Panuwat Dangsungnoen/iStock via Getty Images

With Congress ratcheting down saber-rattling over broader healthcare reforms into 2024, Morgan Stanley has taken a more constructive view on the managed care and retail pharmacy space, mainly due to the biosimilar/GLP-1 opportunity.

However, the analysts led by Erin Wright highlighted the implications of rising healthcare utilization rates and cited the opportunities/ risks related to the upcoming advanced 2025 Medicare Advantage rate notice.

Despite cost trends as seen with rising utilization rates into 2024, “election cycle risk will also be front and center,” MS analysts wrote, issuing their 2024 outlook for healthcare services.

Election risk

MS pointed to the sector’s underperformance this year, noting that managed care organizations dropped 15% while pharmacies fell 49% YTD. According to the firm, managed care organizations have historically shed a median of ~31% during the past six election cycles until a mid-March trough.

However, after the ballot, managed care has historically outperformed the S&P 500, leading to a median relative outperformance of ~12% and ~20% over the six and 12 months following the election day, respectively.

Compared to previous elections, the firm cites a lack of support among lawmakers for broader healthcare reforms, or Medicare for All. “President Biden declaring a run for reelection largely derisked Medicare for All as an overhang by keeping more progressive Democrats on the sidelines,” MS analysts added.

“While past experience tells us to avoid managed care into US presidential elections, we actually view it will be a relatively benign cycle from a healthcare perspective,” the analysts wrote, noting that owning MCO stocks this year ahead of potential troughs “may not be as punitive, if at all.”

GLP-1/biosimilar opportunity

The firm highlights Pharma Benefit Managers as a key MCO theme in the sector, noting their potential to benefit from the GLP-1 class of weight loss drugs and biosimilars.

Despite regulatory headwinds, Morgan Stanley sees value and growth prospects in the PBM space. The group acting as intermediaries between health plans, pharmaceutical manufacturers, and pharmacies has recently come under intense congressional scrutiny over their role in rising healthcare costs.

MS also projects PBM’s potential to benefit from GLP-1 drugs, a new class of obesity drugs marketed by Eli Lilly (LLY) and Novo Nordisk (NVO) (OTCPK:NONOF).

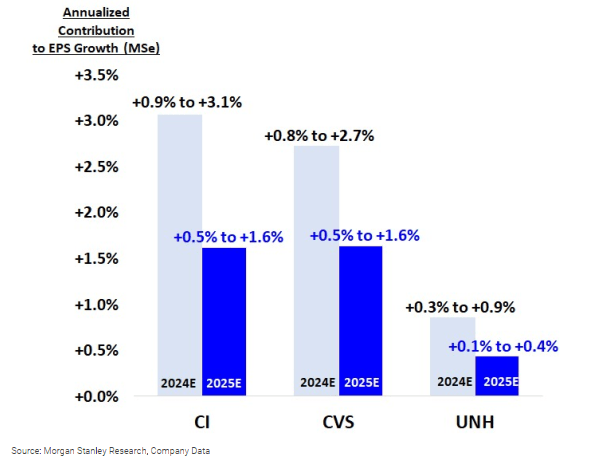

According to the firm, the rising demand for GLP-1s can improve the 2024E and 2025E EPS of three leading PBMs, namely the Caremark unit of CVS (CVS), UnitedHealth’s (NYSE:UNH) OptumRx, and Cigna’s (NYSE:CI) Evernorth, by ~26 bps–~307 bps and ~13 bps–~163 bps, respectively.

There will be additional opportunities from the end of U.S. market exclusivity for AbbVie’s (ABBV) blockbuster arthritis drug Humira, given the $38B market size and upcoming biosimilars, including ones with interchangeable designations.

In January, Amgen (AMGN) introduced its Humira biosimilar, Amjevita, the first of many off-patent versions launched in the U.S. against the bestselling injectable this year.

Rising healthcare utilization

Additionally, Morgan Stanley pointed to rising cost trends in the MCO space after UNH said in June that the company’s medical care ratio, the portion of premiums spent on healthcare costs, will come under pressure amid a post-COVID spike in medical activity.

While higher healthcare utilization, a key investor concern in 2023, “will remain elevated into 2024, it is encouragingly not worsening, a dynamic that we will monitor but is appropriately embedded in expectations for MCOs,” the analysts opined.

MA advanced rate notice

Commenting on the 2025 Medicare Advantage advanced rate notice expected in late January or early February, the analysts argued that MCOs have been bracing for a post-pandemic normalization in the rate environment.

MS estimated that the MA advanced rate notice for the 2025 calendar year could come at +0.2%, in line with the pre-pandemic levels. The analysts also wrote that any weakness in MCO stocks following the announcement will be a compelling buying opportunity.

In recent history, 2022 and 2023 saw the largest hikes to Medicare Advantage final rates before the 2024 final rate came flat.

Medicaid redeterminations

MS thinks that the ongoing Medicaid eligibility reviews, which it expects to continue until at least 2024, will be among the key MCO themes to watch out for next year.

The analysts argue that commercial insurer Cigna (CI) will become a major beneficiary of the ongoing redeterminations, which resumed in April after a pandemic-era pause in the past few years.

“CI does not participate in MDCD managed care programs and MDCD redeterminations represents an upside opportunity for its commercial/employer sponsored plans and the exchange marketplace which is not currently embedded into guidance,” the analysts wrote.

Ratings

The Bloomfield, Connecticut-based company is a key Overweight for MS on its biosimilar opportunity and minority investment in healthcare provider VillageMD, which is majority-owned by Walgreens (NASDAQ:WBA). Its price for CI stands at $365 per share.

However, Walgreens (WBA) has become a key Underweight for MS, and its price target, adjusted to $22 from $27, reflects a softer growth outlook for FY24. The firm cites macro challenges, lower COVID-19 vaccine and test volumes, a weaker respiratory season, and ongoing changes to the company’s retail footprint as reasons for its bearish outlook.

Given its scale and diversification, UnitedHealth (UNH) was crowned Morgan Stanley’s top pick in the MCO space. Citing its growth prospects and diversified business model, the firm raised UNH’s price target to $618 from $579 per share with an Overweight rating.

Other listed MCOs include Centene (CNC), CVS Health (CVS), Elevance Health (ELV), Humana (HUM), Molina Healthcare (MOH), Alignment Healthcare (ALHC), and Clover Health Investments (CLOV).

{kind=link}