Like hundreds of thousands of homebuyers in the UK every year, Steve didn’t think twice before applying for a short-term fixed-rate mortgage. It was only when his application was rejected on a technicality that the Somerset-based IT professional looked for other options.

A mortgage broker suggested he try a new lender called Perenna. He was first impressed that the lender “applied a bit more common sense” to the technicality about the terms of the lease on his flat that had stymied his last application.

But he also learnt that the mortgage on offer was fundamentally different. Perenna, which received a full banking licence last year, offers a fixed interest rate for the entire life of its mortgages, up to 40 years.

“It won’t go down, but it won’t go up,” says Steve, who chose a 25-year loan and who asked the FT not to use his real name. “Given the markets and everything at the moment, it’s nice to know . . . that it’s not going to change.”

Perenna is one of a handful of lenders now offering borrowers the choice to fix their interest rate for decades, in a bid to disrupt the £1.6tn UK mortgage market.

Rising mortgage rates have been the dominant feature of the property market in the past two years, and a major contributor to the UK’s cost of living crisis.

Loans issued during the era of ultra-low interest rates are now reaching the end of their terms, with 1.6mn households due to see their fixed rates end in 2024, according to UK Finance.

A typical borrower who took out a two-year fix at 1.6 per cent in 2022 will face a 42 per cent increase in their monthly payments, according to calculations by Zoopla, the property portal.

