US export controls designed to freeze-in-place China’s leading edge chip development are a powerful brake on Beijing’s ambitions to become self-sufficient in foundational technologies. But this should not obscure the fact that China is building significant capacity in semiconductor markets that rely on mature process nodes – including in sensors, power semiconductors, and microcontrollers found in every day consumer electronics, vehicles, and medical devices. This note takes a closer look at which semiconductor segments still lie beyond the reach of US regulators and where Chinese chipmakers and state backers may focus their resources. We also assess how China’s expanding market share in these mature technology segments could trigger regulatory actions by the US aimed at steering supply chains away from China.

This note was prepared in cooperation with Jan-Peter Kleinhans and Julia Hess at Stiftung Neue Verantwortung.

Key Takeaways

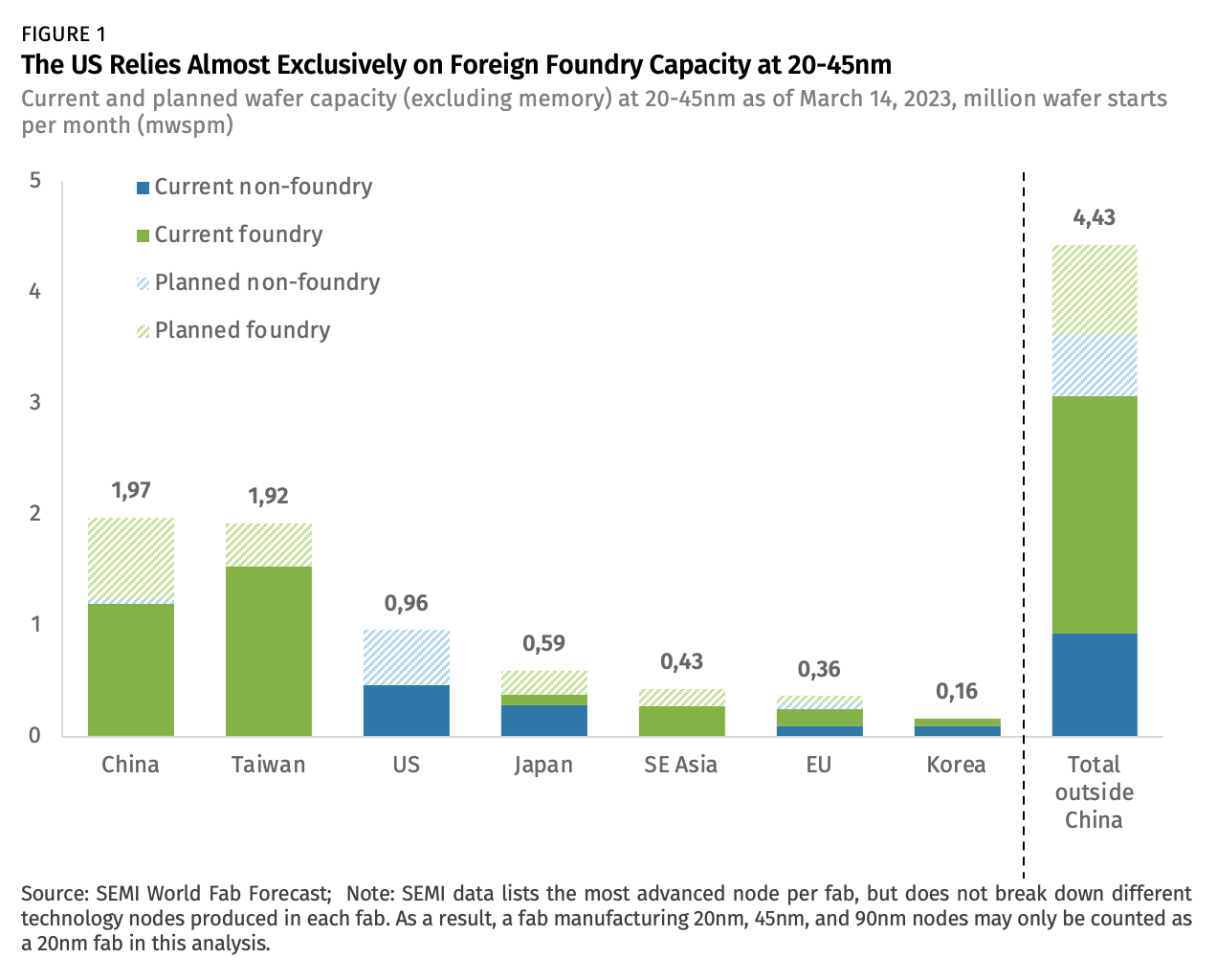

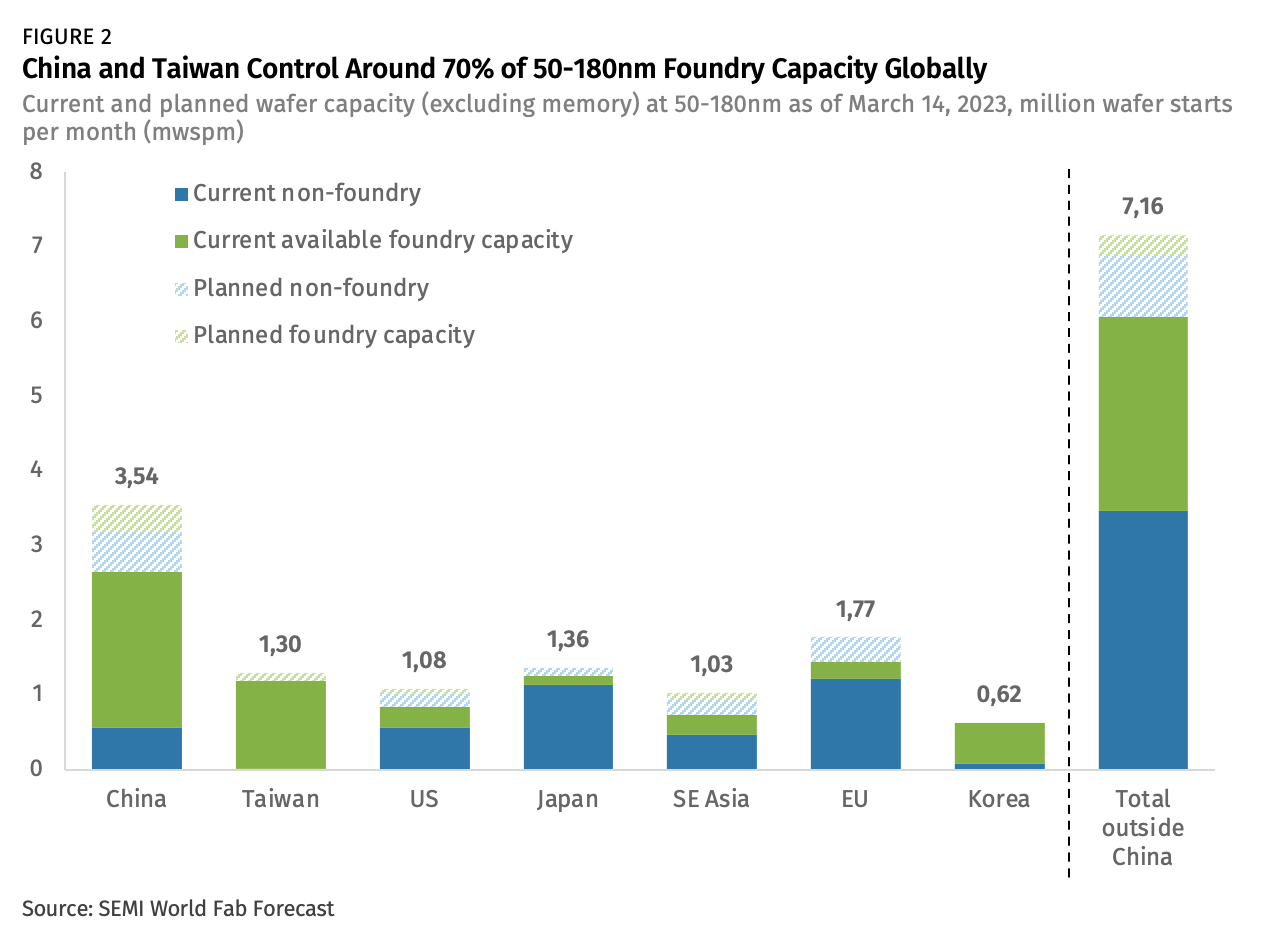

- US fabless chip designers depend almost entirely on foreign foundries for contract-manufacturing of legacy chips: 80% of foundry capacity for 20-45nm process nodes is located in China and Taiwan. For 50-180nm process nodes, China and Taiwan together control around 70% of foundry capacity globally.

- An attempt by the US and partners to outpace China in building out manufacturing capacity for trailing edge process nodes would require considerable time and resources, as well as political tolerance of higher prices. In the next 3-5 years China is due to add nearly as much new 50-180nm wafer capacity as the entire rest of the world.

- China’s tech indigenization efforts, the threat of US export controls, and OEM supply chain diversification could help Chinese chipmakers grow market share in segments that do not rely on node shrinkage, such as microcontrollers and automotive semiconductors.

