AscentXmedia

As I explained in my weekend blog, I’m in New York City this week and I was excited to get back to the New York Stock Exchange. It’s been a while since I was on the trading floor and I bumped into my friend, Peter Tuchman, aka, the Einstein on Wall Street.

Twitter: @rbradthomas

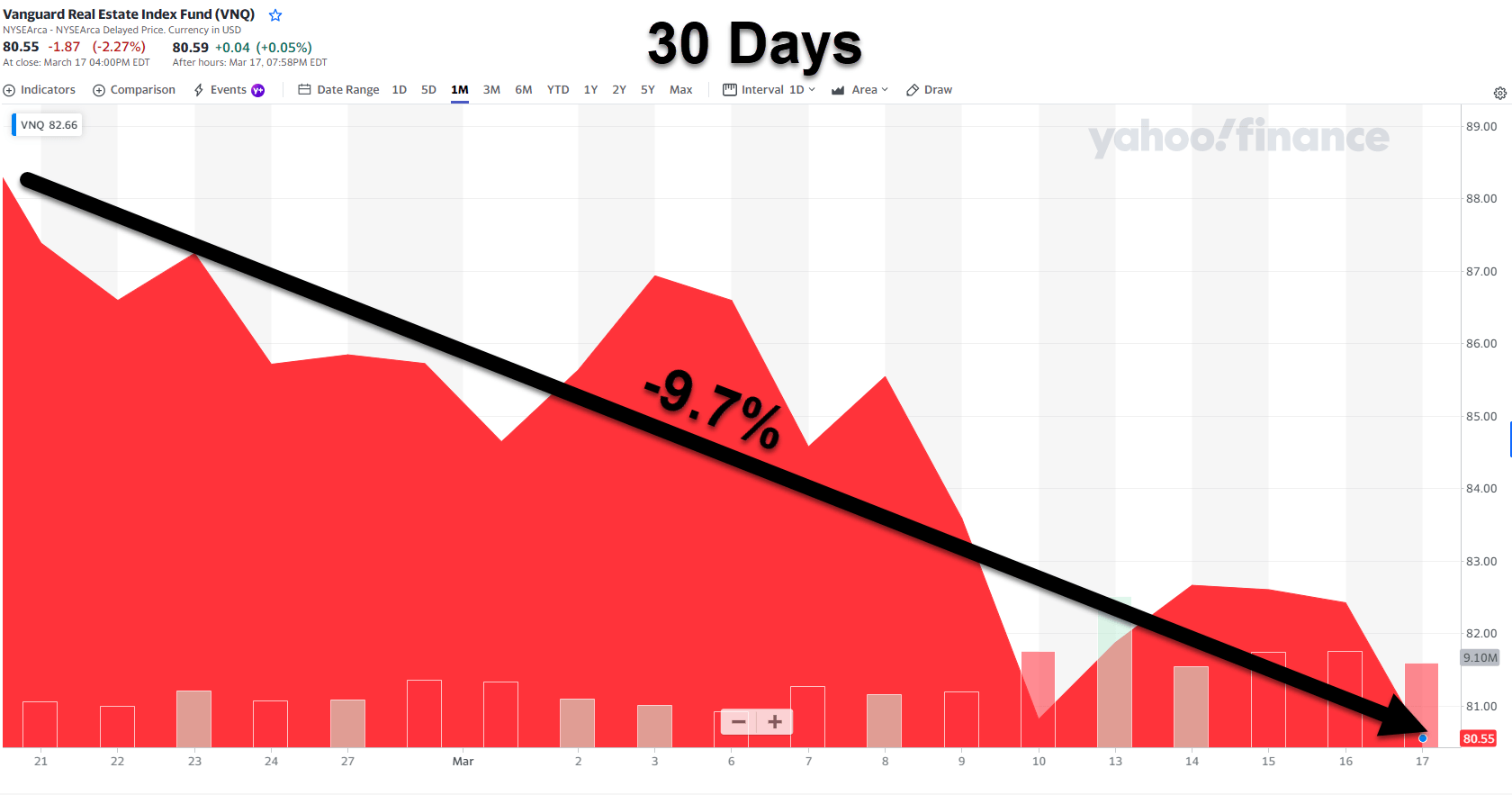

The NYSE is an exciting place and as a Wall Street writer I’m especially mesmerized by the flashing tickers, and boy oh boy, has there been a lot of red this month – shares in REITs are down a whopping 9.7%.

