JuSun/iStock via Getty Images

Summary

I am recommending a hold rating for Napco Security Technologies (NASDAQ:NSSC), as I am unsure how long it would take for the channel destocking process to be finished. It is likely that the business will continue to print weak results in the near term as it laps the tough competition from 1Q23 to 3Q23. While there is positive traction in the Doors segment, it appears that the market is focusing more on the negative aspects of recent performance, as seen from the share price action.

Business

In addition to producing digital locks, access control systems, and smoke and fire detectors, NSSC also produces electronic security devices for use in homes, businesses, schools, and factories. The Company markets and distributes its wares through a global system of distributors. The company has traditionally focused on hardware, but the connectivity services it offers in conjunction with its wirelessly enabled products are driving significant growth in the company’s monthly recurring revenue (MRR). In FY23, the sale of equipment accounts for 65% of total revenue, while services account for 35% (up from 9% in FY17).

Financials/Valuation

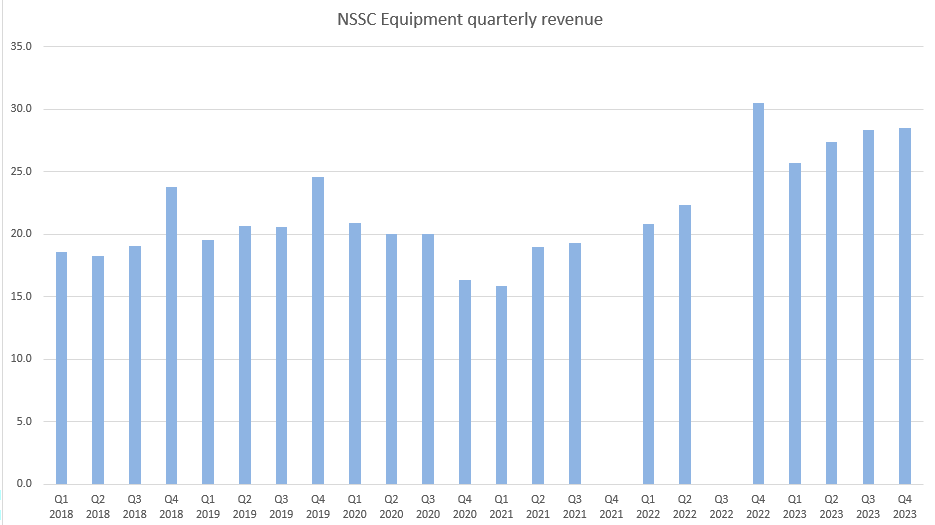

NSSC has enjoyed a surge of growth over the past nine quarters, ranging from low 20 to mid-50% growth rates, driving quarterly revenue to a height of mid-40 million from 20+% million two years ago. However, that growth momentum fell sharply to just 3% in 4Q23, driving revenue to $44.7 million. Revenue was primarily driven by the continuous strength in service but was offset by weak equipment sales performance of -6%, a 25-point deceleration vs. 3Q23. Due to the mix, margins improved, which helped drive net income to $10.6 million. Meeting management guided a range of $10 million to $11 million.

Based on author’s own math

Based on my view of the business, NSSC should see growth normalize back to historical mid-single-digit growth. I modeled 5%, which is similar to the pre-covid period growth rate. However, I expect margins to improve from here as the service portion of the business grows into a larger mix. Note that the service portion has a gross margin north of 80%, while the equipment segment has ~17% as of LTM. The normalization of growth should permanently impair the premium in valuation that NSSC enjoyed vs. peers (such as Aaon, Cade Holdings, Hayward Holdings, SPX Technologies, etc.), who are growing from high single digits to low teens and trading at ~20x forward PE over the last few quarters. I expect NSSC to now trade in line with peers, given that growth expectations are now similar to peers.

Comments

I think the poor revenue performance in 4Q23 was definitive evidence of a channel-wide accumulation of Starlink radios inventory. As NSSC experienced increased equipment sales, deviating from the typical $20 million in quarterly sales, it is inevitable that stockpiles will grow in the coming quarters. The increase can be attributed to distributors stocking up on goods in anticipation of the forthcoming 5G wave as 3G Verizon services wind down. The issue arises when the 3G sunset is complete and distributors realize they have too much stock on hand, initiating the destocking process that has a negative impact on NSSC P&L.

Based on author’s own math

Although it may seem counterintuitive, the fact that NSSC experienced negative growth in 4Q23 indicates that destocking is well under way. My main concern is how long it will take for the channel to restock, as the de-stocking seems to be concentrated on the company’s smaller intrusion radios. Management believes it will be another quarter or two before prices for entry-level intrusion radios stabilize. While this might be true, I believe the immediate fact is that NSSC is going to face a tough competition for the next three quarters (1Q24 to 3Q24), as 1Q23 to 3Q23 were still at elevated demand levels.

“And now they have too much because now things have settled down, the 3G sunset is finished. They have to work that inventory down. We’ll help them this happens periodically all the time. The demand for radios as a whole is very good.” Source: 4Q23 earnings

The positive update here is that management has assured us that this situation is not unusual, and there is still a robust demand for radios in general, especially fire alarm radios, which make up about half of their radio business. With the ongoing long-term trend favoring alarm systems, I am also optimistic about NSSC’s upcoming product, the Prima alarm panel. This product offers security and fire alarm protection along with video and automation capabilities and is set to start shipping in the early part of FY24. This introduction should aid in lessening the effects of inventory reduction over the next three quarters.

I think many investors may have missed the positive in NSSC’s recent results due to the major negative headline. Demand for NSSC’s door-locking devices remains strong (up 4% sequentially and 25% y/y), thanks to increased vigilance regarding student safety and renovations at transportation hubs like airports and healthcare facilities. The success NSSC has had recently in the door-locking device market, together with qualitative comments of growing demand (such as the recent installation of 700 of its Trilogy electronic locks at the University of Arizona), provides further evidence of the company’s upward trend. This continued momentum will be crucial in the next 3 quarters, as it may be able to help offset the impact of the challenging radio inventory situation.

“We are pleased to learn that recently in the University of Arizona, recently installed over 700 of our Trilogy electronic locks on their campus.” Source: 4Q23 earnings

Conclusion

I recommend a hold rating for NSSC due to the uncertainty surrounding the duration of the channel destocking process. I expect the company to continue reporting weaker results in the near term as it faces tough year-over-year comparisons from 1Q23 to 3Q23. Despite positive traction in the Doors segment, the market appears to be more focused on recent performance challenges, as reflected in the share price.

{kind=link}