kurmyshov/iStock Editorial via Getty Images

Investment Thesis

An investment in BMW is too risky, given the changing Chinese market. One in three of the company’s cars is sold in China, but now 25% of car sales in China are already EVs, and BMW’s market share here is much smaller. In addition, European sales are also falling, and the company itself says it has still benefited from order backlog. This will not last forever. At the same time, since a lot of money has to be invested in the electric transition, the current low valuation might not be as low as it seems.

Company overview

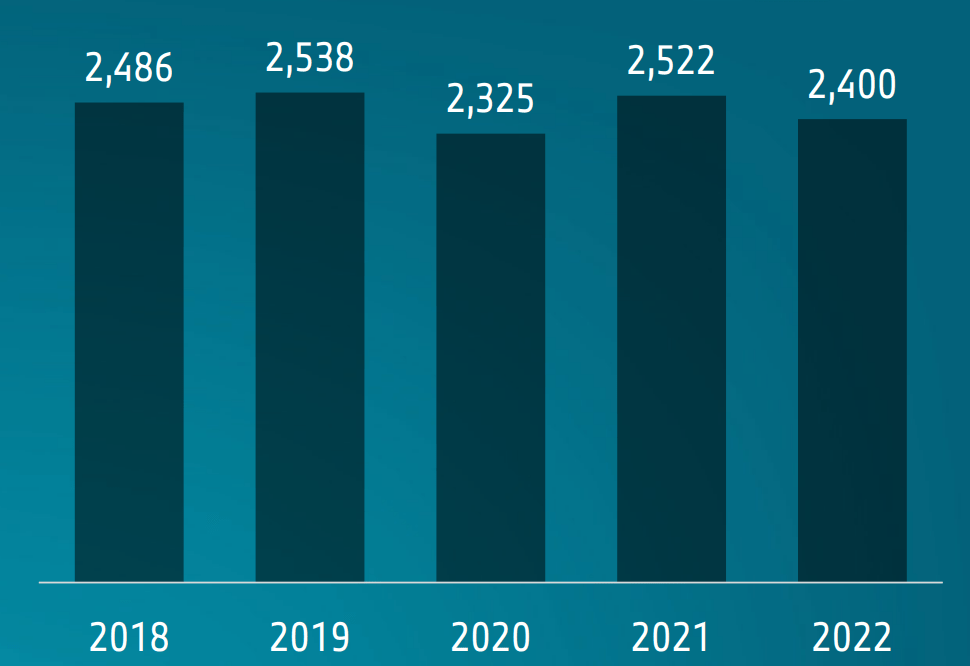

The BMW Group (OTCPK:BMWYY) unites several brands, such as BMW, MINI, Rolls-Royce, and BMW Motorcycles under its umbrella. It’s one of the global heavyweights in the premium automotive and motorcycle industry, being the seventh-largest German company and the sixth-largest automaker by revenue. Last year, BMW sold 2.4 million vehicles, but this number has stagnated for several years.

