sankai

Legacy tech made a comeback last week with shares of Intel (INTC), AMD (AMD), and Micron (MU) rallying. Some laggards came back to life late in the week while Nvidia (NVDA) dipped on Friday. Today, I am revisiting GlobalFoundries (NASDAQ:GFS).

I am downgrading the stock from a buy to a hold following lackluster performance and execution so far in 2023.

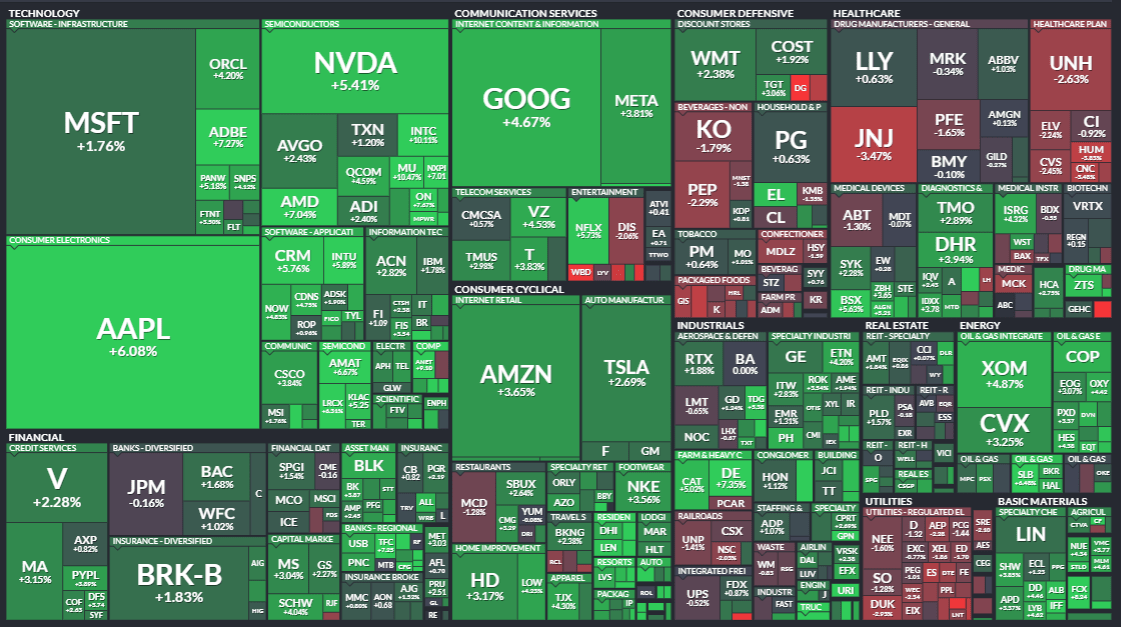

S&P 500 Performance Heat Map Last Week

Finviz

According to Bank of America Global Research, GlobalFoundries is the fourth largest outsourced semiconductor manufacturer (foundry) and is the last remaining US-based pure-play foundry. GlobalFoundries manufactures complex, feature-rich integrated circuits addressing mission-critical applications in smart mobile devices, personal computing, communication infrastructure and data center, home, and industrial Internet of Things (IoT), and automotive markets.

The New York-based $30.6 billion market cap Semiconductors and Semiconductor Equipment industry company within the Information Technology sector trades at a moderate 20.6 trailing 12-month GAAP price-to-earnings ratio and does not pay a dividend. Ahead of earnings in early November, the stock has a not-to-high 31.5% implied volatility and an elevated short interest of 13.5%.

Back in August, GFS reported Q2 sales and earnings that were slightly better than expectations, but the firm lowered its Q3 guidance due to higher-than-anticipated inventories impacting mobile and communication infrastructure markets. The chip company also sees sluggish demand for the balance of 2023 with full-year revenue growth declining to just the high-single digits. Utilization rates have also taken a downward revision with a low to mid-80% range for this year seen, hurting gross margins compared to the previous outlook.

On the plus side, the firm’s Autos and Aero-defense units should offset some of the weakness with a net revenue trough happening back in Q1, so there’s reason for optimism here. The company expects its Autos area to reach $1 billion in sales in 2023, with continued double-digit growth next year. Bullish potential comes from strong manufacturing capacity, geographical advantages, long-term agreements, and steady execution while downside risks include the aforementioned gross margin impact, cyclicality of the semiconductor industry, a high fixed cost structure, and possible operational hiccups regarding how the firm repositions itself.