Yahoo Finance

Many fortunes have been made and lost on Wall Street…and as I pointed out in a recent article, I will make a retirement fortune by owning shares in high-quality dividend growth stocks. I’ll never forget what Frank J. Williams wrote in “If You Must Speculate, Learn The Rules”.

“The creed of the new speculator is: “I want to make a lot of money on little capital in a short time without working for it.” This is just as impossible in Wall Street as it is in any other place. “

I see so many people here on Seeking Alpha hoping to win the lottery by investing in high yield stocks. Afterall, as Williams explains,

“We are all gamblers at heart. We cannot be blamed for wanting to get at the best things in life in the quickest possible way. This is the spirit of America. The stock-market seems to offer the most rapid road to fortune.“

But Wall Street doesn’t have to be like a casino, where you put everything on black or red, and hope that you land on your magical pick. I love these words penned by Williams,

“If you are intelligent, the market will teach you caution and fortitude, sharpen your wits, and reduce your pride. If you are foolish and refuse to learn a lesson, it will ridicule you, laugh you to scorn, break you, and toss you to the rubbish-heap. The stock-market is cruel, but it is glorious, representing all that we admire in the American character, courage, vitality, forethought, vision, and enterprise.“

So today, I wanted to test your risk tolerance level (and mine) and provide you with three high-yielding REIT ideas, and I will warn you, not all of these are buy recommendations.

We always like to warn you of any dangerous picks, because we know the last thing you need is a dividend cut. A few days ago, I wrote that “the older I get, the wiser and more aggressive I get – when it comes to spotting deteriorating fundamentals that could lead to an ultimate dividend cut.”

Muck like Frank Williams I believe that “there is only one narrow trail leading to permanent success in the stock-market. Unless traders are prepared to climb that steep path with cautious steps, it would be better for them to stay out of Wall Street and to keep their money in the savings-bank.”

So, let’s get the high-yield party started…

Ares Commercial Real Estate: 14.4% Dividend Yield

Ares Commercial Real Estate (ACRE) is an externally managed mortgage real estate investment trust (“mREIT”) that originates and invests in commercial real estate loans.

Their debt products include senior mortgage loans, subordinate debt, mezzanine loans, preferred equity, and commercial mortgage-backed securities.

ACRE underwriting centers around the credit of the borrower, the collateral value, and the business plan related to the asset. ACRE generally holds its loans for investment and earns interest income.

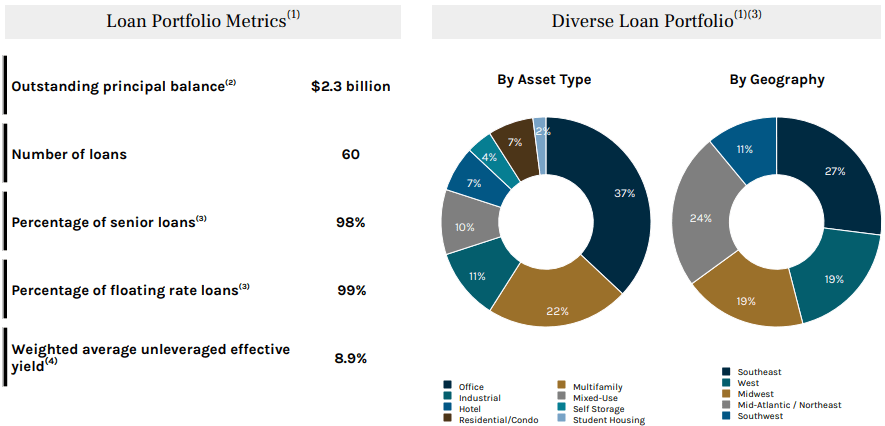

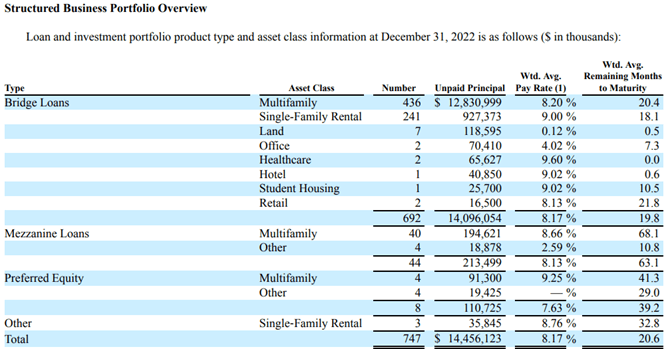

As of December 31, 2022, they had $352 billion of assets under management (“AUM”) and an outstanding principal balance of $2.3 billion. They have a total of 60 loans that are 98% senior loans and 99% floating rate loans with a weighted average unleveraged effective yield of 8.9%.

