Back in June, Republican senators were yelling at Janet Yellen about giving the US economy a “sugar high” via short-dated debt. Smart people at JPMorgan, Barclays and Apollo worry that the government’s reliance on T-bills to fund the deficit risked a rerun of the 2019 repo crisis.

The latest salvo is a paper from Trump-era Treasury official Stephen Miran and economist Nouriel Roubini, who argue that borrowing skewed more towards short-term debt is tantamount to “stealth quantitative easing” and is interfering with the Fed’s ability to fight inflation:

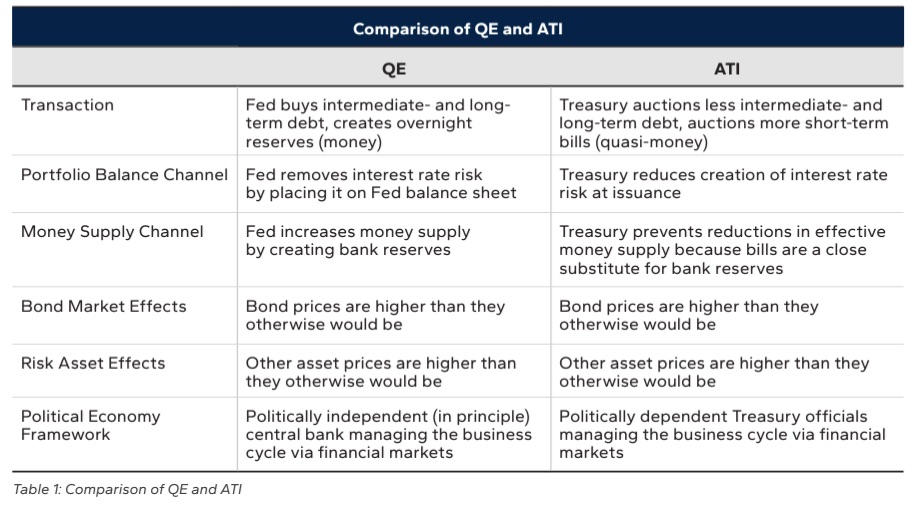

By adjusting the maturity profile of its debt issuance, Treasury is dynamically managing financial conditions and through them, the economy, usurping core functions of the Federal Reserve. We dub this novel tool “activist Treasury issuance,” or ATI. By manipulating the amount of interest rate risk owned by investors, ATI works through the same channels as the Fed’s quantitative easing programs.

ATI has been a major market driver over the past year and we expect it will continue to play a significant role in the years ahead; ATI may become a regular element of the policy toolbox, driving political business cycles in the market and the economy.

. . . Contrary to the Fed’s insistence that monetary conditions are quite restrictive, they are not, and Treasury’s issuance policies help explain the persistence of inflation and strong economic growth.

Blood pressure already raised, next week’s quarterly refunding announcement — in which the Treasury department makes public their borrowing plans for the coming three months — could make budget hawks faint.

The US is borrowing boatloads of money at the moment. The budget deficit really started to expand under president Trump, who drastically cut taxes, and it has ballooned since as Washington has spent on Covid-19 measures, the recovery, domestic programmes and aid to Ukraine and Israel. Interest expenses are adding to the tally too, with rates at 23-year highs.

The Congressional Budget Office in June said they were expecting the deficit to reach $1.9tn this year, up from a February estimate of $1.5tn. That could mean hundreds of billions in additional debt issued in the coming three months.

As Ajay Rajadhyaksha, global chair of research at Barclays and occasional Alphaville blogger memorably put it to mainFT: “We are spending money as a country like a drunken sailor on shore for the weekend.”

Low taxes and more spending has meant tons of Treasury bonds on offer. Last August, the government said it was going to dramatically increase the size of its longer-dated bond auctions. The market freaked out and sent yields higher. Since then, they’ve instead opted to issue lots more Treasury bills — bonds that mature in anywhere from a week to a year.

It’s a plot that has been largely successful, in part because there’s been no shortage of demand. Yields are high on these ultra-safe, ultra-liquid bonds and investors, including money market funds, have had loads of capacity to gobble up the supply.

But the share of bills as a percentage of marketable debt outstanding has risen to around 22 per cent, above the range of 15-20 per cent recommended by the Treasury Borrowing Advisory Committee, a body of bankers, big investors, hedge fund managers and traders that meets quarterly with the Treasury. That might rise further in the coming quarter, given the CBO’s rising deficit estimates.

Miran and Roubini argue that anything above 18 per cent constitutes “activist Treasury issuance” and the “missing” long-term debt has reduced the 10-year Treasury yield by 0.25 percentage points over the past year, and is the equivalent to 1 percentage point in interest rate cuts.

