demaerre/iStock via Getty Images

Amid an incredibly tough macro climate, small-cap companies that have already been struggling before the economy turned south are facing even deeper straits now. Stitch Fix (NASDAQ:SFIX), the clothing e-commerce company that was once lauded for its innovative “Fix” approach of having stylists send customers a curated batch of five items, is no exception. The beleaguered online retailer is dealing with a continuous outflow of customers and deep revenue declines.

Year to date, however, shares of Stitch Fix have jumped ~30%. Sentiment has improved mildly over the past month as interest in tech stocks surged and on a company-specific basis, Stitch Fix also A) turned in relatively strong profitability results in its fiscal Q3 earnings and B) finally announced a new permanent CEO, Matt Baer (a former Macy’s e-commerce executive), replacing founder Katrina Lake who had stepped back into the CEO role on an interim basis.

Is smaller better? Many risks for Stitch Fix still abound

To sum up Stitch Fix’s strategy to deal with its downturn: the company has elected to downsize and take a “smaller is better” approach. On top of deep layoffs over the past year, Stitch Fix has also decided to slim down the number of its distribution centers from five to three. By not renewing leases on distribution centers in Pennsylvania and Texas, the company hopes to centralize its inventory into fewer hubs – ultimately allowing the company to operate at leaner inventory levels to conserve cash.

So far, on top of deep opex cuts, the strategy seems to be producing slightly better profitability on an adjusted EBITDA basis, and for that reason plus the resolution of its open CEO question, I am slightly upgrading my viewpoint on Stitch Fix to bearish, up from a prior view of very bearish.

“Smaller is better” is a strategy that has worked well for embattled consumer technology companies in the past – GoPro (GPRO) is one that comes to mind. Yet at the same time, we can’t ignore the myriad risks that Stitch Fix still deals with:

- Is Stitch Fix relevant anymore, or is it just a passing fad? The idea of getting a “Fix” of five items and keeping only what you like was the whole selling point behind Stitch Fix in the first place. But declining active customers seem to be suggesting that people don’t want this complexity in the shopping process. In fact, Stitch Fix introduced its direct-buy “Freestyle” program to mirror classic e-tailers: and in doing so, it lost its niche in the first place. Without much of a powerful brand to draw from, it’s unclear how Stitch Fix plans to remain relevant.

- Sharp competition from fast casual clothiers. Uniqlo, Zara, and a number of upstart direct-to-consumer brands have exploded on the retail scene. Amid “basic convenience” buyers, it’s unclear where Stitch Fix fits in.

- No clear moat. Stitch Fix’s innovative buying method was part of its appeal versus the dozens of e-commerce clothing competitors out there. With the business doubling down on Freestyle, it’s unclear what Stitch Fix plans to do to hold onto customer loyalty.

- Weighed down by inflationary pressures. Stitch Fix’s gross margins are declining. At the same time, even though the company is letting go of a chunk of its staff, it is also facing corporate wage inflation. The net result is a deep gush of red ink, which is exactly what Wall Street does not want to see in this very cautious stock market.

Ultimately, my view here is that until Stitch Fix can prove it can turn around its top-line trends (revenue, active customer counts, and average basket sizes), no amount of operational mending can save Stitch Fix. Continue to exercise caution here and invest elsewhere.

Q3 download

Stitch Fix recently released its fiscal Q3 (April quarter) results, and while the company’s ability to turn positive adjusted EBITDA profits is heartening, even these slim profits will fade if customer counts continue to shrivel.

Take a look at the Q3 earnings summary below:

Stitch Fix Q3 results (Stitch Fix Q3 earnings release)