ACRE – Investor Presentation

As seen above, ACRE has debt investments across multiple property types including, office, industrial, hotel, multifamily, and others. Their largest property type is office at 37% followed by multifamily at 22%.

They are also diversified by geography with properties serving as collateral spread out evenly across the U.S. Their largest geographic concentration is in the Southeast at 27% and the Mid-Atlantic / Northeast region at 24%.

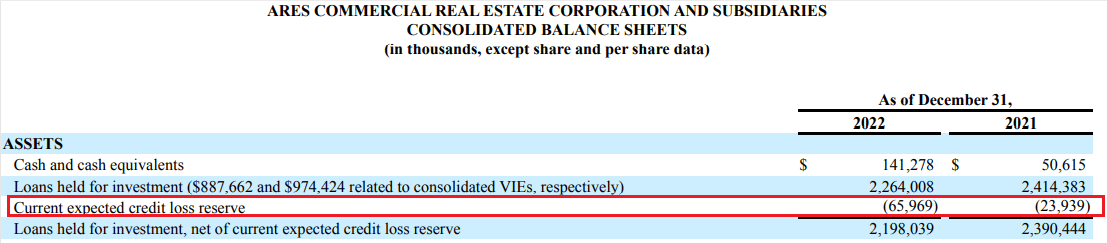

ACRE’s loans held for investment dropped by $150.4 million or 6.23% in 2022 when compared to the previous year. One thing to highlight is that their reserve for expected credit loss increased from $23.9 million in 2021 to $65.9 million in 2022, or an increase of approximately 175%.

ACRE – Form 10K

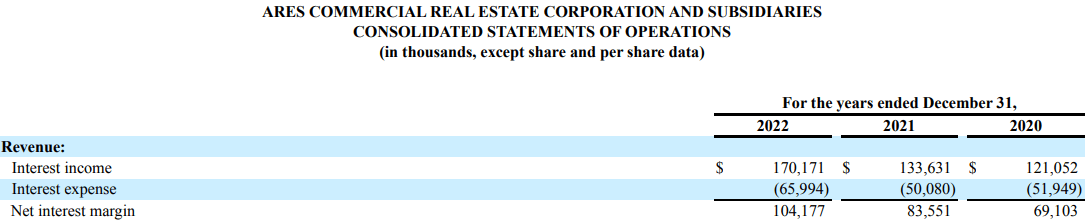

On a positive note, ACRE’s net interest income (“NII”) has been increasing over the last 3 years. From 2021 to 2022, NII increased from $83.5 million to $104.2 million for a year-over-year increase of 24.69%.

ACRE – Form 10K

ACRE has high debt levels with approximately $1.74 billion in total debt compared to total equity of approximately $747.5 million, making their debt-to-equity ratio 2.3x. When excluding the expected credit loss reserve their debt-to-equity ratio improves to 2.1x.

Additionally, their long-term debt to total capital is 69.91%. ACRE has approximately $216 million in liquidity consisting of $141 million in unrestricted cash and $75 million available to them under their secured funding agreements.

ACRE Investor Presentation

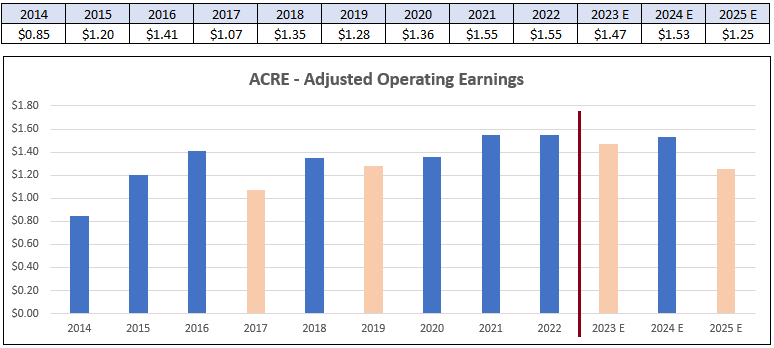

Ares Commercial Real Estate adjusted operating earnings have an overall upward trajectory, but earnings have been choppy since 2014. In 2017 earnings fell by -24% and in 2019 earnings fell by -5%. There was no earnings growth between 2021-2022. Analysts expect earnings to fall -5% in 2023, increase 4% in 2024, and then decline by -18% in 2025.