Here’s their comparison of the effects of QE and ATI:

Notably, they estimate that bill supply as a percentage of outstanding debt has ranged between 34 and 60 per cent over the past few quarters, and argue that this is actively working against the Fed’s disinflationary programme.

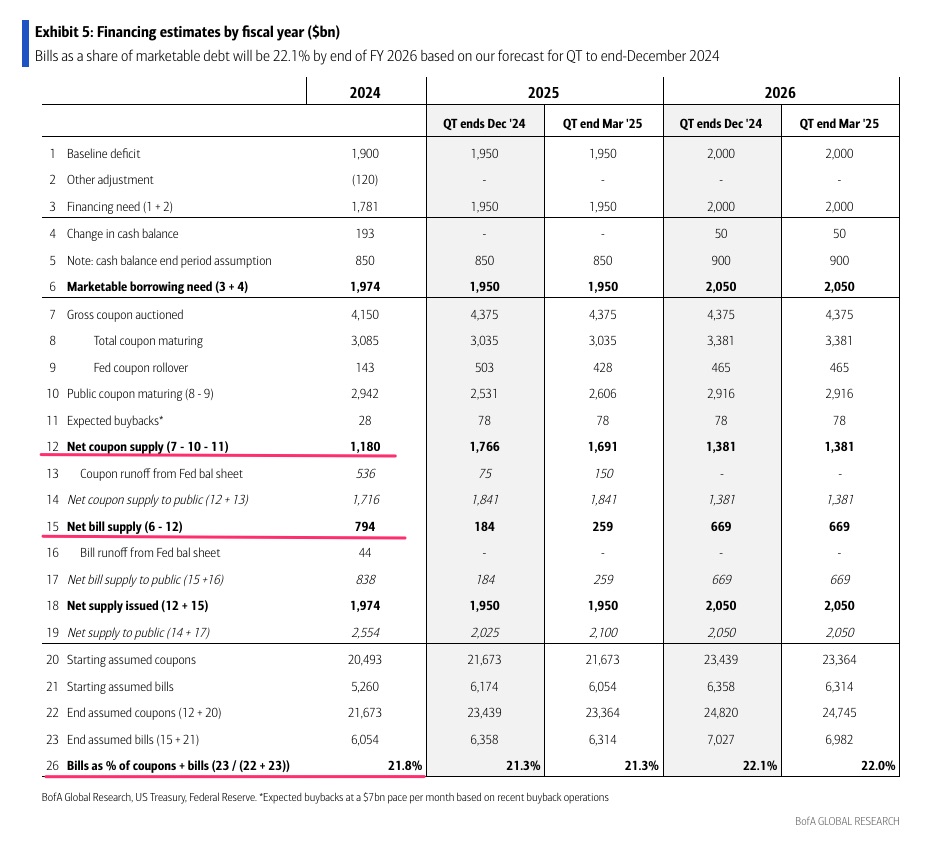

Here are Bank of America’s estimates for 2024 and breakdown of debt issuance over next few years. As you can see they estimate that bills will account for about 40 per cent of net Treasury issuance this year (zoomable version), but that will still leave the overall outstanding share of bills to overall Treasury debt at a shade under 22 per cent by the end of 2024.

The Fed itself has engaged in efforts like “Operation Twist” a few times, where they have skewed their bond-buying to favour one end of the curve in order to control the shape of the yield curve. But, notably, that was directed by the Fed, and not the Treasury.

There are a few immediate questions this argument raises.

Yes, skewing issuance towards T-bills has certainly had some effect on pricing in the market. As you can see from the chart above, long-term bond yields rose after Treasury announced the ramped up auction sizes back in August, and cooled off after the department said it had changed that plan.

But those moves were small compared to the impact that the shifting inflation outlook and interest rate policy has on yields. In practice it’s difficult to exactly decompose the different effects. But it’s clear that bond vigilantes aren’t punishing the US for excess borrowing the way they maybe used to.

Calling this “stealth” QE or “activist” Treasury issuance also implies a political project, but preventing freak-outs in markets is a bipartisan pastime.

Fiscal spending and tax cuts are inherently political, but the deficit has grown significantly under both the Trump and Biden administrations, just by different mechanisms. Ensuring that the expansion of those deficits — voted on by Congress, not Treasury — happens in an orderly way is standard Treasury business.

Don’t forget, its borrowing plans are formed with advice from TBAC, which is mostly a bunch of big investors like Vanguard, Pimco and BlackRock, and senior traders at hedge funds like Element Capital, Rokos Capital or the big banks. It’s chaired by Deirdre Dunn, head of global rates at Citigroup. At last autumn’s meeting they were supportive with the Treasury twisting supply towards bills:

The Committee expressed continued comfort with the bill share of total marketable debt outstanding remaining temporarily above its recommended range given continued robust demand for bills and Treasury’s regular and predictable approach.

