hapabapa

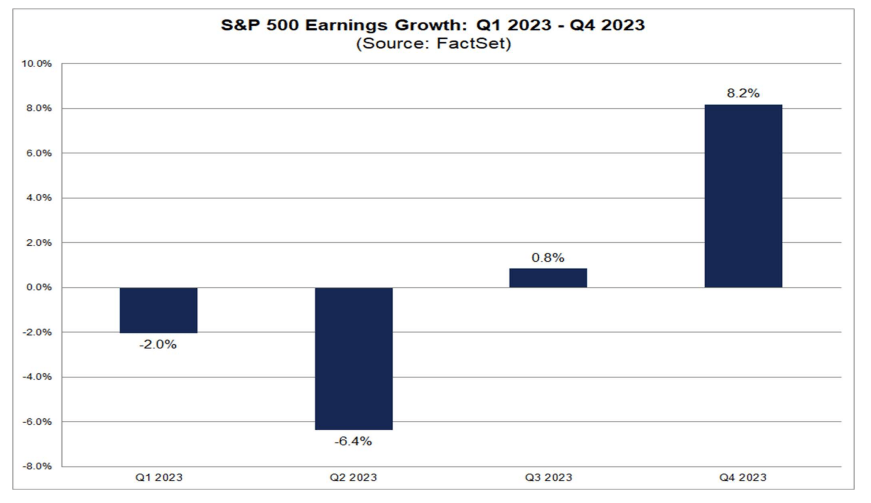

While the Q1 earnings season is technically over, a few key reports trickle in this week. Along with Oracle (ORCL) Monday night, Adobe (NASDAQ:ADBE) reports Thursday AMC. An early look at second-quarter earnings expectations reveals a potential trough in SPX per-share profits. According to John Butters at FactSet, the estimated EPS decline for the S&P 500 is -6.4%. If -6.4% is the actual decline for the quarter, it will mark the largest earnings decline reported by the index since Q2 2020 (-31.6%).

I am initiating coverage on Adobe with a hold due to its fair valuation and technicals that are stretched ahead of earnings later this week.

S&P 500: Trough Earnings Today?

FactSet

According to Bank of America Global Research, ADBE is a diversified software company that offers electronic document technology and graphic content authoring applications to creative professionals, designers, knowledge workers, high-end consumers, developers, and enterprises. Flagship products from Adobe include Creative Suite, Photoshop, Acrobat, Premiere, Dreamweaver, Illustrator, InDesign, and LiveCycle. PDF and Flash technologies from the company have become industry standards and act as a platform for other Adobe products.

The California-based $208 billion market cap Application Software industry company within the Information Technology sector trades at a high 44.7 trailing 12-month GAAP price-to-earnings ratio and does not pay a dividend, according to The Wall Street Journal. The legacy tech large cap has just a 1.3% short interest ahead of earnings on Thursday night.

Back in March, Adobe reported an EPS beat while top-line results also bettered the Wall Street consensus. Revenue was up 9.4% year-on-year and its management team issued Q2 operating EPS guidance in the $3.75 to $3.80 range. It was a solid quarter all around with impressive operating leverage helping to fuel profitability. In-line guidance for the current quarter helps support a long-term positive outlook as it gains share due to a growing Creative Cloud subscriber base and a healthy distribution channel of users.

More recently, the stock rallied after an upgrade from analysts at Wells Fargo – AI was cited as a future earnings driver for the tech name. Last week, ADBE introduced its own generative AI tool, Sansei GenAI for its Adobe Experience Cloud applications. With a bright future, there are risks including heightened competition and its highly cyclical industry.

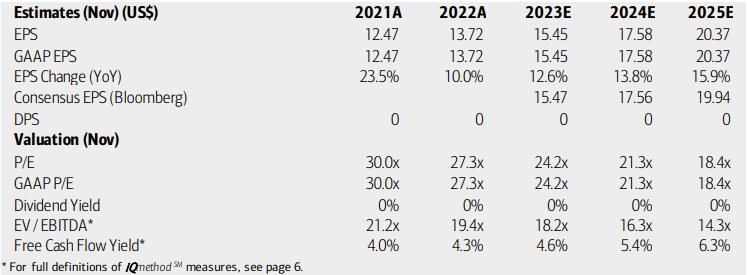

On valuation, analysts at BofA see earnings climbing at a steady and high pace through 2023. The Bloomberg consensus outlook is about on par with what BofA projects, too. While Adobe is free cash flow positive with a 25x FCF multiple, no dividends are expected to be paid on shares.

Following a massive run-up from a month ago, the valuation picture is less attractive compared to after it reported Q1 results back in March. Then, the P/E multiples were in the low to mid-20s, as shown below. Now, however, tack on about 30% to those figures. What’s more, the EV/EBITDA multiple is stretched at 22x next-12-month adjusted earnings.