FAST Graphs (compiled by iREIT)

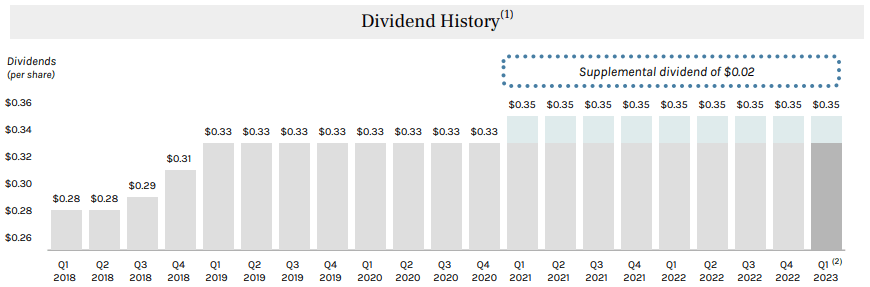

ACRE pays a 14.43% dividend yield and has paid steady dividends over the last several years but hasn’t increased its regular quarterly dividend since 2019. Since 2021, ACRE has paid a supplemental dividend of $0.02 making its total quarterly dividend payout $0.35 per share since the first quarter of 2021.

ACRE – Investor Presentation

The dividend has been covered by distributable earnings since 2018. In 2022 ACRE had distributable earnings of $1.55 and paid a dividend of $1.40 for a dividend payout ratio of 90.3% when based on distributable earnings.

ACRE Investor Presentation

While it’s encouraging that ACRE’s net interest income has increased over the last 3 years, that increase did not flow through to the bottom line as there was no increase in earnings or distributable earnings from 2021 to 2022.

Overall ACRE’s earnings are choppy, with growth in consecutive years, but sharp declines in other years. Analysts’ projections for future earnings also show an expected decline, especially in 2025 with an expected decline in earnings of -18%.