- Chinese firms designing cutting-edge semiconductors for markets like smartphone processors and autonomous driving are still producing well below the high performance computing thresholds set by US export controls, but will remain heavily dependent on foreign-owned foundries to manufacture such chips.

Navigating US Chip Controls

The US has ramped up semiconductor export controls aimed at China over the past year. In August 2022, the US implemented a multilateral agreement to restrict electronic design automation software for cutting edge chip development. Then, on October 7, 2022, the US rolled out a comprehensive package of export controls that restricted sales of high-performance computing chips to China and targeted critical chokepoints in semiconductor value chains—software and chip manufacturing equipment—to arrest China’s development in leading edge chips. By early 2023, the United States had negotiated an understanding with Japan and the Netherlands (both critical to the SME controls) to restrict the export of tools needed to produce logic chips at 14nm and below.

If rigorously enforced, mounting US-led restrictions could severely curb China’s ability to scale up leading edge chip development and make advancements in “force-multiplying” semiconductor technologies, including supercomputing and cloud artificial intelligence (AI) accelerators.

The heaviest restrictions in the Oct. 7 controls are centered on high performance computing chips. There are just a handful of companies globally that design such state-of-the-art chips. These include US-based Nvidia’s H100 and AMD’s MI250, as well as Chinese start-up Biren Technologies’ BR100. If cutting-edge chips with US-origin technology meet the compute performance thresholds in the Oct. 7 controls, the US can block the sale and production of these chips to any Chinese entity. This could have a profoundly negative impact on Chinese companies designing cutting-edge chips for cloud computing, deep neural networks, and other applications that require massive amounts of computing power—an alarming prospect for China as the United States is embarking on a new innovation era in areas like generative AI.