Adobe: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

As it stands, the forward PEG ratio of ADBE is reasonable at 2.0 – that is below the 5-year average but at a slight premium to the sector median. On a forward price-to-sales basis, Adobe trades at a 10.7 multiple – also slightly under its long-term average. To me, those numbers are fair given higher interest rates today. Overall, considering strong growth prospects and currently high profitability, the lofty valuation is warranted, but I see the stock simply near fair value.

ADBE: Priced Right Ahead Of Earnings Thursday

Seeking Alpha

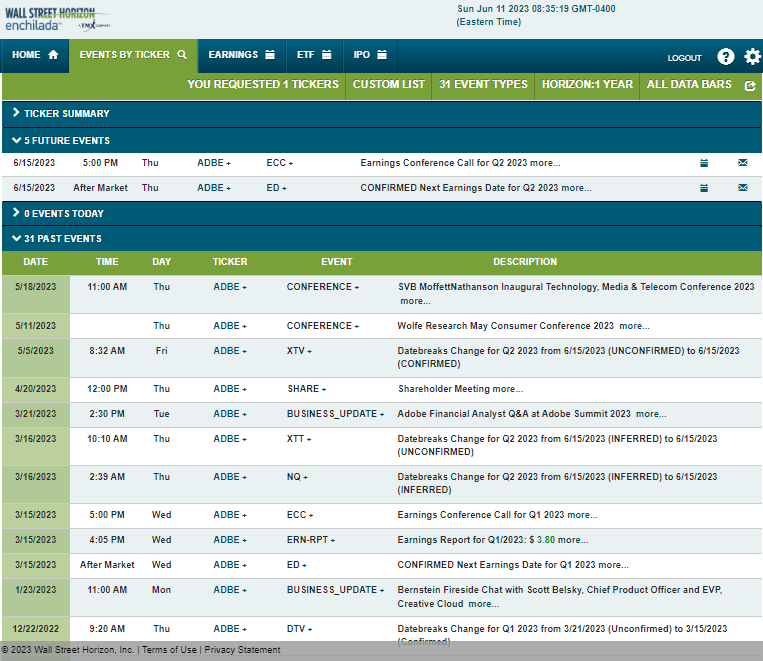

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q2 2023 earnings date of Thursday, June 15 AMC with a conference call immediately after the numbers cross the wires. You can listen live here. No other volatility catalysts are expected in the coming weeks.

Corporate Event Risk Calendar

Wall Street Horizon

The Options Angle

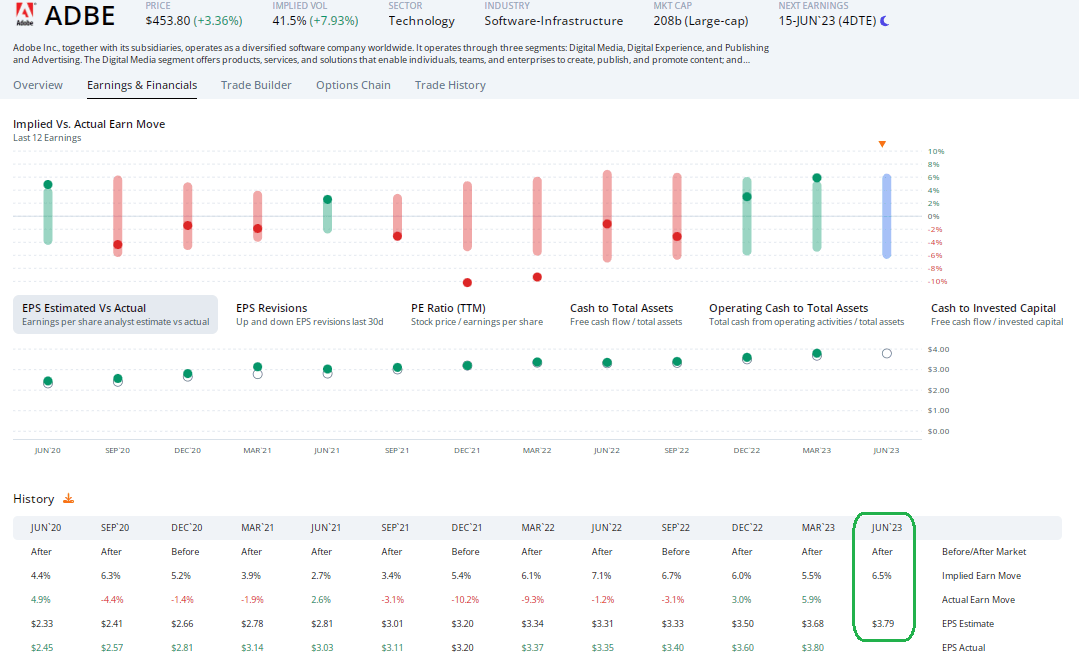

Digging into the upcoming earnings report, data from Option Research & Technology Services (ORATS) show a consensus EPS figure of $3.79. That would be a 13% jump in operating earnings on a year-on-year basis and would be a sequential increase from Q1 per-share profits. I expect a bottom-line beat since Adobe has topped expectations in each of the last 12 reports. The share price reaction history is more uncertain, though. The stock has traded higher post-earnings in the last 2 reports, but the previous 5 instances saw share price declines – with a pair being near –10%.