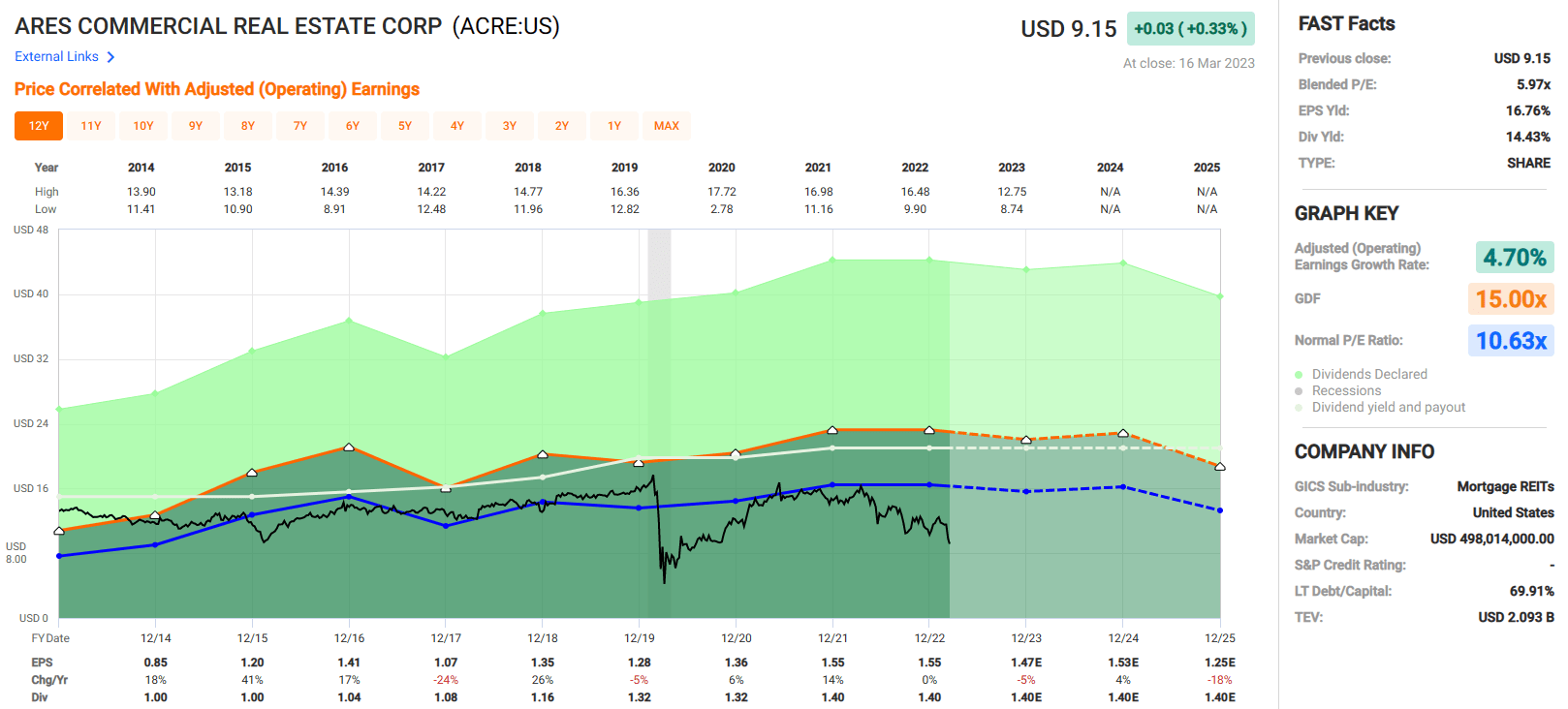

ACRE is trading at a significant discount with a P/E of 5.97x compared to their normal P/E of 10.63x, but dividend growth has been modest with an average annual increase of 3.90% over the last 9 years and if analysts’ projections hold up, ACRE’s earnings will not cover the dividend by 2025. At iREIT we rate ACRE a Tier 3 and are including it on our dividend watchlist.

FAST Graphs

Arbor Realty Trust: 13.7% Dividend Yield

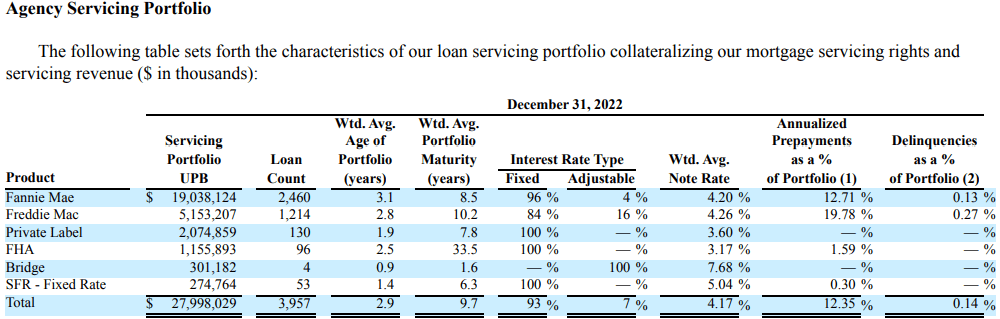

Arbor Realty Trust (ABR) is an internally managed mREIT that offers financing solutions for multifamily and commercial real estate. Their loan products include bridge loans, FHA multifamily loans, mezzanine and preferred equity and Fannie Mae / Freddie Mac loans.

Arbor operates through two business segments: Structured Loan Origination (Structured Business) and Agency Loan Origination (Agency Business). The bulk of their net interest income (“NII”) comes from their Structured Business with NII of $364.9 million compared to $25.8 million from their Agency Business. As a percentage, Arbor’s Structured Business makes up 93.39% of their total net interest income.

ABR – 10K

Through their Structured Business segment, Arbor mainly issues bridge loans for multifamily and single-family rental, and to a lesser extent other types of commercial real estate including office, healthcare, hotel, retail, and student housing.

Within their Structured Business segment, bridge loans makes up 692 out of 747 of their total loans. Bridge loans are typically short in nature and are often used to provide short term financing until the borrower can establish long-term funding. In addition to bridge loans, their Structured Business issues mezzanine loans and preferred equity for multifamily properties.