Below the Radar

The US has (for now) set relatively high compute performance thresholds for these restrictions. For example, one of the thresholds is 4800 TOPS * bits (tera operations per second). Chinese companies designing cutting-edge chips for markets like mobile chipsets (e.g., UNISOC, Xiaomi, Oppo, and Vivo) or autonomous driving chips (e.g., Horizon Robotics) could stay well below such thresholds.

For example, UNISOC’s current state-of-the-art mobile chipset T820 has an integrated AI accelerator with 8 TOPS at 8 bits precision, resulting in 64 TOPS * bits—far below the US-regulated 4800 TOPS * bits threshold. The same goes for Horizon Robotics’ autonomous driving chip, Journey 5, which has a compute power of 128 TOPS at 8 bits precision, resulting in 1024 TOPS * bits. So long as the United States maintains a relatively high compute performance threshold, these firms will still be able to compete in international markets for years to come, albeit with a lingering risk that Washington can adjust the regulatory parameters at any time.

In addition to setting compute performance thresholds in designing China-wide restrictions, the Oct. 7 controls and US negotiations with its partners have focused on the critical inputs needed to produce advanced logic chips at or below 14nm. These controls directly impact China’s ability to fully indigenize production of server, laptop, graphic and smartphone processors — a market where a product’s competitiveness relies heavily on shrinking the node feature size of the chips powering the device. For example, Apple’s A16 processor for the iPhone 14 Pro (16 billiontransistors on a 4nm node) has one hundred times more transistors than Apple’s A4 processor in the iPhone 4 (149 million transistors on a 45nm node).

When Size Doesn’t Matter

The Oct. 7 controls deal a heavy blow to China’s chip ambitions but there are still many types of chips that do not depend on or even benefit from node shrinkage (e.g., how many transistors can be squeezed onto a square millimeter of silicon). This is true for power semiconductors, analog chips and microcontrollers, where China still has ample room to grow. A wide range of applications, including cars, medical devices, Internet of Things, drones, industrial automation, robotics, and precision agriculture rely mainly on chips manufactured on “mature nodes” where Chinese foundries like SMIC and Hua Hong are rapidly building out capacity.

Classifications like “legacy”, “mature” or “trailing-edge” node production can be somewhat misleading in describing fabs manufacturing chips for power semiconductors, image sensors or microcontrollers. Mature node feature sizes (such as 28nm, 45nm or 90nm) can still be considered “state of the art” in their respective markets.

The Foundry Capacity Challenge

Below we break down foundry and non-foundry capacity at 20-45nm (key for microcontrollers) and 50-180nm (important for power semiconductors, IoT chips and sensors) process nodes. The distinction between foundry and non-foundry is critical: China’s and Taiwan’s capacity comes from foundries for contract manufacturing, meaning they offer their skills and manufacturing capacity to any firm designing chips. In contrast, the United States’ share of trailing-edge wafer capacity comes almost exclusively from Integrated Device Manufacturers (IDMs), such as Texas Instruments, that design and manufacture their own chips in their own fabs. As shown in Figure 1, US chip designers depend almost entirely on foreign foundries to manufacture chips on 20-45nm nodes.

Share Figure

Data on announced fab investments as of March 2023 show that around 60% of worldwide manufacturing capacity for 20-45nm process nodes is located in China and Taiwan, with 27% in China alone. Once new fabs that are scheduled to come online are included, China and Taiwan together could account for close to 80% of 20-45nm foundry capacity globally over the next 3-5 years.

The picture looks very similar in mature nodes at 50-180nm: China currently controls around 30% of 50-180nm manufacturing capacity globally, and that could climb to 35% global capacity within the next 5 years (Figure 2) if all fabs in China that have been announced as of March 2023 are built according to plan. Within a decade, China could control around 46% of 50-180nm global foundry capacity for fabless chip designers.

China’s expanding mature node wafer capacity carries important implications for both Chinese and foreign OEMs. For China’s domestic manufacturers of electric vehicles, industrial robotics, drones, IOT appliances, medical devices and other products, China’s low-margin and high-volume growth in legacy chip manufacturing lowers the cost of production and helps insulate Chinese OEM supply chains from external shocks.

At the same time, China’s growing capacity and cost-competitiveness encourages foreign OEMs to source cheap legacy chips from China while focusing resources on cutting-edge tech development. This dynamic could fuel concerns among US policymakers about supply chain dependencies on China in “legacy tech” areas. A recognition of these risks was behind a $10 billion allocation in the US Chips and Science Act for legacy chip manufacturing. But if the United States and partner countries want to outpace China in this market segment, it will take time, resources and a political tolerance of higher prices. For perspective, in the next 3-5 years China is due to add nearly as much new 50-180nm wafer capacity (900.000 wspm) as the entire rest of the world (1.1 million wspm).

Moreover, even if the US chose to focus on steering the sourcing of legacy chips away from China, it would still have to reckon with risks to chip manufacturing in Taiwan—critical to US and partner foundry capacity—due to the possibility of a cross-Strait crisis. Assuming planned fab expansions come to fruition within the next five years, Taiwan will continue to be home to 39% of 20-45nm and 24% of 50-180nm foundrycapacity globally.