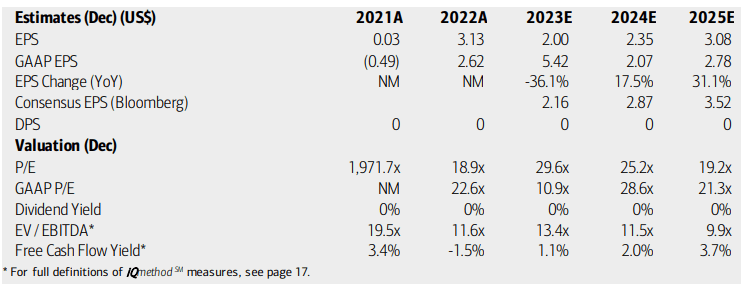

On valuation, analysts at BofA see earnings falling 36% this year on a GAAP basis and then rising about 18% in 2024. Per-share profits in 2025 are then seen as accelerating with operating EPS nearing $3 by that time. The Bloomberg consensus outlook is more sanguine, seeing EPS rising by more than 50% by 2025. No dividends are expected to be paid on this company with modest free cash flow per share. Still, the forward operating P/E of 27 is about on par with the Information Technology sector average while GFS’s EV/EBITDA ratio is actually less than that of the broader market.

GlobalFoundries: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

If we assume normalized EPS of $2.40 over the coming four quarters and apply a 23 multiple, near the average of its primary competitors listed below, then the stock should trade near $55 – that is about the share price today. I am optimistic, though, that GFS will execute well in the coming quarters, and if that plays out, then the valuation could become more attractive in 2024.

GFS: Generally Weak Valuation Conditions Currently

Seeking Alpha

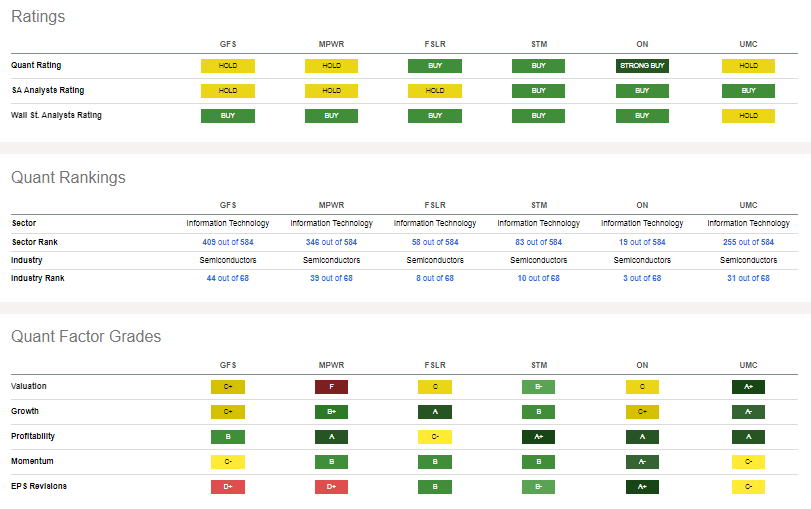

Compared to its peers, GFS features a middle-of-the-road valuation while its growth trajectory leaves something to be desired by the bulls. While profitability is respectable, its stock price momentum has been particularly soft this year amid a rosy outlook in the chips market. Finally, earnings revisions have been poor, hence my downgrade today.

Competitor Comparison

Seeking Alpha

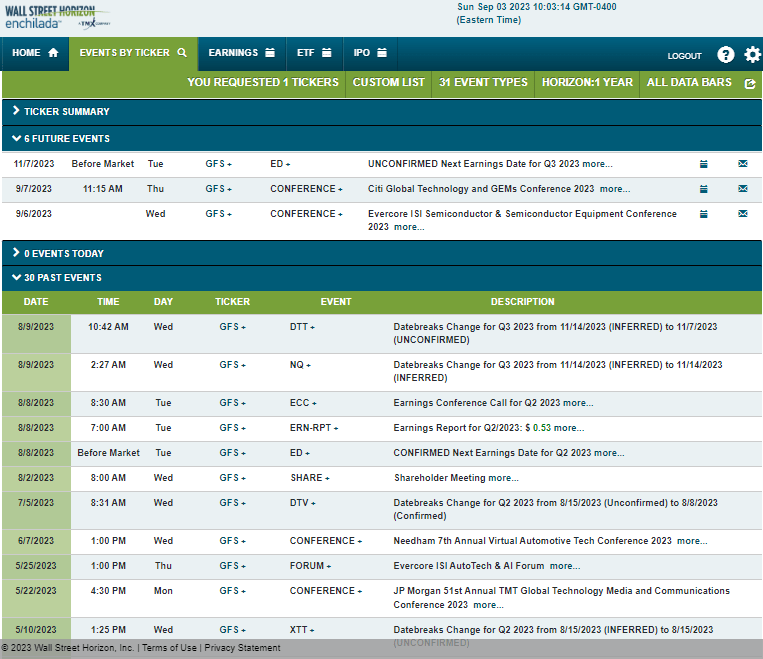

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q3 2023 earnings date of Tuesday, November 7 BMO. Before that, there could be some share price volatility around a pair of industry conferences at which GFS’s management team is expected to present. The first is the Evercore ISI Semiconductor & Semiconductor Equipment Conference from September 6 to 7 and the next is the Citi Global Technology and GEMs Conference 2023 from September 5 to 8.

