Investors are pushing back their expectations of interest rate cuts around the world, as the US Federal Reserve’s battle with price pressures complicates other central banks’ loosening plans.

As the US reported the latest in a string of poor inflation figures, markets reined in their forecasts for rate cuts by the European Central Bank and the Bank of England, as well as by the Fed itself.

“The Fed’s inflation problems have a global dimension and other central banks cannot ignore them,” said James Knightley, chief international economist at ING in New York. “In particular, if the Fed can’t cut rates soon it could stoke up dollar strength, which causes stress for the European economy and constrains other central banks’ ability to cut rates.”

He added: “Plus there is a worry that what is happening on inflation in the US could surface in Europe as well.”

Senior officials at the ECB and BoE argue they are not confronting the same inflation problems as the US, implying they have more scope to cut rates earlier.

But shifts in the futures market indicate the global impact of the persistent US inflation problem.

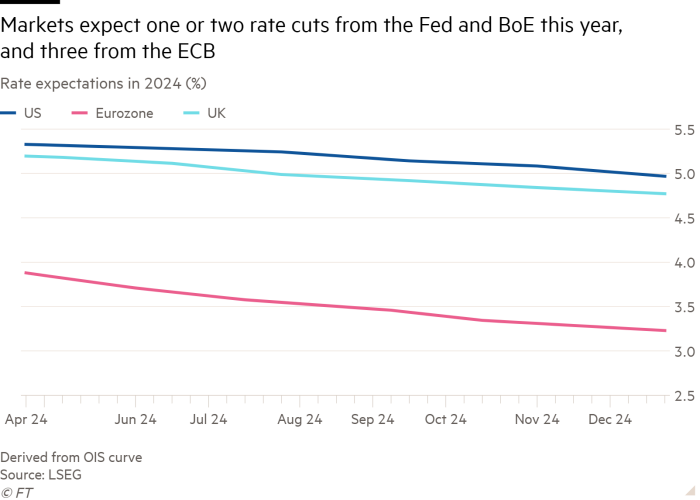

Traders now expect the ECB to cut rates by an average of about 0.7 percentage points this year starting at its next policy meeting on June 6, while two weeks ago they expected cumulative cuts of 0.88 points.

At the beginning of the year, when US inflation appeared on a firmer downward path, they expected cuts of 1.63 points.

Markets now anticipate BoE cuts of 0.44 percentage points this year compared with 0.56 points two weeks ago and 1.72 points at the start of the year.

The backdrop for the shift has been the market’s reduced expectations for the Fed, which is set to keep rates at their 23-year-high at its meeting next week. While at the start of the year investors had expected as many as six quarter-point cuts, this year, they now expect one or two.

The US and its European counterparts have diverged in the past. But if other regions cut rates more aggressively than the Fed, they risk harming their own economies because of the impact on exchange rates, import costs and inflation.

“There’s a good macro case for divergence, but ultimately there’s a limit on how far it can go,” said Nathan Sheets, chief economist at US lender Citi. He added that it was “more challenging” for the ECB to “cut aggressively in an environment where the Fed is waiting”.

Fed chair Jay Powell conceded this month that US inflation was “taking longer than expected” to hit its target, signalling that borrowing costs would need to stay high for longer than previously thought.

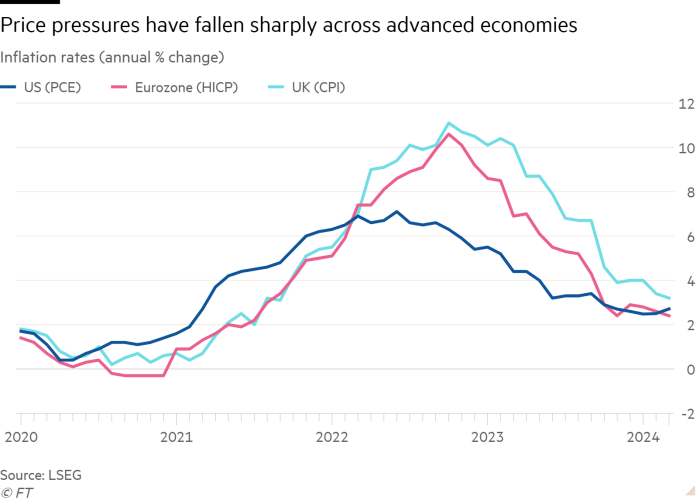

In figures on Friday, the Fed’s preferred inflation metric came in higher than expected at 2.7 per cent for the year to March, and a minority of traders are now even betting on Fed rate rises in the next 12 months.