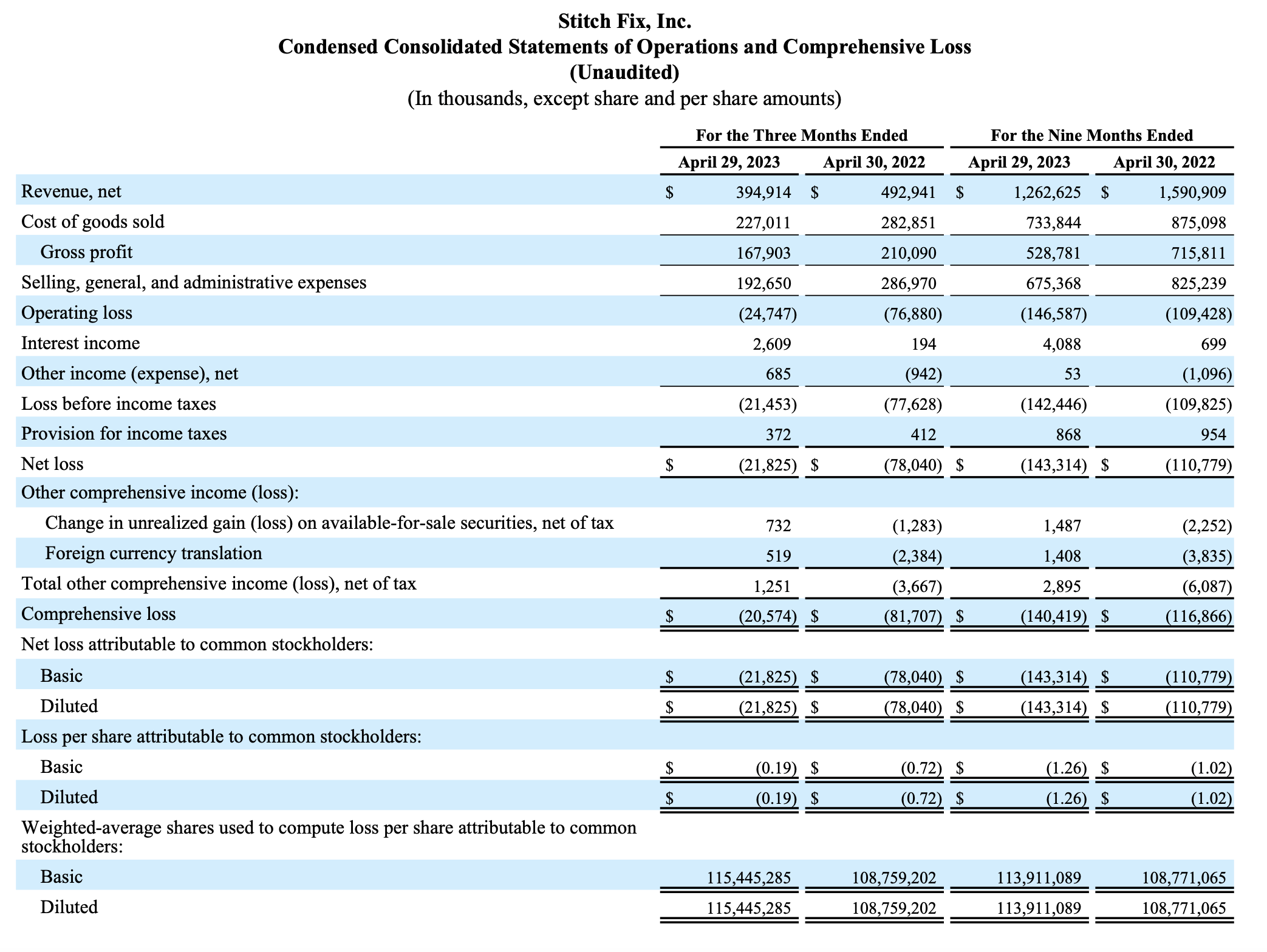

Stitch Fix’s revenue declined -20% y/y to $394.9 million, slightly beating Wall Street’s expectations of $388.8 million (-21% y/y) by a one-point margin. The decline here was consistent with a -20% y/y decline in Q2.

Active customers, meanwhile, continued to shrink – as a reminder here, Stitch Fix defines an active customer as somebody who has made a purchase within the last 12 months. Given the recency of Stitch Fix’s sharper revenue declines, we should expect more customer bleed-off as long-tailed customers lapse as inactive. In Q3, the company counted 3.476 million active customers, down 98k sequentially and -11% y/y.

Stitch Fix active client counts (Stitch Fix Q3 earnings release)

It’s worth noting as well that in Stitch Fix’s current “downsizing” mantra, the company has also elected to exit the UK market, which was the company’s first major international foray. Per founder Katrina Lake’s remarks on the Q3 earnings call:

Additionally, the continued realities of economic conditions in both the U.S. and the UK have led us to re-examine our geographic footprint. And this morning, we informed our employees in the UK that we are exploring exiting the UK market in FY 2024. In FY 2023, the UK will represent approximately 50 million in annual revenue and negative 15 million of adjusted EBITDA.

Though we believe Stitch Fix is a service that will ultimately find success across many geographies, including the UK and Western Europe, today, we are not confident in the path to profitability in the near-term in that market, especially as we prepare for potentially extended periods of complicated macroeconomic conditions in both the U.S. and UK. There are also numerous investments we have made in our core client experience that we have not replicated in our client experience in the UK.”

