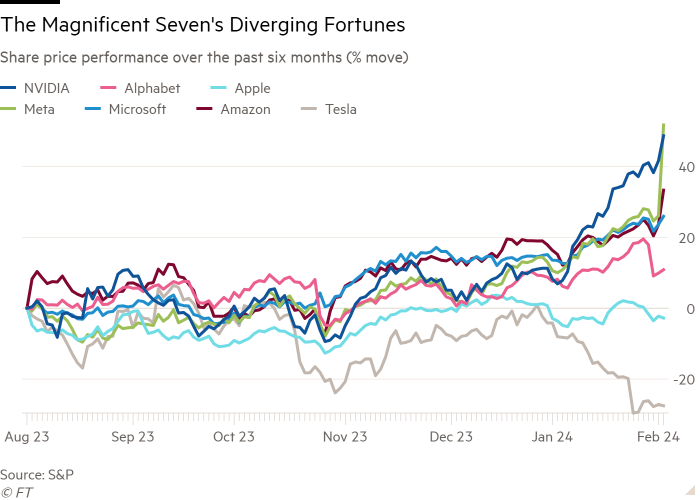

The grip of the so-called “Magnificent Seven” tech companies on US stock markets has loosened as investors focus on concrete results rather than solely on artificial intelligence’s potential.

The seven largest tech groups — Microsoft, Apple, Amazon, Alphabet, Meta, Tesla and Nvidia — drove most of last year’s stock market gains as traders bet that they would be winners from the growth of AI. But gaps between them have widened as all but one reported financial results over the past few weeks.

“It is not trading as a bloc any more,” said Jim Tierney, a growth-focused portfolio manager at AllianceBernstein. “Last year everybody got the AI halo . . . 1707036824 the market is starting to zero in on what are the individual prospects of each of the Magnificent Seven as opposed to treating them as one security.”

While four of the seven have continued to outperform the wider stock market, Alphabet has lagged behind the S&P 500, and Tesla and Apple have been the two largest drags on the index. Tesla has tumbled so far it is now fighting to hold on to its place among the top 10 most valuable companies in the US.

Nvidia, which reports its fourth-quarter results in late February, has experienced the most direct continuation of last year’s AI-focused trend. Its shares have soared another 34 per cent, encouraged by other companies’ AI investment plans.

Meta, Microsoft and Amazon are among those that have doubled down on AI spending, but their stocks have been supported by more prosaic factors like strong sales and, in Meta’s case, the announcement of its first ever dividend. In contrast, Apple investors have been spooked by weaker sales in China and Tesla was hit by a warning about slowing growth.

“People are looking at the specifics,” said Fawaz Chaudhry, head of equities at Fulcrum Asset Management. “I would say for Tesla at least, some of the sheen was unearned in terms of AI . . . [and] Apple has been less clear about how it will monetise the data it has with AI.”

Towards the end of 2023, macroeconomic trends gave an extra tailwind to megacap stocks and smaller companies alike, but recent economic data and central bank updates have added to the pressure on companies to deliver.

Falling inflation spurred hopes that interest rates were close to their peak, powering a broad late-year rally. In recent weeks, however, investors have been toning down their expectations of how quickly interest rates will fall.

Lower rates increase the valuation investors are willing to pay for riskier assets like stocks. The Fed is still expected to start cutting rates later in the year, but with much of the benefit already priced in, most investors do not believe price to earnings ratios can rise much further. That increases the importance of earnings to drive further share price gains.

“Heading into earnings season, investors were already really bullishly positioned on some larger-cap names, so the bar to outperform was higher,” said Vishal Vivek, a strategist on Citi’s equity trading desk. “It’s been the companies that have really given something extra to investors that have traded up”.

The recent shift in tone has seen Warren Buffett’s Berkshire Hathaway and drugmaker Eli Lilly overtake Tesla in terms of market capitalisation.

Eli Lilly’s strong performance in particular — its stock has almost doubled over the past year on the back of strong demand for new weight-loss drugs — highlights the fact that there are at least some themes besides AI that have stirred investor enthusiasm. Novo Nordisk, Eli Lilly’s Danish rival, has also soared.

But investors who were hoping for a more general broadening of market gains have so far been disappointed. Amanda Agati, chief investment officer for PNC Financial Services, said: “Our wish at Christmas was a resurgence in the bottom 493 stocks [in the S&P 500]. We got coal in our stockings so far . . . There’s still a very narrow market leadership on full display.”

The S&P 500 is up 4 per cent year to date. The strongest drivers of the gains have shifted slightly — Apple, Tesla and Alphabet have recently been replaced by Eli, Berkshire and Nvidia rival AMD — but by some measures the market’s advance has been even more heavily concentrated than in 2023.

The equal-weighted version of the S&P 500 has risen just 0.2 per cent compared with the benchmark index’s 4 per cent gain. Last year the top seven contributors drove around 60 per cent of market gains; year to date they have powered more than 80 per cent of the increase.

Agati said there were hopes that fourth-quarter earnings season would help lift confidence in the rest of the market. But with almost half of companies now having reported, results thus far have been mixed.

The S&P 500 is on track to eke out a year on year earnings increase of 1.6 per cent for the fourth quarter of 2023, according to FactSet, but if the original Magnificent Seven were excluded, earnings would be down over 8 per cent.

“You are going to see more differentiation between the megacaps and arguably we already are,” said Michael Grant, head of long/short strategies at Calamos Investments. “But let’s not forget why the dominance of these businesses exists . . . Outside of these names, the broader earnings outlook for the equity world is muted.”

{kind=link}