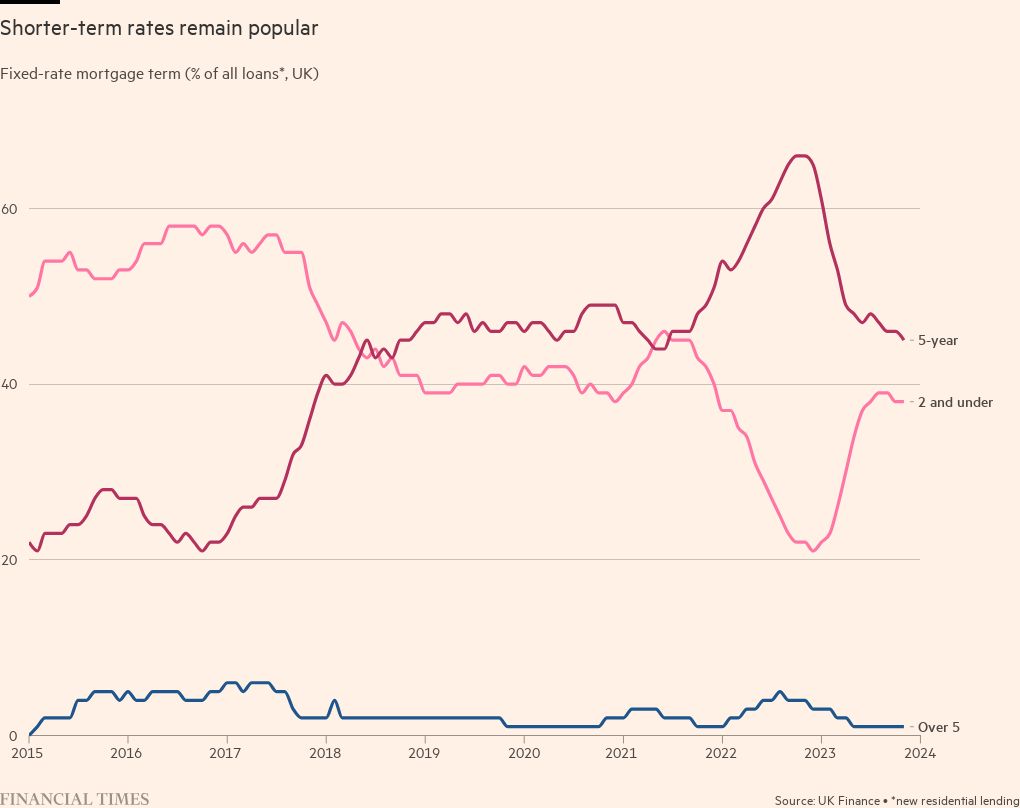

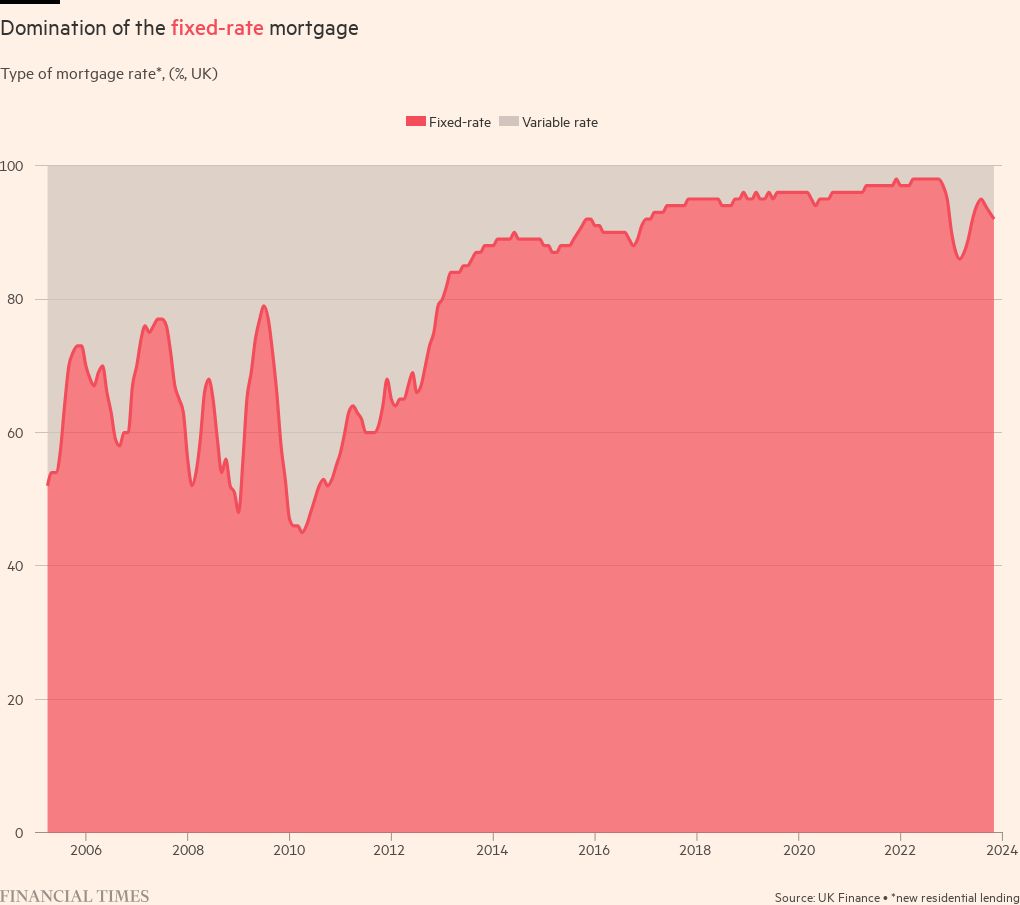

The sudden jump to much higher borrowing costs has highlighted an oddity of the UK mortgage market: the unusually high portion of short-term fixed loans. More than 90 per cent of UK borrowers take out a fixed-rate mortgage for five years or less.

Long-term fixed-rate mortgages are the norm in the US. Locking in for more than 10 years is the most common choice for borrowers in the Netherlands, Denmark and other European countries.

Short-term rates are popular in the UK for their low initial cost and the flexibility they allow for borrowers who foresee themselves flipping their first home to move up the property ladder. But the structure of the mortgage market has been blamed for making it more difficult for first-time buyers to get on the housing ladder at all.

Short-term deals also force individuals to second-guess the interest rate cycle, a challenge that frequently wrongfoots economists and professional traders, leaving them exposed to interest rate shocks.

“Nobody talks about the elephant in the room. Our mortgage market is not fit for purpose,” says Perenna founder and chief executive Arjan Verbeek. “All the European peer countries have better functioning mortgage markets . . . People are protected from a mortgage rate shock.”

Verbeek’s argument has gained traction with politicians. Shadow chancellor Rachel Reeves has hailed the potential benefits of long-term fixes to support a “revolution” in home ownership.

She has said long-term deals could make sense “for a lot of people, especially for families” because “potentially you would be able to borrow a bit more, to put down a bit less of a deposit. If you can take out some of that stress and instability, that will make a difference”.

Labour has pledged to study other countries where these loans are more common, and work with lenders to “encourage increased offering of longer-term fixed-rate mortgages”.