Corporate Event Risk Calendar

Wall Street Horizon

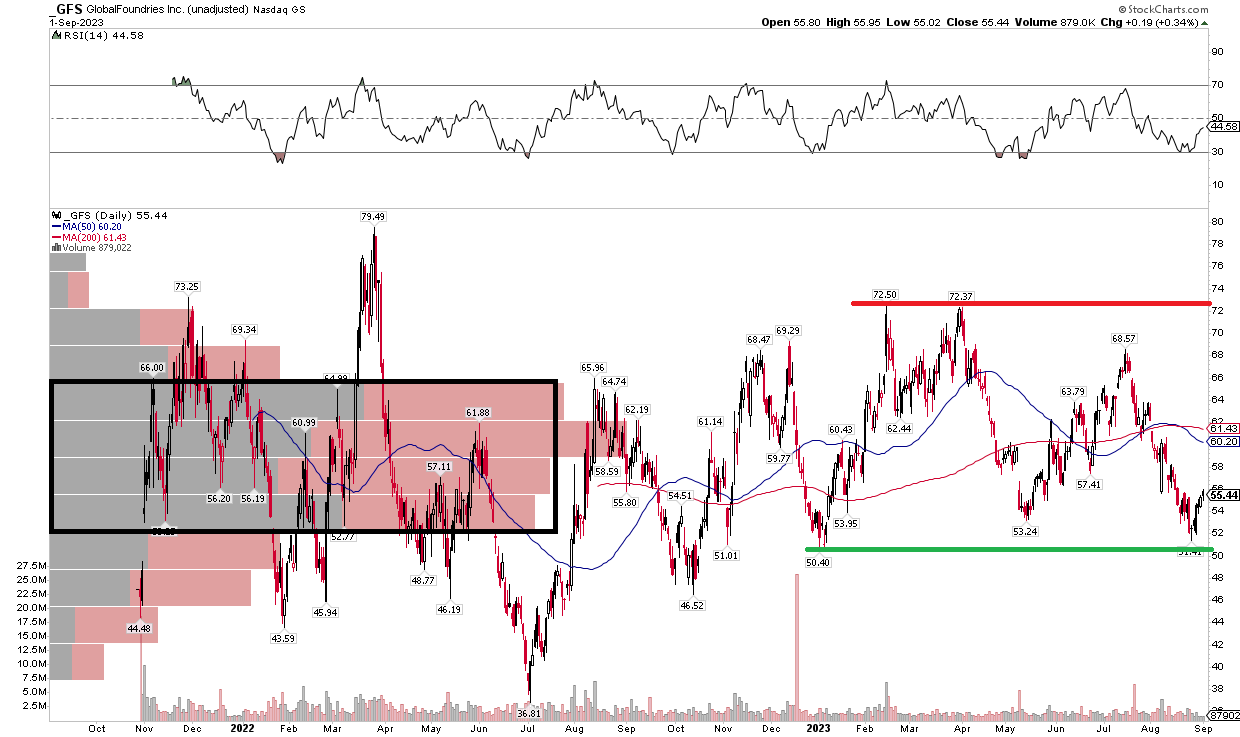

The Technical Take

GFS has done a whole lot of nothing since shares began trading in late 2021. Notice in the chart below that the stock has been one big chopfest. With shares rangebound, perhaps we can identify some support in the $51 to $53 range while resistance could come into play at a double top from the first half of the year just above $73.

Supporting the neutral stance is a high amount of volume by price in the $53 to $65 zone, as indicated by the horizontal bars on the left side of the graph. There is also little to be gleaned from the RSI momentum indicator at the top of the chart – it has been bouncing back and forth from 30 to 70, so range traders could play that trend. With a flat long-term 200-day moving average and a 50dma that is also wobbling, that is just another sign of trendless price action.

Overall, perhaps a long play here as the stock rallies off support could work, with a sell stop under $50, but at a broader level, the chart is kind of a mess.

GFS: A Rangebound Chart, Shares Working Off Support

Stockcharts.com

The Bottom Line

I am downgrading GFS from a buy to a hold. This semiconductor stock has not been a winner in 2023 like so many other chip names. With a less optimistic earnings outlook and a chart that is merely rangebound, all signs point to a continued holding pattern.

{kind=link}