matdesign24/iStock via Getty Images

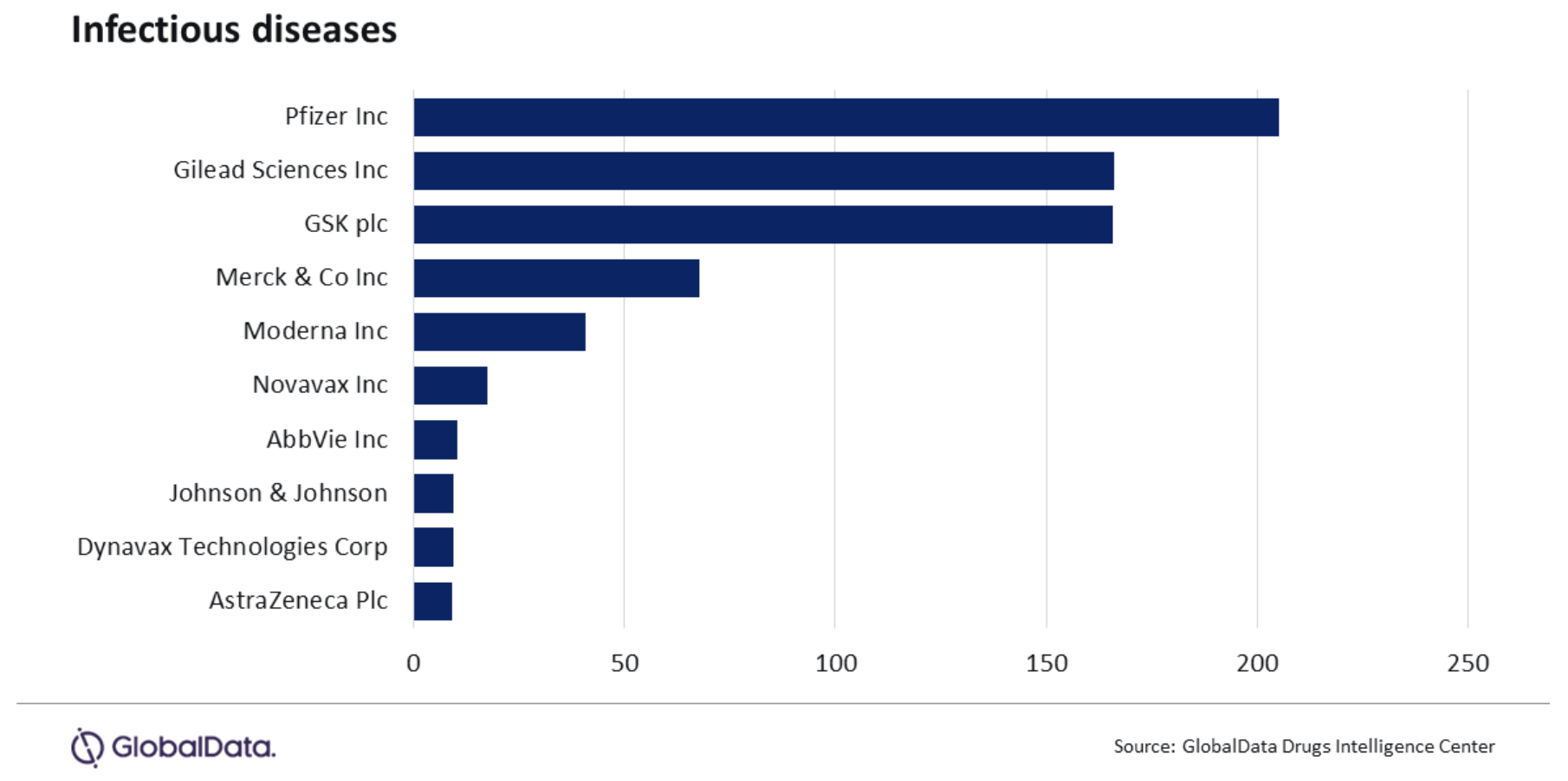

Pfizer (NYSE:PFE), Gilead Sciences (GILD), and GSK (GSK) are in position to control a majority of the infectious disease treatment market due to increasing demand for COVID-19 drugs and HIV medications.

That’s the assessment from analytics and consulting firm GlobalData, which forecasts a CAGR for the market of 5.7% between 2023 and 2029.

The firm added that the infectious disease treatment market will reach $150B by 2023 with the three pharmas controlling 62% of it.

While some might be surprised to see Pfizer (PFE) have such a dominating position in infectious disease treatment given the decline of COVID in the US and many other countries, GlobalData pharma analyst Kevin Marcaida said its COVID vaccine Comirnaty and antibiotic Paxlovoid are still showing strong sales. He added that price hikes planned for the new version of the shot and the incidence of COVID-19 in poorer countries will continue to buoy sales of these two products.

Mercaida noted that Comirnaty and Paxlovid are estimated to bring in $122B in sales between 2023 to 2029.

Pfizer (PFE) will also likely benefit from its recently approved respiratory syncytial virus vaccine, Abrysvo, in those 60 and older. In phase 3, the drugmaker has aztreonam/avibactam for infections due to Gram-negative bacteria with limited or no treatment options.

Meanwhile, Gilead (GILD) is projected to have sales growth in its infectious disease franchise of 12.4% between now and 2029 driven by sales of HIV drug Biktarvy (bictegravir/emtricitabine/tenofovir), which brought in ~$2.7B in Q1 alone. It is projected to contribute $92B in sales between 2023 and 2029.

In the coming years, Gilead (GILD) is also likely to benefit from growing sales of its new HIV medicine, Sunlenca (lenacapivir), which hit the market in January. After initial dosing, Sunlenca is given just twice a year.

In the late-stage pipeline, Gilead (GILD) has obeldesivir in phase 3 as a COVID therapy. For hepatitis delta virus, it has an application pending with the FDA for Hepcludex, and in phase 3, bulevirtide as another HDV candidate. In phase 2, Gilead (GILD) has selgantolimod as a potential hepatitis B cure.

GSK (GSK), meanwhile, will benefit in particular from two treatments: The shingles vaccines Shingrix and the HIV drug Dovato (dolutegravir/lamivudine). The former is projected to generate total sales of $4B between 2023 to 2029, according to GlobalData.

Dovato is made by ViiV Healthcare, of which GSK (GSK) is majority owner. The HIV med is projected to bring in $20B during the period.

Like Pfizer (PFE), GSK (GSK) will also benefit from sales of its recently CDC-backed RSV vaccine. Although the recommendation from CDC is for those 60 and older, the shot will likely get approval for other demographics in coming years.

In the late-stage pipeline, the British drugmaker also has gepotidacin for urinary tract infections and gonorrhea; bepirovirsen for chronic hepatitis B; and tebipenem pivoxilv for UTIs.

More on infectious disease treatments

Pfizer posts promising Phase 3 data for AbbVie-partnered antibiotic

Pfizer, BioNTech start trial for first mRNA-based shingles vaccine

Gilead wins EU nod for full approval of hepatitis delta virus therapy

GSK oral UTI antibiotic meets key goals in late-stage trials

GSK to invest £1B in R&D to fight infectious diseases in lower-income countries

{kind=link}