And at their last meeting, TBAC advised the Treasury’s debt management office to basically stay the course.

Miran and Roubini’s suggestion that anything above 18 per cent T-bill issuance is “activist Treasury policy” is a bit weird, given that it’s right in the middle of TBAC’s recommended range (which has only been around for a few years anyway). The suggestion that “ATI may become a regular element of the policy toolbox, driving political business cycles in the market and the economy” also doesn’t mesh with the fact that the share of T-bills has always fluctuated around the pretty-new recommended band, rather than inside it.

Or are they suggesting that the Obama administration was trying to do “stealth” QT for much of 2010-2020?

The reality is that the US debt management office simply skews issuance a little towards where they think capacity is greatest and the US government can get the best deal. When rates are higher, they usually go shorter, and when they’re lower they go long — all within the “regular and predictable” framework, naturally.

It should be noted that the weighted average maturity of the US government’s debt burden has actually increased markedly over time, with the recent skew towards bills still leaving it near the highest in modern times.

Finally, the question of whether a skew in Treasury issuance maturity is comparable to quantitative easing is interesting, but hard to answer based on effects.

The exact effects of quantitative easing on the real economy are not agreed on, to put it mildly. While QE is understood to be stimulative and QT is understood to tighten financial conditions, arguments about the extent of those effects and how exactly they might translate into interest rate policy are all over the place.

Anyway, the US government will make its latest quarterly refunding announcement on Monday, which will offer insight into how much it expects to issue in Treasury bills in the coming three months.

For now, demand for Treasury bills remains robust, and the increase in issuance hasn’t caused any evident strains in funding markets yet. You could see that demand for shorter-term debt on Tuesday this week, when investors bought up record amounts of two-year Treasury notes at auction.

Primary dealers — big banks that are responsible for buying up any supply at auction not purchased by investors — took up just 9 per cent of the $69bn in notes on offer, the lowest percentage on record, according to BMO Capital Markets. Investors bought the bonds at 4.43 per cent, 0.025 percentage point below where the bonds were trading prior to auction, another indication of strong demand.

So what will we see in Monday’s refunding announcement? More of the same, according to pretty much all the bank research FT Alphaville has seen on the topic. And they all expect this to be largely fine.

Here’s Bank of America:

Our projections suggest that near term bills as a share of marketable debt will remain above TBAC’s 20% recommended level. We do not think that this poses an issue, as bill demand remains firm and bills versus OIS remain in recent ranges. Money fund inflows have remained robust, with the yield curve still inverted/flat. Bill demand will also be supplemented by MMF reform supporting higher government fund AUM. UST could decide longer term to allow a longer-lasting overshoot of bills from the recommended 15-20% range, but we would expect a more thorough discussion with TBAC and market participants first. The debt limit, which comes back into effect on January 1, 2025, would likely lead to large bill paydowns in 1H’25

JPMorgan:

The fiscal picture has deteriorated somewhat and we now project a $1.915tn deficit in FY24, but this estimate overstates the increase in projected outlays, as it’s partially driven by subsidy costs related to student loans. Accordingly, we think Treasury remains well financed through late FY25 and therefore the guidance Treasury provided in May, that it “does not anticipate needing to increase nominal coupon or FRN auction sizes for at least the next several quarters,” remains appropriate.

Indeed, Treasury has created nearly $600bn in additional borrowing capacity for FY25 relative to FY24 and the current auction schedule leaves Treasury well financed though next year. Accordingly, we look for nominal auction sizes to remain stable at current levels for the balance of this year, though we project further modest increases to TIPS auction sizes

And Goldman Sachs:

We expect Treasury to feature a somewhat higher issuance trajectory at next week’s refunding meeting compared to last quarter, reflecting higher deficit projections. We think T-bill issuance will absorb the increase in financing needs for now, and anticipate no changes to coupon auction sizes for Q3.

We don’t think Treasury needs to discard its previous guidance that it “does not anticipate needing to increase nominal coupon or FRN auction sizes for at least the next several quarters” just yet. Risks are, however, that it softens that language given elevated deficits, but such an adjustment might be paired with emphasis that the 15-20% recommended range for the bill share is not a binding one.

The deficit outlook is likely to warrant considering coupon size increases before too long, however. We think a reasonable timeline would be to begin discussions in 1H25, with a series of gradual increases starting in 2H25 that would stabilize the bills share around the top of the 15-20% range by 2H26.

In other words, it’s a really interesting paper you should give a read, but probably not something we need to freak out about.

{kind=link}

{kind=link}

{kind=link}