This time around, the options market has priced in a 6.5% earnings-related stock price swing when analyzing the at-the-money straddle expiring soonest after Thursday’s release. That’s actually the highest premium baked in among the 3 reports this year so far. With somewhat calm reactions over the last year, averaging 3.3%, I am inclined to sell that premium. Let’s attempt to identify where to short options via the chart.

ADBE: Earnings Growth Y/Y, Options Expensive, Expecting A Beat

ORATS

The Technical Take

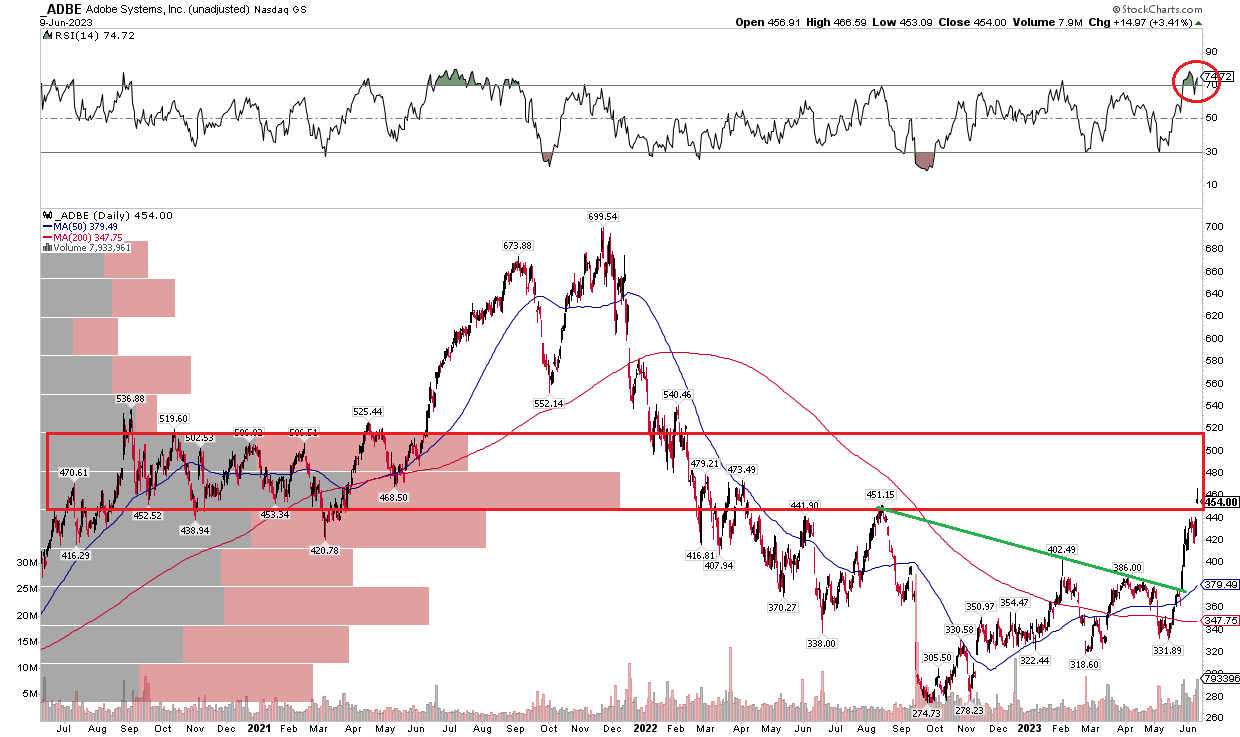

Like many tech names, Adobe has caught a bid from AI mania. Notice in the chart below that the stock has rallied from near $330 in mid-May to almost $470 at the high last Friday. But I see risks ahead. What’s telling is that the stock has rallied into the 2020-early 2021 range between $450 and $520. That is a significant congestion zone, so this first attempt into it could be a challenge. With high volume by price around where ADBE currently trades, the longs should consider harvesting profits.

Moreover, the stock is near-term overbought with the RSI reading at the top of the chart penetrating 80. While I like that shares featured a bullish breakout above a downtrend resistance line around the turn of the month, a retreat is quite possible today. Thus, selling $470 strike calls into earnings could be a near-term play. Long-term investors, however, should look to buy the dip on a correction into the low $400s.

ADBE: Shares Rally Into Resistance

Stockcharts.com

The Bottom Line

I like the growth outlook and long-term prospects with Adobe, but the valuation is merely fair to me at current levels while the technical picture illustrates a neutral to slightly bearish picture after a strong month of momentum.

{kind=link}