Home ownership rates in England have stagnated for a decade, after falling from their peak before the 2008 financial crisis.

The housing market has become increasingly divided between families who own their homes, and can help their children on to the property ladder and those without equity who are being left behind. The number of owner-occupiers with a mortgage has fallen by 2mn since 2002 and sits at levels last seen in the 1980s, according to Building Society Association research.

Higher house prices and tighter lending criteria mean that the average first-time buyer deposit has risen from £22,600 to £68,700 over 20 years, increasing from 0.6 times average incomes to 1.2 times, according to CBRE.

“There are good reasons for any government at any time to want a nation of homeowners,” says Yolande Barnes, chair of the Bartlett Real Estate Institute at UCL. “From a practical point of view, the last thing you want is a whole load of millennials retiring with no equity.”

But the idea also faces scepticism. Many lenders say there is little demand from consumers and that nurturing that demand will be a major challenge, given that these product are unfamiliar and more expensive upfront. Regulatory reform would be more effective in helping buyers, they argue.

“It always, invariably, looks much cheaper to get the two- and five-year fixed rate,” says Simon Gammon, a broker at Knight Frank Finance. “The peace of mind of a longer term mortgage doesn’t look worth it compared to the rate.”

Ian Mulheirn, a researcher at the Resolution Foundation, says the “obsession” with building more homes has obscured the vital importance of access to credit for aspirant buyers.

“The question is: who bears the risk?” says Mulheirn. “We have been in this market where we just say households bear the risk of interest rates going up, of losing their jobs, of house prices going down.

“The big picture story is: is it sensible to leave these risks on households’ shoulders and try to regulate to protect them, or is there a better way of doing this whole thing?”

The domestic mortgage is one of the most commonplace forms of debt in the world, but the financial architecture behind these loans differs significantly from country to country.

In the UK, home loans are funded in part from deposits and lenders carry the risk of default. Insurance to protect against defaults, widespread in the 1990s, is now rarely used.

“If [longer-term fixed rates] do take off and proliferate, the banks and building societies will have to look at their funding model in the future and what that means for them because they don’t have those long-term savings that they can rely on for 15, 20, 25 years,” says Charles Roe, mortgage director at trade body UK Finance.

Mortgage pricing is based on the cost of “swaps”, derivative contracts that banks use to manage their interest rate risk. In theory, borrowers benefit from a cheaper fixed rate for two or five years, and then roll on to a higher “standard variable rate”, currently around 8.5 per cent on average. In reality, most borrowers refinance at the end of the fixed rate and never pay the higher variable rate.

Regulations designed to protect the financial system after the 2008 financial crisis require banks to “stress test” mortgage applicants, generally to at least 1 per cent above the current standard variable rate.

That means someone buying an averagely priced house on a five-year fix at 4.84 per cent and currently paying around £1,300 per month might be stress tested to make sure they can afford a 9.5 per cent interest rate and monthly payments of close to £2,000.

Stress tests create a trap for affluent renters. Some households will pay more in rent than they would pay for their mortgage, but can’t qualify for a loan because they fail the stress test. Older applicants are also barred if the mortgage term stretches into retirement.

The idea of reforming the UK market with longer-term rates was included in Boris Johnson’s 2019 election manifesto, and analysed in a government-commissioned study as long ago as 2004.

But the launch of Perenna gives these policy ideas a practical and entrepreneurial champion. For the start-up bank, the stress test is basically irrelevant because the monthly payments never change.

The company says it will lend up to six times the borrower’s income, far higher than the standard 4.5 times from high street banks. And it can lend to retirees provided the repayments are affordable on their fixed income.

The interest rates on its loans are between 0.12 and 0.89 percentage points more than the short, fixed deals, depending on the tenure and deposit. But for a couple with a joint income of £60,000, Perenna says it could offer a maximum mortgage of £307,489, giving the buyer an extra £72,000 compared with a loan on standard terms.

Perenna borrowed ideas from Denmark, Germany and Verbeek’s native Netherlands to design its new product. The former credit rating analyst and his team have worked since 2018, funded by venture capital firm Silverstripe, to set up the company and obtain a banking licence.

Perenna does not take deposits, but instead plans to fund mortgages by packaging them into bonds that can be sold to investors. It plans to sell the first bonds this year once it has enough mortgages on its books.

