Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

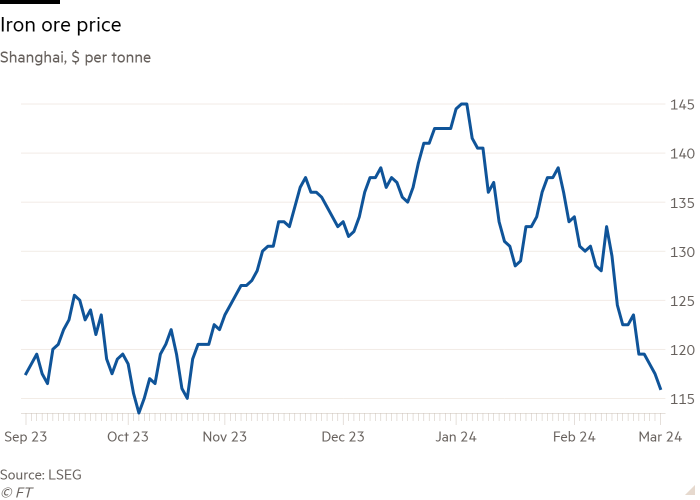

Spring is historically the peak season for steel demand in China. When futures plunge just ahead of that time of year, you know that something is not right.

Three years ago, prices for iron ore, the material used for steelmaking, rose so fast to record highs that Beijing had to intervene with vows to punish speculation. More than two decades of nonstop gains in real estate prices had left the local steel sector’s growth seen as almost guaranteed.

Now iron ore prices are plunging, down over tenth since mid February and by nearly a fifth this year. Oversupply coupled with China’s economic slowdown means the sector is becoming a dangerous one to invest in.

Global investors had hoped for a rebound in Chinese steel demand following the Lunar New Year holidays last month as consumer spending showed signs of improvement. That has not materialised. Demand is falling from all the sectors that have been the largest buyers of steel: property developers, carmakers and home appliance companies.

Futures for iron ore have been sliding last week in Singapore, as have Chinese futures and steel contracts in Shanghai. Inventories at major Chinese steel mills jumped more than a quarter over the past few weeks.

Overcapacity has long been a problem, despite Beijing’s efforts to limit steel production, with about 500 steel mills in the country. Demand from the local property sector — which, as the hungriest sector, accounts for over a third of China’s total steel consumption — remains depressed with no end to the real estate crisis in sight.

Country Garden, one of the largest developers, received a liquidation petition filed by one of its creditors last week, which suggests a further decline in steel demand is on the cards. Liquidation proceedings mean the priority becomes selling off assets and could make it more challenging for developers to access new funding, halting construction and leaving thousands of homes unfinished

Shares of Baoshan Iron & Steel, the listed subsidiary of China’s largest steelmaker Baowu, are down over 40 per cent from their 2021 peak. They trade at 11 times forward earnings, significantly lagging behind the performance of regional peers such as South Korea’s Posco. Operating margins are slim at less than 5 per cent, having fallen more than 40 per cent in the past two years.

Investors should not risk getting caught in the turmoil. Further steel price and margin declines, followed by industry consolidation, appear inevitable.

Lex is the FT’s concise daily investment column. Expert writers in four global financial centres provide informed, timely opinions on capital trends and big businesses. Click to explore

{kind=link}