BMW 2022 report

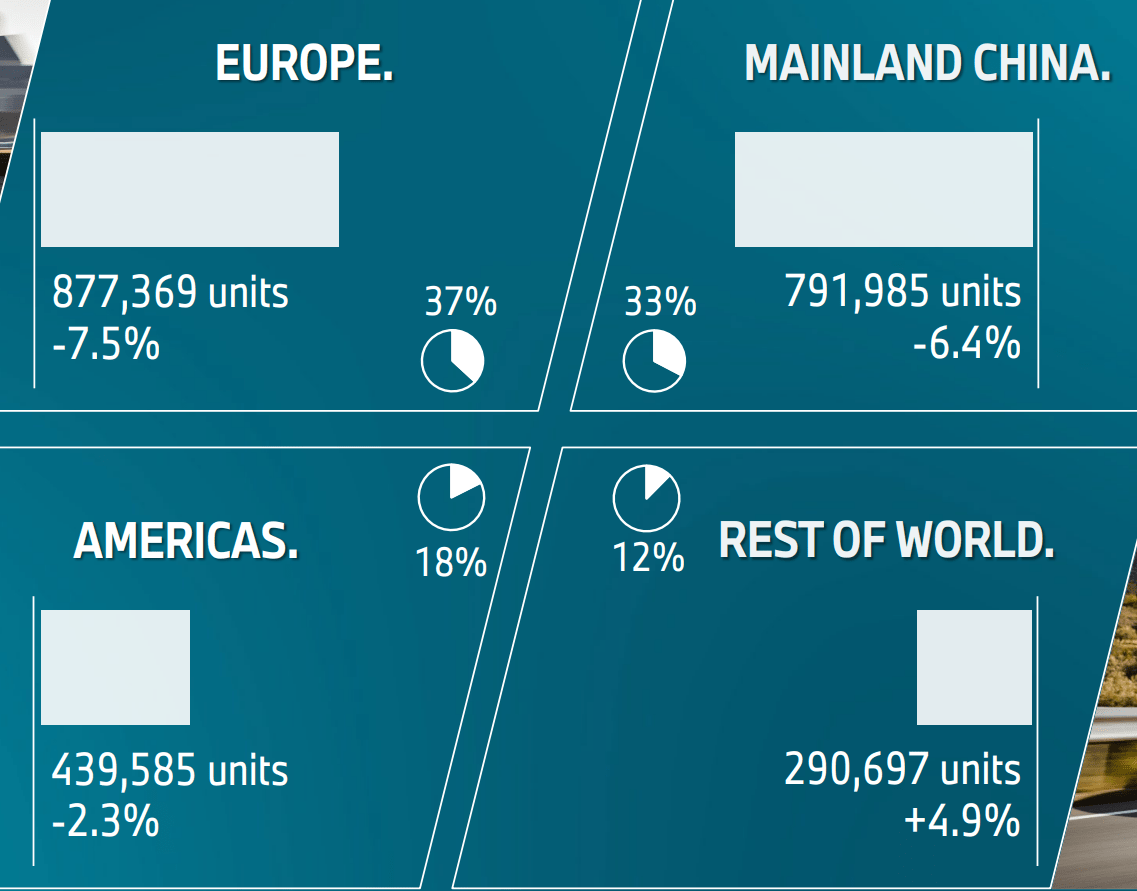

Europe remains the biggest market for BMW, accounting for 37 percent of the total sales. China is second with a 33 percent share. The United States contributed to 18 percent of the total sales last year.