Marcelo Carvalho, global head of economics at BNP Paribas, said the ECB was neither “Fed-dependent” nor “Fed-insensitive”.

Despite the market’s expectations that high US borrowing costs will limit their freedom of manoeuvre, top European central bankers insist their less serious inflation problem requires a different response.

“It is a different kind of animal we are trying to tame,” ECB president Christine Lagarde said this month in Washington.

She said the “roots and drivers” of the two regions’ price surges were different — with Europe affected more by energy costs and the US by big fiscal deficits.

BoE governor Andrew Bailey has also argued that European inflation dynamics were “somewhat different” from the US.

Top officials from the ECB and BoE have signalled rates will still be cut this summer, despite the inflation data that has led investors to price in the first Fed rate reduction in November.

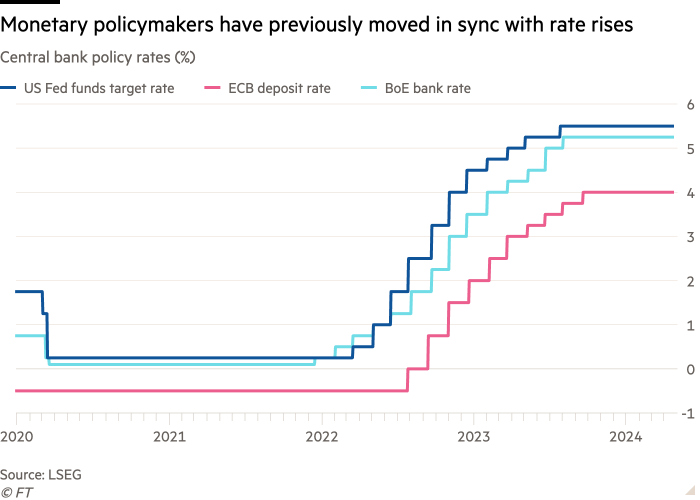

The shift is a marked contrast to earlier this year when the Fed was seen as leading the way down.

“The ECB and BoE are operating in a much weaker growth environment, so I suspect they will have no compunctions about cutting rates earlier,” said Mahmood Pradhan, head of global macroeconomics at Amundi Asset Management.

But ECB policymakers have given divergent indications on how big a rate gap with the Fed they can tolerate.

Banque de France governor François Villeroy de Galhau told Les Echos that he expects continued cutting “at a pragmatic pace” after June. However, Austria’s central bank head Robert Holzmann warned: “I would find it difficult if we move too far away from the Fed.”

The euro has fallen 3 per cent against the dollar since the start of the year to just above $1.07, but investors have increased bets it could drop to parity with the US currency.

Such a fall would add about 0.3 percentage points to eurozone inflation over the next year, according to recent ECB research. The bank’s vice-president, Luis de Guindos, said this week it would “need to take the impact of exchange rate movements into account”.

The far-reaching impact of US policy is already highly visible in Japan, where investors are increasing bets that the Bank of Japan will need to keep raising borrowing costs as a weaker yen fuels inflation. The yen has dropped to 34-year lows against the dollar, pushing up the price of imported goods.

But some EU policymakers argue that if a more hawkish Fed leads to tighter global financial conditions, it could bolster the case for easing in the eurozone and elsewhere.

“A tightening in the US has a negative impact on inflation and output in the eurozone,” Italy’s central bank boss Fabio Panetta said on Thursday, adding that this was “likely to reinforce the case for a rate cut rather than weakening it”.

Tighter US policy also affects global bond markets, with Germany’s 10-year Bunds often mirroring movements by the 10-year US Treasury.

BNP Paribas estimates that if European bond yields were driven half a percentage point higher by the fallout from US markets, it would require an extra 0.2 percentage points of rate cuts by the ECB to offset the impact of tighter financial conditions. Similarly, it would require 0.13 points of extra cuts by the BoE.

Tomasz Wieladek at T Rowe Price in London argued that the ECB and BoE “need to actively lean against this tightening in global financial conditions to bring their domestic financial conditions more in line with the fundamentals in their own economies”.

Additional reporting by George Steer in London

{kind=link}