Hwangdaesung/iStock via Getty Images

Leading pure-play cybersecurity company Palo Alto Networks, Inc. (NASDAQ:PANW) surprised Wall Street analysts as it decided to report its fourth-quarter or Q4FY2023 earnings release on August 18 (Friday) after the market closed.

Wedbush’s Dan Ives even spooked investors that the company’s decision to release earnings on a Friday evening was a “disaster timing move for the ages.” While PANW saw significant volatility in the week, PANW closed remarkably above this week’s lows, suggesting dip buyers bought late into the week’s close.

Following last week’s futile buying attempt to bottom out, this week’s price action is constructive, indicating dip buyers weren’t unduly concerned with Wedbush’s “disaster” theme.

I assessed much of PANW’s near-term downside has been reflected following the early August crash led by Fortinet’s (FTNT) shocking release. As such, operators have astutely attempted to price in near-term downside heading into Palo Alto Networks’ FQ4 scorecard, expecting a tepid performance from the cybersecurity leader. While PANW’s short-term price action indicated a possible bottoming set-up, its long-term price action suggests it could entail further downside volatility.

Since I didn’t have exposure heading into Palo Alto Networks’ earnings card, I added exposure on August 10, taking advantage of its recent downside volatility. However, I didn’t add my full allocation into PANW, anticipating an improved risk/reward level if PANW couldn’t attract sufficient buyers back after its earnings release.

Therefore, yesterday’s remarkable FQ4 report by management telegraphed the company’s robust underlying growth drivers ahead of its peers. Palo Alto Networks posted a solid card, with revenue up 26% YoY in Q4. The company reported billings growth of 18%, which was lower than its full-year metric of 23%. As such, the increased deal scrutiny and macroeconomic uncertainties were also felt in Palo Alto Networks’ recent performance, suggesting it wasn’t immune to these headwinds.

Management also alluded to these challenges, worsened by the elevated interest rates, leading to higher cost of capital issues its customers face. Despite that, RPO growth remained robust, up 30% YoY in FQ4.

Notably, the company posted solid guidance for the next fiscal quarter and the full-year (FY24). Despite that, it indicates that growth is expected to slow further, although the company remains on track to report robust forward-looking metrics. Accordingly, Palo Alto Networks’ project FQ1’24 billings growth of 18% at the midpoint. However, the company anticipates a more robust full-year midpoint metric of 19.5%.

As such, investors should expect a stronger second-half acceleration in FY24, although growth is expected to normalize from FY23’s robust performance.

With that in mind, it’s vital to assess whether PANW remains an attractive stock, given further normalization in its growth profile, despite operating leverage gains. Coupled with the caution suggested by its long-term price action, investors need management to continue executing well to justify its growth premium, as seen in its “D” valuation grade, as assigned by Seeking Alpha Quant.

However, the company’s “A-” growth profile should help to sustain its premium valuation, bolstered by its best-in-class “A” profitability metric. Therefore, I believe it should provide sufficient buying support for PANW at the current levels, provided we see dip and momentum buyers returning over the next few weeks.