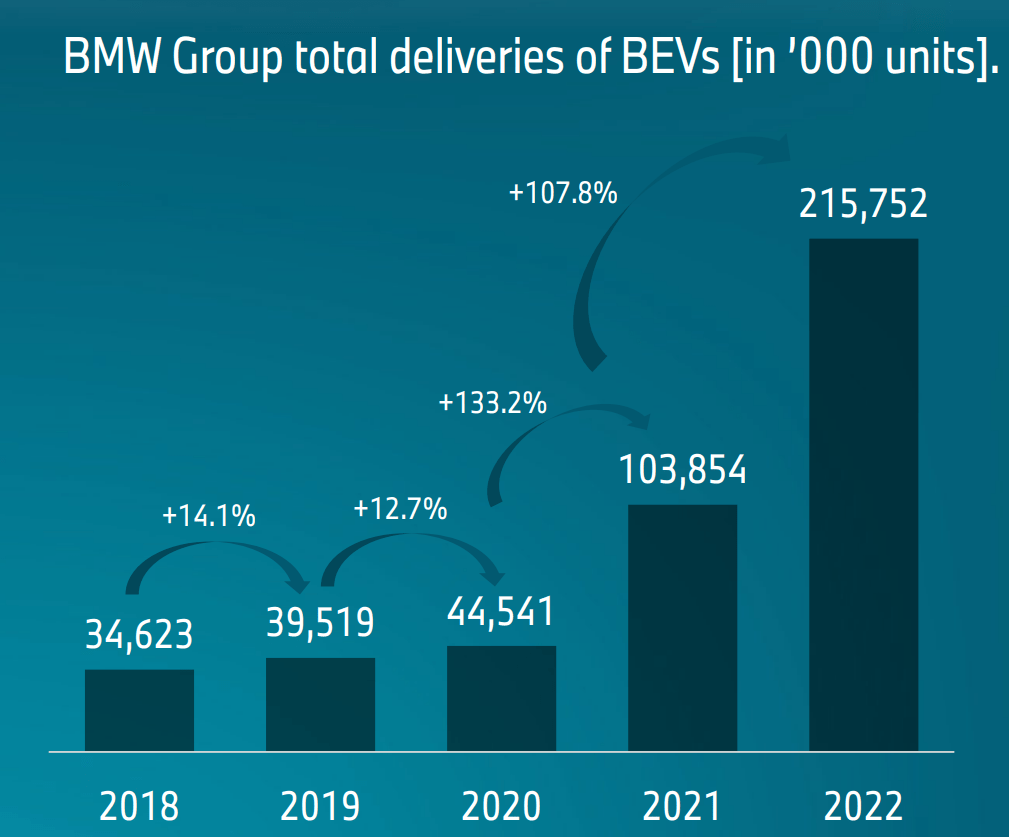

BMW’s business has three segments: Automobiles, Motorcycles, and Financial Services, and the automotive segment accounts for 87 percent of total sales. The EV segment accounted for about 9% of sales, and the company says the target for 2023 is for EVs to reach 15%.

BMW 2022 report

Fewer overall sales in 2022

This strong increase in electric vehicles should not obscure the fact that the total number of vehicles sold is falling. This applies in particular to the two most important markets of Europe and China. The Americas fell slightly, and the rest of the world increased by 4.9%.

BMW report 2022

This is a worrying development, especially because total sales in Europe have decreased, but not by 7.5%. In China, they even increased from 21M to 23M. Overall, global car sales are marginally lower in 2022 compared to 2021, while BMW sales are down 4.8%. From this, one can only conclude that BMW’s market share must have dropped.

The China problem

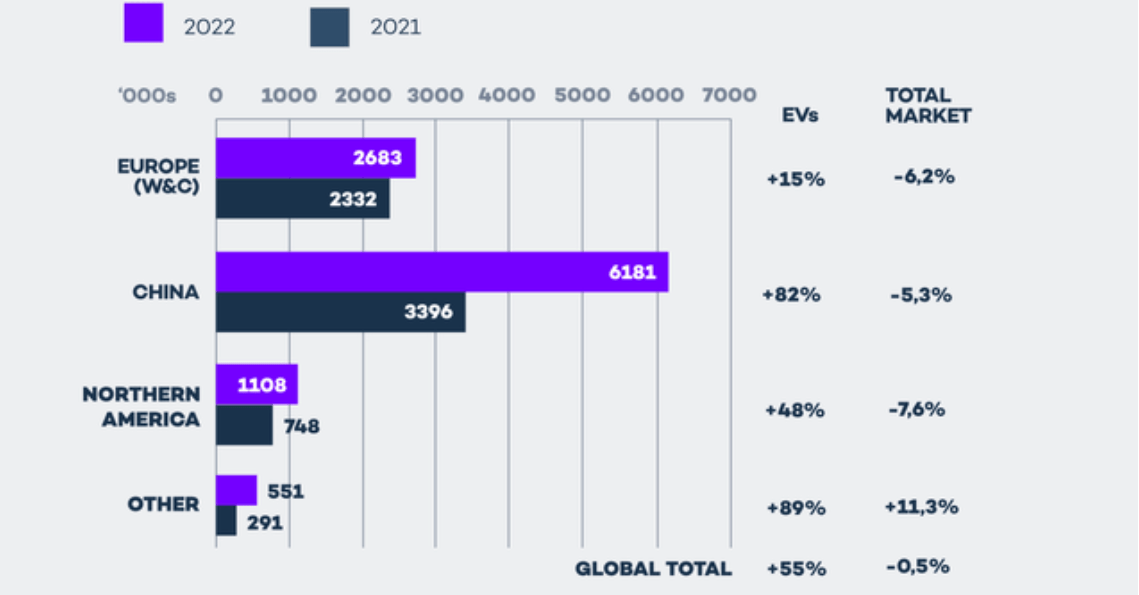

I recently wrote a detailed article about the changing market in China titled “Power Shift: China’s EV Market, Impact On Western Brands, And Some Trading Ideas”. I think it´s a must-read for investors in the automobile sector. In summary, foreign automakers have dominated China in the past, but Chinese brands are preferred for EVs. As a result, foreign automakers operating in China will most likely lose significant market share in the coming years.