ABR – 10K

Through their Agency Business they originate, sell and service a variety of multifamily financial products through Government-Sponsored Enterprises (“GSEs”) like Fannie Mae and Freddie Mac. Within their Agency Business segment, the revenue generated is primarily through gains and fees from the origination and sale of mortgage loans.

Arbor is an approved Delegated Underwriting and Servicing (“DUS”) lender for Fannie Mae and has similar designations with multiple GSEs. Through their Agency Business they can originate and sell loans, or a portion of the originated loans to a GSE.

Loans issued under GSE and HUD programs are normally sold within 60 days from the origination date, while their private label loans are pooled together, securitized, and generally sold within 180 days of the origination date.

ABR – 10K

Through their two operating segments, combined net interest income came in at $390.8 million in 2022 for a 53.80% year-over-year increase.

ABR – 10K

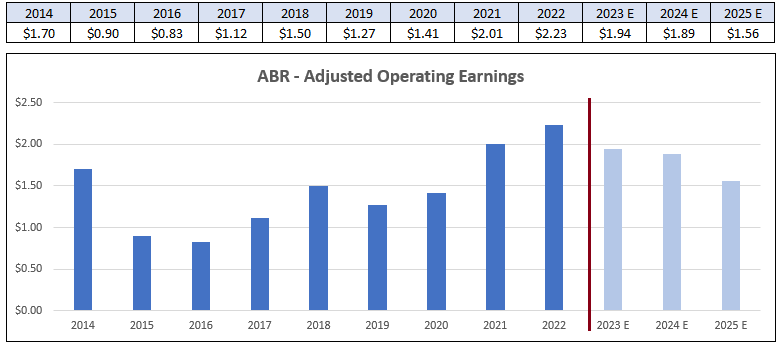

Arbor’s adjusted operating earnings have been mixed but have had an overall upward trajectory from 2015 to 2022. ABR’s earnings have increased 4 years in a row, but analysts expect earnings to decline over the next three years. Expectations for 2023 show a 13% decline in earnings, a decline of 3% in 2024 and a decline of 17% in 2025.

FAST Graphs – Compiled by iREIT

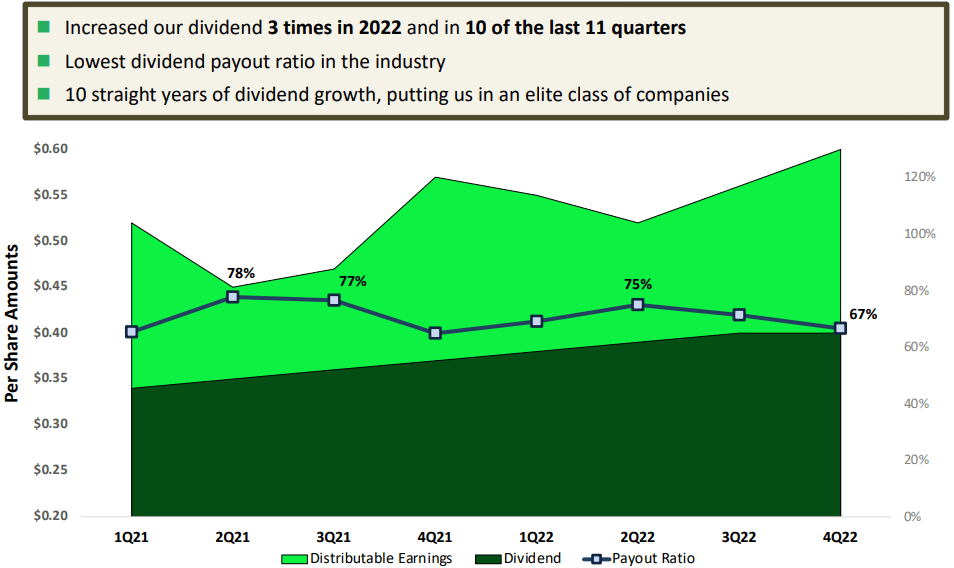

Arbor has an outstanding dividend track record with 10 consecutive years of increases, including 3 increases in 2022. They currently pay a 13.65% dividend yield that is well covered by their distributable earnings with a payout ratio of 67% as of the fourth quarter of 2022.

ABR has been consistent with its increases, but also has a compound dividend growth rate of 18.38% over the last 10 years.