China’s Attempts to Move up the Chip Value Chain

Beyond capacity buildouts, there are other factors to consider when assessing China’s competitiveness in mature process node manufacturing. Here we examine the growth drivers and barriers for China in moving up the value chain in three distinct semiconductor markets: general purpose microcontrollers, automotive semiconductors, and mobile chipsets for smartphones and tablets.

General purpose microcontrollers

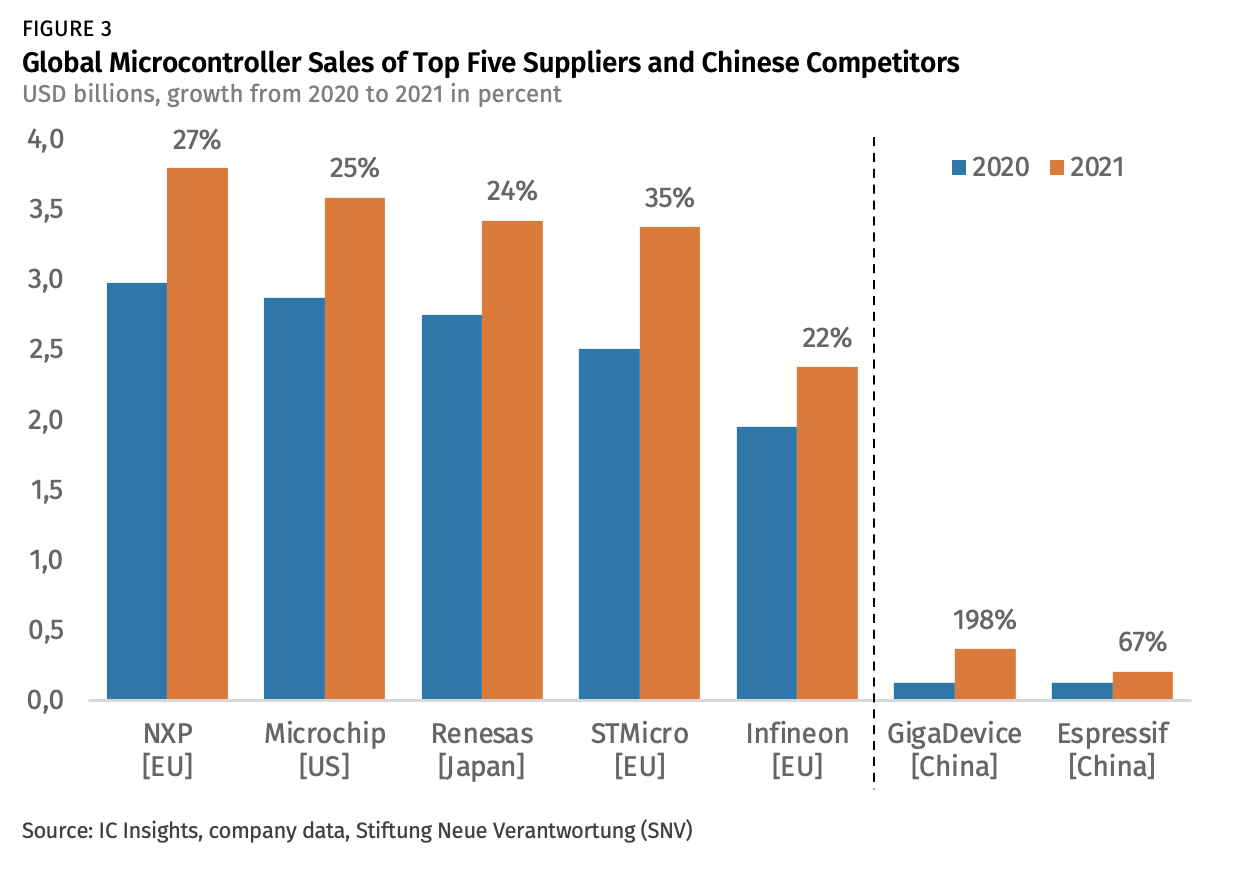

Microcontrollers are essentially tiny computers on a single chip that are used to measure, sense, control and compute almost everything in our environment. They are indispensable to modern consumer electronics, cars, agriculture, energy grids, hospitals and countless other applications. Global microcontroller sales reached $20 billion in 2021 and the leading (by revenue) five suppliers controlled 82% of the market. No Chinese company sits among the ten largest microcontroller suppliers (Figure 3).

Most modern microcontrollers are produced on mature nodes at 20-180nm and have computing frequencies several orders of magnitude lower than, for example, mobile chipsets (measured in megahertz versus gigahertz, respectively). Competition in microcontrollers is mainly driven by three factors:

- Features and level of integration: The more features a microcontroller offers, the more versatile the product. Modern microcontrollers are highly integrated devices using multiple interfaces, communication protocols, digital and analog inputs and outputs, timers and much more.

- Development environment and support: Microcontrollers are programmed with specialized software. The better the software stack (measured by ease of use, documentation, support services, etc.), the easier it is for developers to program the microcontroller. This dynamic also creates lock-in effects: developers who are familiar with certain microcontrollers and their software stack may be reluctant to switch to an unfamiliar supplier.

- Cost: Since microcontrollers are often used for simple tasks, compared to high-performance cloud accelerators or mobile chipsets, costs are a competitive differentiator.