The situation is like this: China is by far the biggest car sales market, about as big as the US and Europe combined. EVs have a 25% market share of new Chinese sales, and, except for Tesla, Western manufacturers play almost no role here. This development is not yet reflected so much in the figures due to the remaining 75%, in which many sales can still be generated. But the more EVs are sold, the more market share Western companies will lose. At the same time, China itself is trying to become one of the leading exporters of cars and is penetrating more and more into Europe and all other countries of the world. So Western manufacturers could lose not only the Chinese market but also a part of all other countries.

Power Shift article

My interpretation of BMW’s figures is that you can already see the impact. As I said earlier, total sales in 2022 in China increased by 2M vehicles, but BMW sold 6% less. I believe this trend will continue. Currently, Western companies can’t compete on price with domestic Chinese manufacturers as they offer more and more vehicles under $20k.

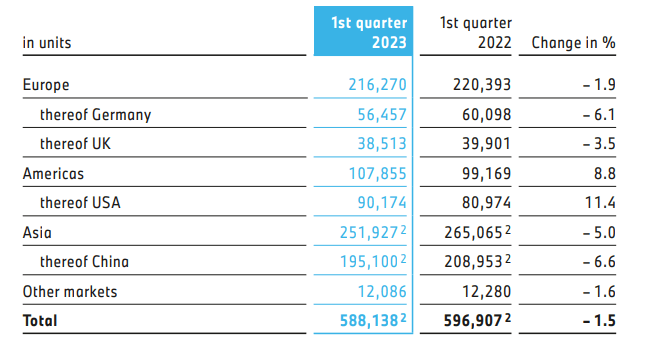

Looking at Q1 2023 YoY, we see the same development. By far the most important country in terms of sales is China, and at the same time, the fastest falling.

BMW Q1 2023

The Chinese market still accounts for a third of BMW’s total sales; that means there is still a lot of room to fall further. I also don’t like the company’s communication style because their investor presentation refers to the aftermath of the pandemic and presents this as why sales are falling. However, this is not the case because, as I said, total sales in 2022 have increased sharply.

What is BMW’s market share in the EV market in China? According to this Chinese website, the company has sold 42k EV cars, but over 6M EVs in total were sold in China. That’s a market share of 0.68%.

virta.global

For comparison, according to my calculation of BMW’s total sales in relation to China’s total car sales, minus electric vehicles, I arrive at a BMW market share of 4.17% for ICE vehicles.

That means the company has 83% less market share in EVs. Assuming that sooner or later, only EVs will be sold in China (which will probably happen at some point) and BMW’s market share would remain at 0.68%, then the company would sell 650 K fewer vehicles per year (25% of the total sales).

Of course, this does not have to happen. There are assumptions in my calculation. But what is not an assumption is that sales are already falling, the percentage of sales of EVs in China is increasing, and BMW s market share here is significantly less. So my calculation is a projection into the future if things stay as they are now.

Outlook and Valuation

But to give credit where credit is due, I must say that it is impressive that the company has managed to increase its overall revenue despite fewer deliveries. The company is focusing increasingly on premium segments with greater pricing power and margins. Although sales are still increasing, net income is decreasing, and the company itself says that earnings per share in 2023 will be significantly worse than in 2022.

German companies often pay dividends only once a year, and most companies pay in May. The ex-dividend date is already over, and on paper, the yield on the current share price looks excellent and corresponds to a yield of 8%. However, investors need to be careful because the money paid out relates to last year’s profits, and if 2023 results are significantly worse, next year’s yield will most likely be lower. EPS are currently downward trending.

The company also points out that Q1 2023 even benefited from European backlog orders. And points out that the consumer, especially in Europe, is still under strong pressure from high inflation. The competitive situation in China is expected to become “even more intense” in the course of the year (page 18).

Conclusion

Everything I have mentioned in this article is already too risky for my taste. But I have not even mentioned all the risks. Furthermore, there is the fact that China is exporting more and more internationally, and therefore, the problem of Chinese competition is not only in their domestic market but soon everywhere in the world.

Otherwise, I would consider chasing the seemingly high dividend yield a big mistake. This has just been paid out and will look different again next year.

Overall, I am very cautious in the automobile market. The entire industry is changing, and I believe European companies could emerge as big losers. Not only does the European consumer have less and less purchasing power, but Europe also has unattractive location conditions due to high energy prices, and for virtually all European manufacturers, China is the most important market. BMW is far from being existence-threatened; probably, they will find their niche in the future car market, but how exactly that will play out and what the sales figures will be is too much speculation for me to consider an investment.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}