The bright side behind this is profitability. Gross margins, a perennial challenge for Stitch Fix, improved 150bps sequentially from Q2 to 42.5% (though down 10bps y/y). The company is aiming to boost gross margins through a combination of lower promotional activity plus its slim-down of inventory (hopefully reducing obsolescence and waste).

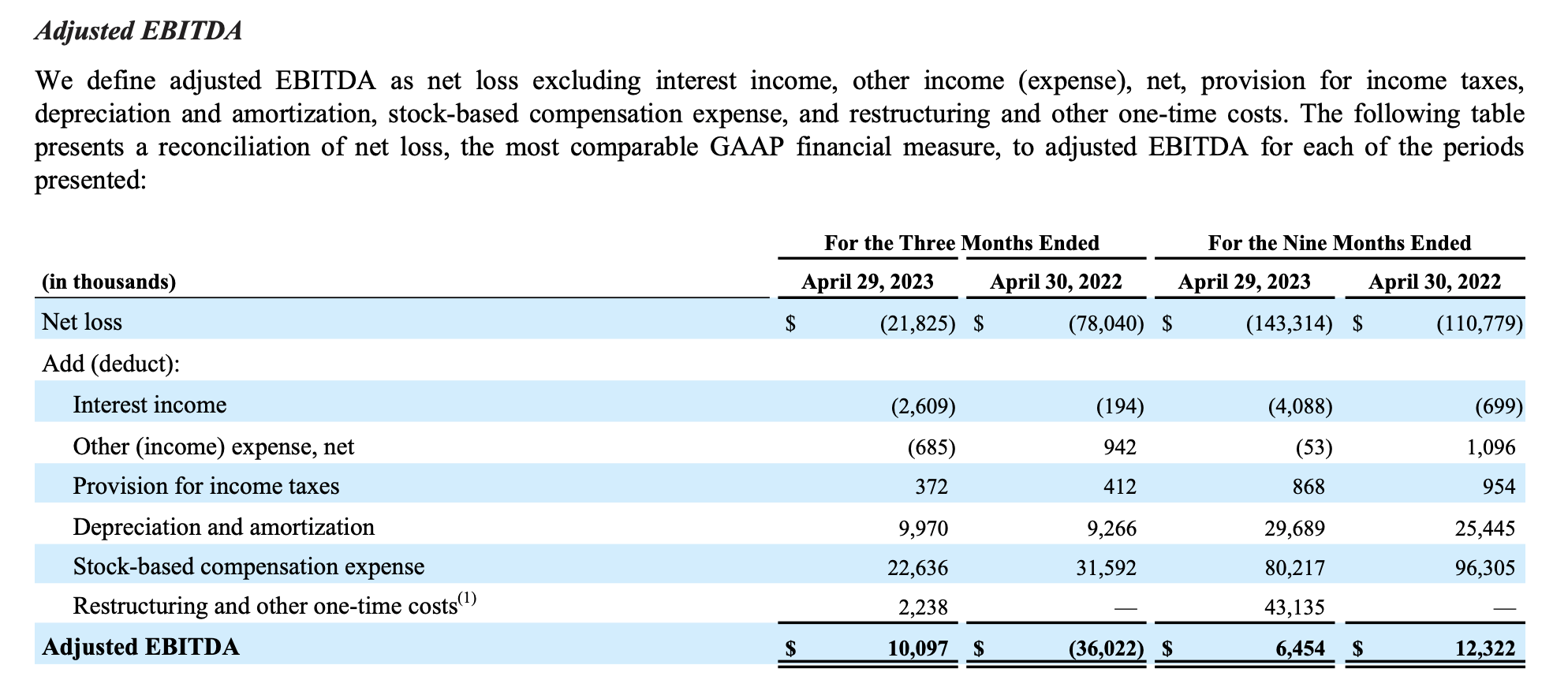

Stitch Fix adjusted EBITDA (Stitch Fix Q3 earnings release)

As shown in the chart above, Stitch Fix’s adjusted EBITDA expanded to $10.1 million (a 2.6% margin), versus -$36.0 million (-7.3% margin) in the year-ago quarter. The company expects to generate $10 million in adjusted EBITDA for the full year FY23, implying $3.5 million in adjusted EBITDA for Q4. This is inclusive of $135 million of cost savings / headcount reductions already implemented in FY23, and the distribution center shrinkage that the company is proposing for FY24 is expected to generate $50 million of annualized savings.

Key takeaways

Though I find Stitch Fix’s commitment to course-correcting its business and slimming down costs admirable, I think the negative revenue and customer trends will outweigh these efforts and still plunge Stitch Fix into incurable depths. Remain on the sidelines here.

{kind=link}