Chinese microcontroller suppliers are starting from a low base in market share but have several advantages that could propel growth. First, the rise of China’s consumer electronics, home appliances and Internet of Things companies, such as DJI, Haier or Xiaomi, are already expanding the total addressable market for Chinese microcontroller suppliers. Second, Chinese companies, along with foreign companies trying to preserve their market share in China, may be more compelled to source from domestic microcontroller manufacturers due to the threat of US export controls and with state pressure rising on firms to advance “self-reliance” policies. Third, supply chain disruptions are encouraging Chinese and foreign companies alike to seek out a more diverse set of suppliers.

Integration and interoperability will be critical to Chinese firms’ ability to grow microcontroller market share. The product strategy of China’s largest microcontroller supplier, GigaDevice is a case in point. The company’s GD32 microcontrollers are compatible (and often directly interchangeable) with Europe’s STMicroelectronics’ STM32 microcontrollers. During the pandemic-era global chip shortages, GigaDevice used its “pin-compatible clones” to fill in supply gaps left by STMicrolectronics, which at the time was reporting a production lead time of 52 weeks and longer for most STM32 microcontrollers. GigaDevice timed the product slip-in strategy well: the company’s microcontroller revenue tripled, from $122 million in 2020 to $363 million in 2021. That said, Chinese microcontroller companies are not all mere copycats: Espressif, which went public on the Shanghai Stock Exchange in 2019, develops competitive microcontrollers produced on TSMC’s 40nm node and has rapidly gained popularity due to the product’s Wifi and Bluetooth integration.

Automotive Semiconductors

Modern cars contain hundreds of semiconductors, including microcontrollers, power semiconductors, sensors, and memory chips. The transition to electric vehicles is set to turbocharge demand for automotive semiconductors: a typical electric vehicle contains more than $1,000 worth of semiconductor content, compared to around $330 in semiconductor value for conventional vehicles, according to the US International Trade Commission.

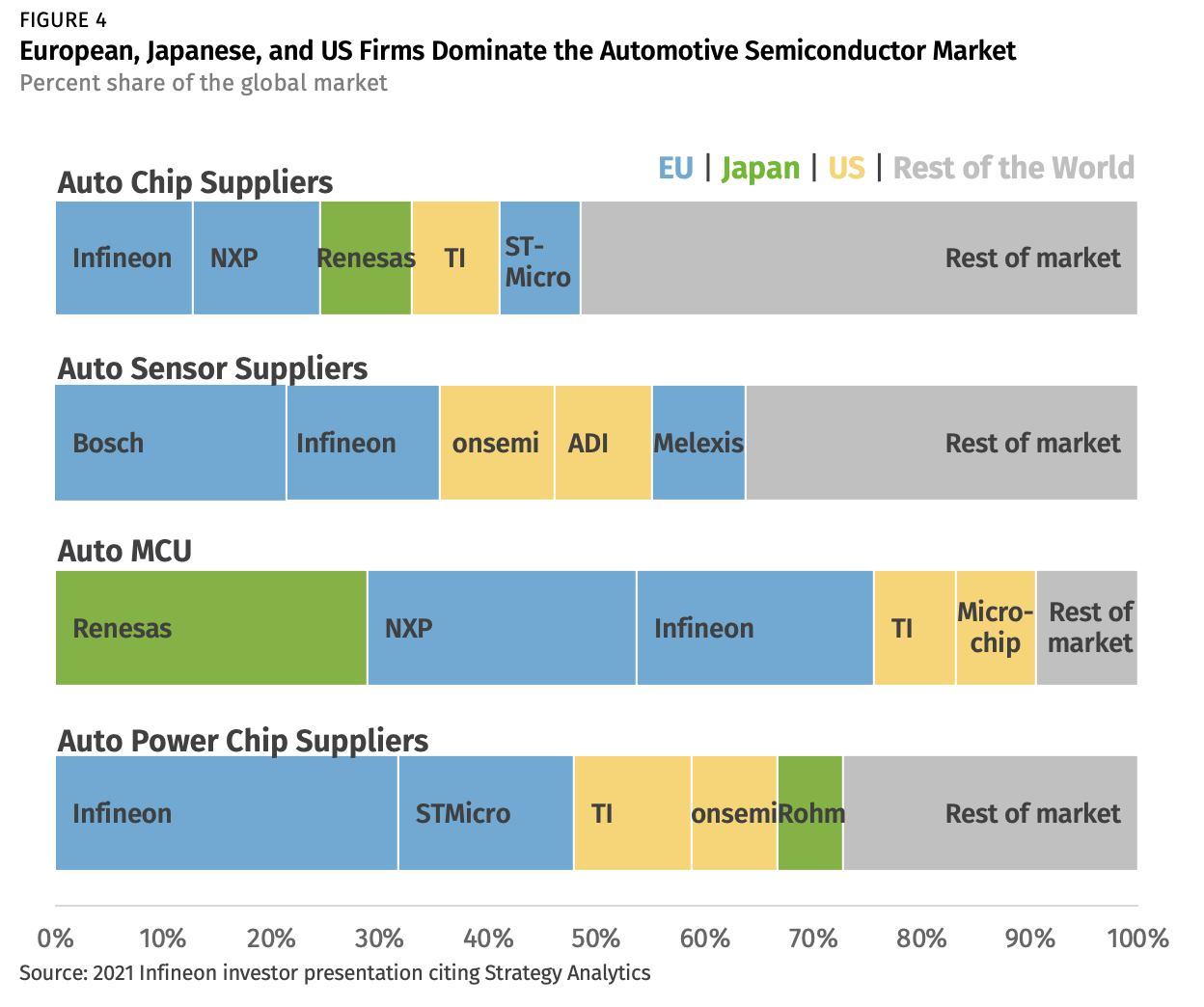

Not surprisingly, the largest (by revenue) automotive chip suppliers in the world are in Europe, Japan, and the US, where suppliers compete across multiple sub-segments in well-established auto manufacturing hubs (Figure 4.) For now, Chinese automotive chips are used in international markets for simpler functions, such as seat control, water pumps or lighting, but China’s first-mover advantage in NEVs creates new opportunities for China’s automotive chipmakers to move up the value chain.

