JLco – Julia Amaral/iStock via Getty Images

It remains to be seen whether the blockbuster retail sales report for last month points to “resilience or a last hurrah” in the wake of weakening consumer demand and persistent inflation, S&P Global Market Intelligence analyst Michael Zdinak wrote in a recent note.

Stronger-than-expected retail sales combined with January’s unexpectedly robust nonfarm payrolls report and surprisingly impressive manufacturing industrial production growth helps lower the odds that the economy will dip into a recession in Q1, Zdinak contended, “but let’s not get carried away.”

He cited the move toward earlier holiday sales as the main driver behind December’s 1.1% dip and January’s 3.0% bounce in retail sales, which are not adjusted for inflation. Federal Reserve officials have made plain time and time again that one or two months of data are not enough to make reliable predictions about the broader economy, especially when it comes to setting monetary policy.

But taking the latest report at face value, along with a resilient labor market marked by a historically low jobless rate, elevated wage growth and a high level of job openings, the rate-setting Federal Open Market Committee might be inclined to keep interest rates higher for longer, in a move that would take its peak federal funds rate higher than previously projected.

“February’s data will be closely watched to determine the direction of consumer spending and the economy this year,” the Feb. 15 note said. Retail sales are closely-watched data as consumer spending accounts for some 70% of the country’s output.

Two days before the release of the Feb. 15 retail sales report, S&P Global economists had predicted retail sales will grow by 0.5% in 2023, or a 0.1% slump on a real (inflation-adjusted) basis, only to then return to slower growth than pre-pandemic levels, according to a separate report. Also, price growth for the year is expected to collapse to 0.6% from 8.9% in 2022.

“If the consumer is pulling in their horns, then to a significant degree that is going to contribute to slower economic growth and maybe recessionary growth,” Federated Hermes Chief Equity Strategist Phil Orlando told S&P.

In another sign that consumer demand has ebbed at end-2022, E-commerce behemoth Amazon (AMZN) recently turned in Q4 earnings that trailed Wall Street expectations by a wide margin. And Walgreens Boots Alliance (WBA), the owner of retail pharmacy chains Walgreens and Boots, posted fiscal Q1 results reflecting a decline in sales.

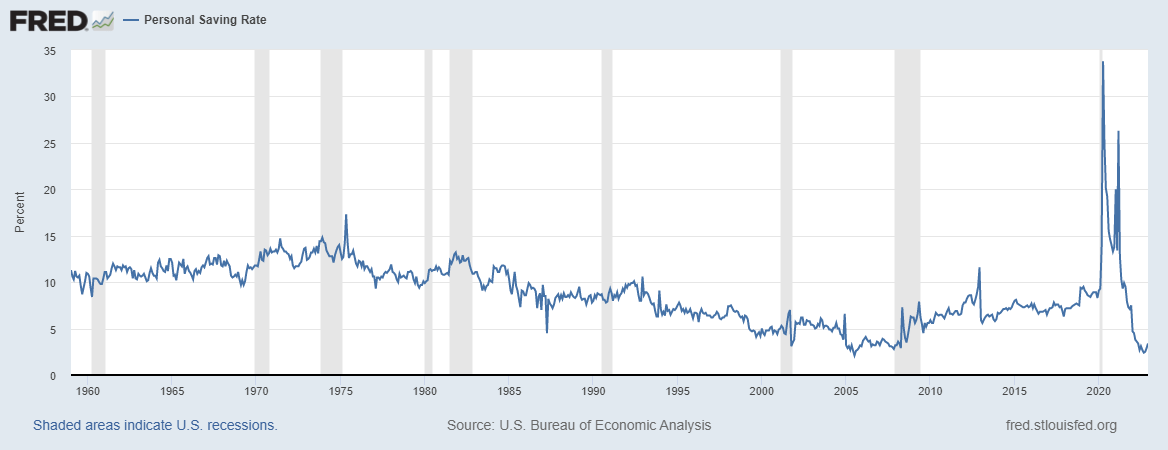

2022 also ended with a historically low personal savings rate, as seen in the chart below, while household debt climbed to its highest in two decades. Whether or not a recession hits the U.S., triggered by the Fed’s ongoing interest-rate increases, that dynamic does not bode well for consumer spending. Furthermore, a recent round of stronger-than-expected economic data has prompted both policymakers and markets to call for a higher terminal rate. That in turn would potentially hurt consumer demand as borrowing costs (for mortgages, auto loans, etc.) would drive even higher.

In Q4 2022, e-commerce retail sales slid 0.1% versus Q3’s 3.0% climb.

SA contributor James Picerno explains how the strong rebound in retail sales gives the Fed more room to lift rates.

{kind=link}