Borrowers face the same early repayment charges as a normal five-year fix, Perenna says. After five years there is no penalty for repaying the loan early or refinancing at a better rate. Mortgages are also portable, subject to conditions, if the borrower moves.

Verbeek says there is significant demand for mortgage-backed bonds from pension providers, who need to match their obligations to retirees against reliable long-term income streams.

“There is nothing more natural than the young family paying £500 to pay off their mortgage and that money going to the pensioner next door,” he says. “We take domestic savings and put them into the domestic economy.”

But pension managers typically want long-term and guaranteed income to fund payouts to retirees, so Perenna will have to carefully manage the terms of its bond issuance to balance meeting investors’ demands and offering flexibility to borrowers.

Advocates believe that if lenders can find a way to navigate these challenges it would unlock home ownership for a new cohort of first-time buyers. A 2019 Centre for Policy Studies paper estimated an additional 1.9mn renters could access a long-term mortgage.

Other reforms could also play a role. A study by the Tony Blair Institute found that borrowers with a smaller deposit and therefore a higher loan-to-value (LTV) ratio are charged a greater interest rate premium in the UK.

In other countries, mortgage insurance mitigates the risk premium for high LTV loans. Even after paying for insurance against default, buyers can still save money. In Canada and Australia, such cover is typically mandatory for low-deposit loans.

In a report published yesterday, the Building Society Association urged other policy changes to redress the balance between ensuring financial stability and allowing access to credit. It said long-term fixes “offer a number of attractions” but had yet to entice many borrowers.

Other experts, such as Barnes at UCL, believe the problem comes down to fundamental economic conditions. She argues that in the 20th century, mortgages were successful in “transferring an enormous amount of equity from landlords to their former tenants”. Consistently higher inflation quickly eroded the real-terms value of those loans, making them more affordable.

“We’re in a different era that does not favour debt in relation to real estate purchases,” she says. Policymakers should focus on other solutions, such as ways for tenants to gradually buy equity off their landlords, she adds.

“The danger of trying to copy 20th century models from other countries is that you’re missing what the actual problem is.”

The more immediate challenge is convincing consumers to try longer-term loans.

Few lenders currently provide multi-decade fixes. Specialist lender Kensington offers fixed rates for up to 40 years while April Mortgages, a wing of Dutch asset manager DMFCO, has products up to 15 years in the UK market.

If longer fixed-rates caught on they could significantly disrupt the UK mortgage sector. Critics of the current structure argue that banks count on a certain percentage of borrowers falling off the carousel of fixed rates and paying the expensive standard variable rate for a period of time. UK Finance says around 7 per cent of borrowers are on SVRs at any one time, although sometimes this is because they are expecting to sell their home in the near future.

Mortgage brokers, who provide fee-based advice to borrowers, also rely on the steady churn of short fixes coming to an end. “There’s a whole economy based on reviewing your rate every two and five years,” says Knight Frank’s Gammon.

But short-term deals also offer a cheaper interest rate up front. And many UK borrowers want the flexibility move up the housing ladder.

“In the UK, we do have an aversion to fixing for that length of time,” says Roe. “Most people’s marriages don’t last 25 years so, you know, fixing your mortgage for 25 is pretty hopeful.”

Banks already offering seven and 10-year fixes have seen very low take-up from customers, say industry representatives. Liam O’Hara, head of mortgages at First Direct, says that the UK has developed a “highly dynamic” market where lenders compete hard to offer the cheapest short-term rates.

Expectations that the Bank of England will soon cut rates is further damping demand for longer term products, he adds.

Ryan Etchells, chief commercial officer at Together, a specialist mortgage provider that is one of the UK’s largest non-bank lenders, says short-term fixes fitted a pattern of home ownership in the UK where buyers flip properties more quickly.

“The traditional UK trend in home buying is that customers move up the ladder over the course of their lives. The European trend is that people live in their homes for longer. We’re starting to see the European trend come into the UK market,” he says.

But after a recent market study, Together decided not to launch a long-term fixed product. “If we brought that product to market, we don’t think it would be meeting enough customers’ needs to make it attractive, frankly,” says Etchells. “The market demand just isn’t there yet.”

This item has been amended since publication to correct the name of the venture capital firm that has backed Perenna and clarify that Liam O’Hara is head of mortgages at First Direct

{kind=link}