Key barriers to entry must nonetheless be crossed for China’s automotive chipmakers to make a serious dent in this fast-growing market, namely:

- Safety-certification: Automotive chips need to meet several safety certification requirements to be eligible for sale to automotive OEMs. This requires a strong understanding and close coordination with the design and manufacturing process. Moreover, automotive OEMs push their supply chain toward “zero defects” (defect rates for modern vehicles are in the range of 10 defective parts per billion).

- Long product life cycles: Since the average life cycle of a car is around 15 years, automotive chip suppliers need to guarantee supply and performance of specific chips for several years in the production cycle. As a result, automotive OEMs place a lot of trust in their chip suppliers and employ extensive qualification processes before a new supplier is incorporated into the supply chain.

Share Figure

Chinese companies have seen the most growth so far in the automotive microcontroller market, with more than 20 Chinese companies, including BYD, ChipON, Geehy, and GigaDevice, developing automotive-grade microcontrollers. While Chinese-made automotive microcontrollers are mostly used today for simple functions, there are several factors that could move Chinese firms up the value chain to grow domestic and global market share. These include:

- Growing presence of Chinese OEMs: More than 80% of China’s EV market is controlled by domestic companies, such as BYD, Wuling, Changan and Geely. These Chinese EV OEMs are more likely than foreign auto OEMs to source from domestic auto chip suppliers. For example, ChipON (founded in 2012 and planning an IPO) has developed its own IP for automotive and industrial microcontrollers and has received funding from several Chinese automotive OEMs. As in Europe and Japan, China is counting on close collaboration between Chinese car OEMs and domestic auto chip suppliers to grow both sectors in tandem.

- Automotive chip shortages: While many semiconductor markets experience oversupply, automotive chips have so far been the exception. Many automotive chips are expected to remain in short supply throughout 2023, potentially even longer. As a result, automotive OEMs are trying to source from multiple suppliers to boost supply chain resilience. This creates an opportunity for new auto chip suppliers, including Chinese firms, to enter the market.

- Geopolitical buffer: Chinese auto OEMs may be concerned about the potential for US-led export controls to spread to certain types of automotive chips with US-origin technology (for example, by targeting silicon-carbide power semiconductors). This creates another incentive for Chinese auto OEMs to look to domestic auto chip suppliers to ensure business continuity. Foreign automakers looking to protect market share in China and become more competitive in the NEV space may also be compelled to source from local Chinese suppliers. For example, Volkswagen Group and its software company CARIAD announced a joint venture with Horizon Robotics in October 2022. China’s state-backed investments to draw in foreign investment may also include conditions obliging foreign auto OEMs to raise local technology content.

