepsi (PEP) is the only non-tech company in the top 10, with a 2.3% weight. While I don’t think the downside is as big as some of the other stocks in the top 10, it’s not a business I would pay over 25x earnings for, despite a 2.7% dividend. It’s a slow-growth business, and I don’t find their business mix to be all that attractive. It’s basically just a mix of different junk foods and drinks, and I think people will start to pay more attention to their diet and health in the coming years.

Broadcom (AVGO) would probably be my first choice to buy in the top 10 today, but it only accounts for just over 2% of the ETF. The company has a P/E of just over 16x and a dividend yield of 2.9%, and a history of being a very successful operator in the semiconductor industry. They operate in a different part of the industry than Nvidia, but the valuation is much more attractive. The market cap is $264B, so they might not grow as fast as the last decade, but Broadcom is a solid dividend growth stock.

Conclusion

I’m sure some commenters will talk about their trades in TQQQ (which I love to hear about, by the way), but I’m just not at a point where I’m comfortable buying the ETF today. TQQQ has a different risk profile than QQQ, including potential systemic issues and massive volatility with leveraged ETFs, but if your timing is good, you get a lot more bang for your buck buying the leveraged TQQQ ETF. I have said in the past that I’m looking for capitulation and panic, but I will still look elsewhere as long as the valuations for the largest stocks in the index stay rich. There are only a couple of stocks in the top 10 I find attractive today, but TQQQ could still have a huge run if the market takes off. While TQQQ is still on my watchlist, it is staying on the backburner while I focus on other sectors that I find more attractive today.

{kind=link}