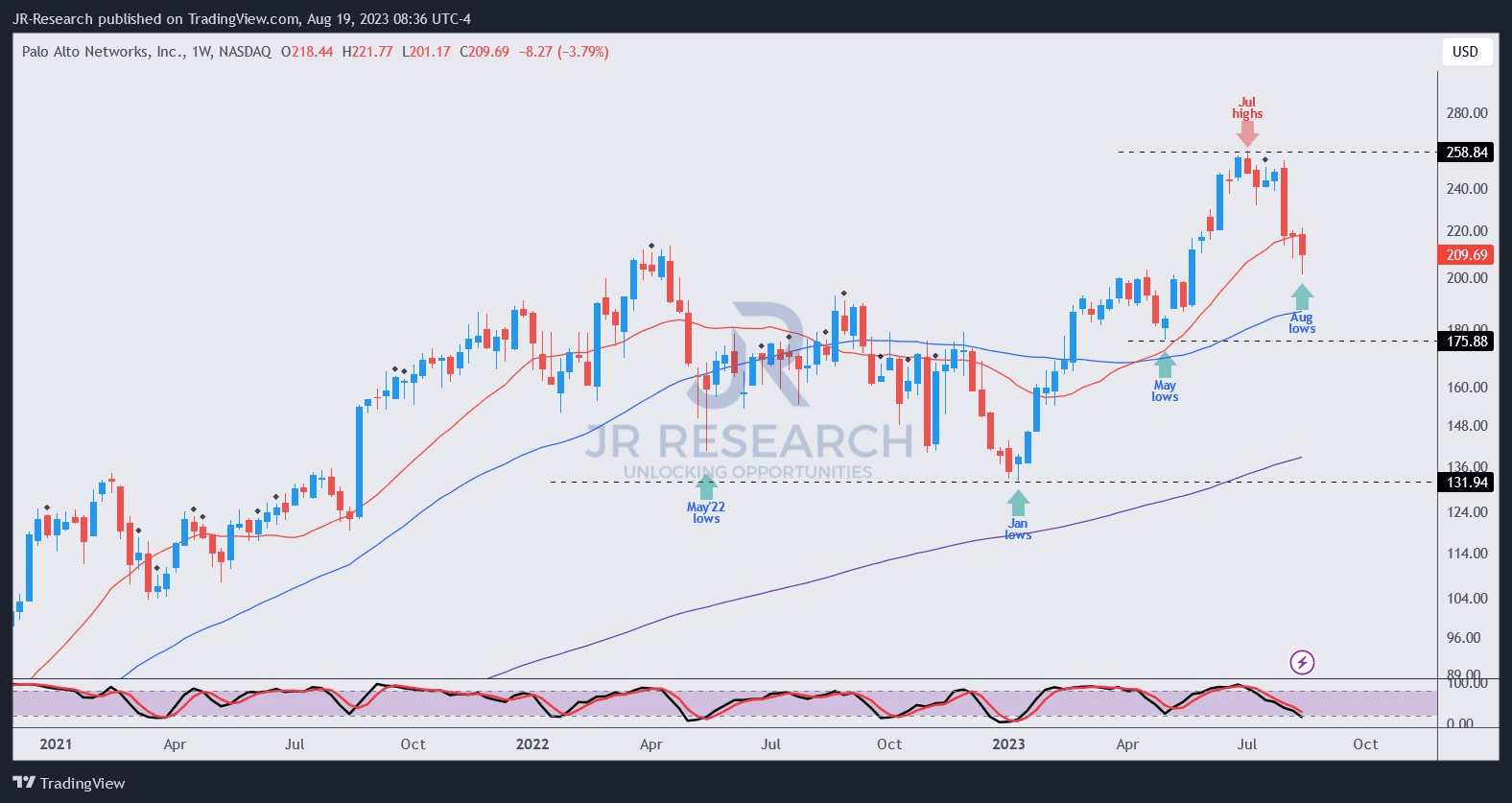

PANW price chart (weekly) (TradingView)

PANW’s medium-term uptrend remains intact despite the recent selloff. Its post-earnings sizzle needs to be followed through over the next few weeks to ascertain a continuation of its uptrend bias.

PANW’s selling intensity could worsen if buyers fail to sustain the current levels. Therefore, investors are encouraged to be cautious about adding all their intended allocation at the current levels. Given the caution in its long-term price chart (monthly), we need more clarity from buyers corroborating their willingness to defend the current support zone.

I believe buyers could be attracted to return aggressively at the $175 levels (Mar 2023 lows) if we get there. It’s much closer to my high-conviction buy levels, suggesting I could decide to add aggressively to fill my allocation if PANW falls further.

For now, I believe PANW’s near-term bottom looks constructive but needs clarity over the next few weeks. Keep spare ammo to mitigate downside risks (for averaging down), given its premium valuation and less constructive long-term price action.

Given the post-earnings surge, I believe the risk/reward is relatively well-balanced at the current levels. Hence, I will observe closely for another more attractive buy point moving ahead.

Rating: Hold. Please note that a Hold rating is equivalent to a Neutral or Market Perform rating.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

{kind=link}