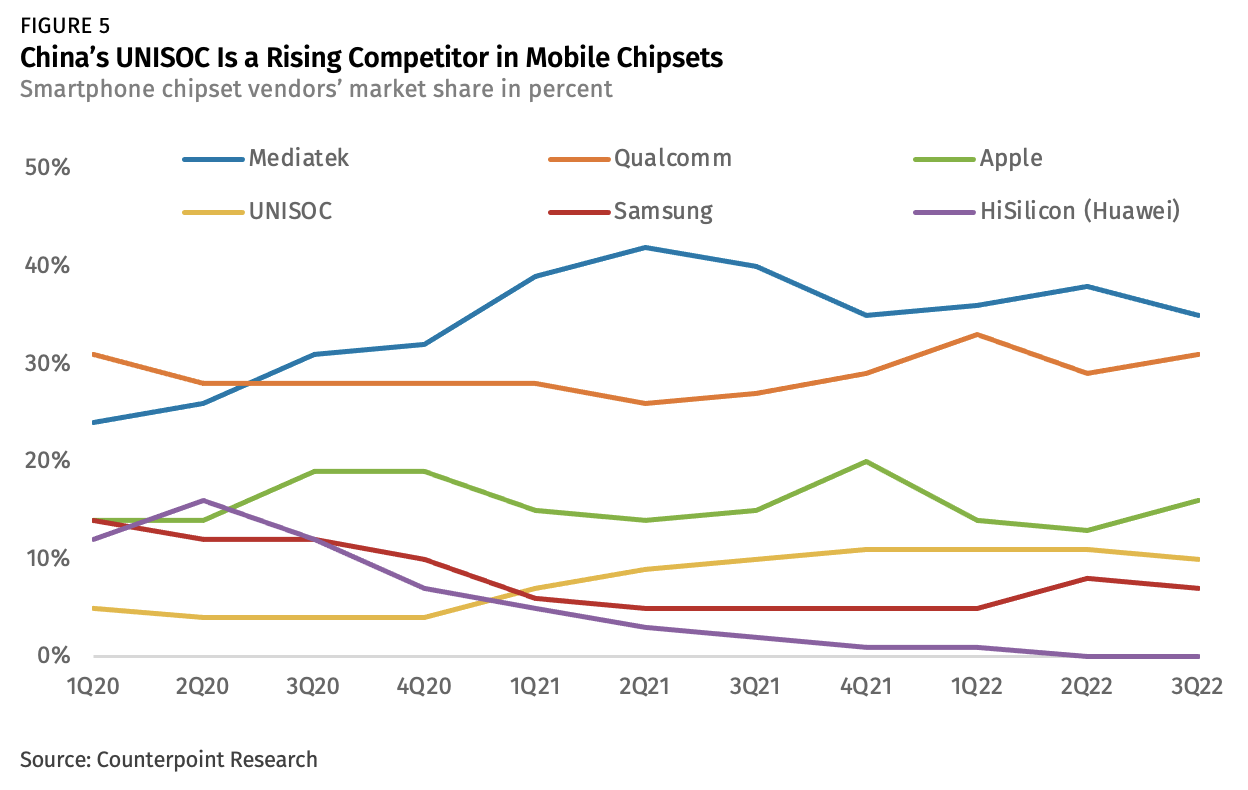

Mobile Chipsets

The raw computing power of mobile chipsets in smartphones and tablets is well below the compute performance thresholds set out in the Oct. 7 US controls. But since mobile chipsets depend heavily on node shrinkage for performance gains, Chinese mobile OEMs cannot escape their heavy dependence on foreign foundries to manufacture leading-edge chips. For example, Chinese mobile chipset manufacturer UNISOC depends on TSMC’s 6nm EUV manufacturing for its flagship T820 mobile chipset. Despite this significant vulnerability, there is room for Chinese mobile chipset makers to increase their market share.

Competition in smartphone chipsets is mainly driven by cost, performance, and fast-paced innovation. Apple is the exception on cost: while Apple’s iPhones capture less than 20% market share, Apple has made 80% of the profits in the global smartphone market since 2015. With the exception of Apple, cost tends to have a substantial impact on the competitiveness of smartphone manufacturers and the chipset market more broadly.

The global mobile chipset market today is led by Mediatek (Taiwan) and Qualcomm (US), followed by UNISOC (China) and Samsung (Korea). Apple does not sell its own mobile chipsets on the open market. After smartphone manufacturer Huawei was targeted with hard-hitting US export controls starting in 2019, UNISOC gained market share at the expense of Huawei-owned HiSilicon. The company’s global mobile chipset market share more than tripled, from less than 3% in 2019 to more than 10% in 2022. UNISOC’s biggest customers are Chinese handset OEMs Oppo, Vivo, and Xiaomi. These companies are also investing in in-house chip design and could see their market share grow in the mobile chipset space within the decade. Samsung has more recently begun using UNISOC chipsets in its entry-level tablets and smartphones.

Looking forward, Chinese mobile chipset designers will face hurdles in keeping pace with foreign competitors due to multilateral restrictions on cutting-edge chip design software. In August 2022, the Wassenaar Arrangement imposed licensing restrictions on electronic design automation (EDA) tools that are capable of designing next-generation transistor structures (Gate-All-Around Field-Effect Transistors or GAAFETs). As a result, US EDA suppliers, such as Synopsys and Cadence, have been shipping restricted versions without GAAFET-capabilities to Chinese customers since November 2022. Without access to these crucial chip design tools, Chinese mobile chipsets designers will likely be stuck at (roughly) 3nm process nodes.

Beware of US Entanglements

Chinese semiconductor companies have room to expand in areas so far untouched by US-led export controls, but the risk of US entanglements looms for any OEM considering the adoption of Chinese-made chips. For as much as the Oct. 7 controls focused on high-performance computing and cutting-edge logic chips, they also exposed US anxiety about supply chain dependencies on China more broadly.

For instance, the Oct. 7 controls went beyond restrictions on the production of leading-edge logic chips, where China remains far behind the US and partners, to also cover (largely commoditized) memory chips, where China had been gaining market share. Specifically, the US tied advanced memory chips (defined by the US as chips with 128 layers or more for NAND and 18nm half-pitch or less for DRAM) to weapons of mass destruction (WMD) end-use to justify comprehensive licensing restrictions on manufacturing tools and software.

Japan and European partners are aligning with the US on export controls targeting advanced logic chip production but are unlikely to adopt the US national security argument for memory chips. Even so, the US was able to leverage unilateral export controls to knock China’s YMTC out of the competitive 3D NAND flash memory market. YMTC was steadily gaining market share (capturing almost 5% of global NAND sales by some estimates) until it was hit by the Oct. 7 controls and subsequently added to the BIS Entity List in Dec. 2022. Chinese state-backed funders have since thrown YMTC a USD $7 billion lifeline but cash infusions do little to solve the firm’s challenge in sourcing non-US-origin software and tools.

The memory chip example raises a critical question for both Chinese and foreign OEMs trying to weigh the pros and cons of sourcing chips from China: will US-led controls extend into other commercial areas where a national security argument can be stretched to undercut Chinese tech competitors, even if those companies are operating well below US-defined performance compute thresholds in more mature market segments?

As geopolitical competition between the United States and China intensifies (in part from growing US-led tech and investment controls), some US policymakers are drawing attention to China’s “coercive leverage” in supplying inputs (including legacy chips, active pharmaceutical ingredients, solar cell and battery technologies, and critical materials) that pervade consumer and industrial applications. This concern is translating into calls for tighter controls to steer supply chains away from China.

The US has an expanding toolkit to address its supply chain concerns. These include:

- The tightening of existing export controls on China-based, foreign-owned fabs: South Korean leading edge memory chipmakers Samsung and SK Hynix could have their one-year licenses revoked (or threatened to be revoked) if the US assesses that these firms are not moving quickly enough to diversify advanced memory chip production away from China. At the same time, prematurely shuttering Samsung’s and SK Hynix’s memory fabs in China would risk significant price fluctuations and disruptions to the global memory chip market.

- Scaling up export controls and sanctions against Chinese tech entities: A number of justifications may be used against Chinese OEMs and chip suppliers, including sanctions violations, dual-use applications, data security and cybersecurity concerns, and human rights abuses. SMIC is already on the BIS Entity List, but could face tighter restrictions still. A pending US move to further restrict export licenses on Huawei, already battered by the foreign direct product rule (FDPR), illustrates how a sliding scale of controls can reach into mature tech markets.

- Expanding list-based export controls to less sensitive technology areas: The caveat here is that partners could be reluctant to align with the US on controls in commoditized markets. This would increase the risk of foreign firms growing their market share in China at the expense of US companies. This is one of the key considerations Commerce BIS regulators are supposed to factor in when crafting restrictions.

- Tightening conditions on US chip industrial policy: The US CHIPS Act of 2022 gives considerable authority to the Secretary of Commerce to adjust guardrails and claw back funding from recipients. The March 21 Commerce Notice of Funding Opportunity contained several key provisions, including stringent restrictions on recipients’ ability to expand manufacturing capacity in China (not to exceed 5% and covering an additional category of “semiconductors critical to national security” to account for materials science breakthroughs in China). Recipients are also not permitted to “knowingly engage in any joint research or technology licensing effort with a foreign entity of concern that relates to a technology or product that raises national security concerns.” This is an intentionally broad provision designed to get companies to first report relevant transactions to Commerce, which will then use that information to refine the restrictions.

- Restrictions aimed at safeguarding US Information and Communication Technologies (ICT) supply chains: The recently-introduced White House-backed, bipartisan RESTRICT Act deliberately takes a comprehensive approach to targeting foreign entities of concern tied to any US ICT products or services that could pose a risk of sabotage or subversion, catastrophic impacts on critical infrastructure, election interference, subversion of democratic processes, or (a catch-all) risk to the national security of the US or safety of US persons.

- Procurement and investment restrictions tied to subsidy support: The US Merger Filing Fee Modernization Act of 2022required firms pursuing M&A deals with foreign entities of concern to disclose to the Federal Trade Commission information on any subsidies received by that foreign entity. The EU is ahead of the US in this trend: the Foreign Subsidies Regulation, which entered into force in early 2023, empowers the European Commission to investigate whether any company operating in the EU has received any form of direct or indirect financial subsidy from a non-EU country. If the Commission concludes such support has had a market-distorting effect, it can impose mitigating measures, block deals, and even force the dissolution of tie-ups.

- Inbound and outbound investment screening: The US and a number of partner countries are examining whether investments, such as mergers, acquisitions, or partnerships, have the potential to increase critical supply chain dependencies on China. If such risks are identified, deals could be blocked on national security grounds. A looming executive order from the White House is expected to prioritize semiconductors as the US takes its first steps toward developing a notification and potential blocking mechanism for outbound investments in “force-multiplying” technologies.

Entering a Dark Forest

US-led restrictions on China’s chipmakers will force Beijing, local governments, and corporate boardrooms to make some tough decisions as they consider where best to focus their money, talent, and time in order to get China’s chip industry out from under Washington’s thumb. The highest levels of government may tout self-reliance as the number one task for Chinese chipmakers trying to break free of US-origin tech entanglements. But semiconductor value chains are simply too complex and interconnected for any one country to become entirely self-sufficient. And there are no short cuts when it comes to developing cutting edge chips.

A strikingly sober assessment of China’s chip industry published by the Chinese Academy of Sciences (CAS) noted that China has mistakenly assumed it could develop its chip sector without investing in basic R&D to develop next generation transistors. China, the article notes, “the US turned off the lighthouse” and “we have now entered a dark forest” when the United States decided to choke off supplies of critical software and tools. Beijing is now scrambling for a solution, with calls ranging from boosting basic R&D and industrial policy funding to appointing “supply chain chieftains” to oversee the industry’s development.

But more funding, restructuring, and talent poaching is unlikely to bridge the large gaps in China’s development of cutting-edge chips. China has already committed to investing around $150 billion between 2014 and 2030 to grow its chip industry. And yet Chinese semiconductor firms are producing only around 7% of the chips China consumes —far short of Beijing’s target to achieve self-sufficiency rate of 70% by 2025. On top of high technical barriers, intensifying export controls, and intricately woven supply chains favoring the US and its security partners, China must also contend with tightening fiscal pressures, amid a structural economic slowdown, and a record of waste and corruption in its Big Fund industrial policy as it tries to formulate a policy response.

The temptation to follow the path of least resistance is likely to grow as China’s economic stresses deepen. There is a vast commercial chip market where Chinese chipmakers (for now) are free to compete and where Chinese industrial end-users will be geopolitically motivated to boost domestic chip content. US tech companies trying to preserve market share via “in China for China” policies face a web of competing pressures as a result: growing state pressure in China to adopt homegrown chips, heat from US policymakers trying to decouple US-China tech supply chains, and competition from foreign firms whose host governments have little interest in extending restrictions into more commoditized market segments.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}