ABR Investor Presentation

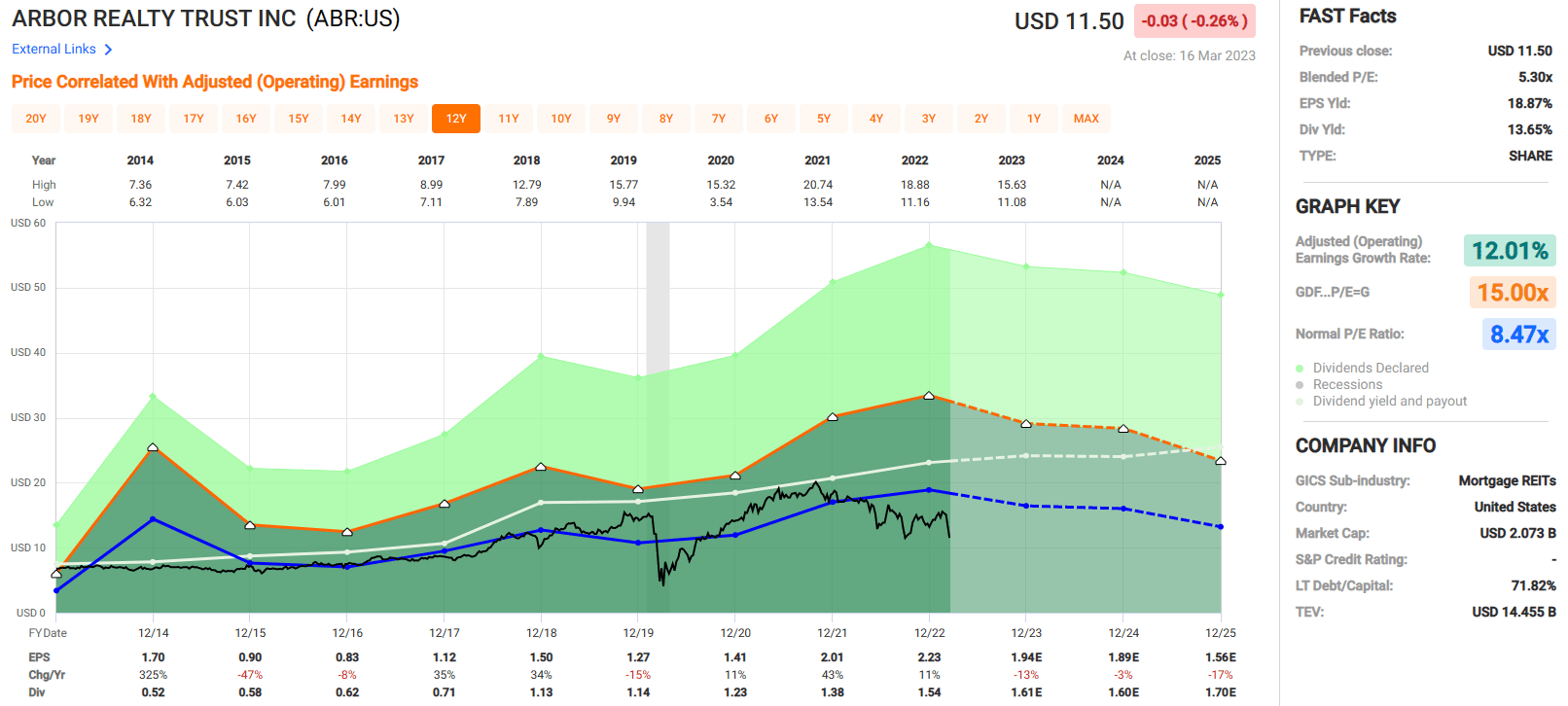

Arbor is currently trading at a P/E of 5.30x which is well below their normal P/E of 8.47x. Their adjusted operating earnings have declined at times over the last decade, but since 2014 they’ve had an adjusted operating earnings growth rate of 12.01%.

They pay a very high yield that is very well covered, especially when compared to industry norms, and have an impressive dividend growth rate over the past decade. At iREIT we rate Arbor Realty Trust Tier 2.

ABR was the subject of a “short and distort” attack this week from an unknown entity known as Ninji. It’s hard for us to take this short seller seriously and after speaking with ABR’s CFO earlier this week, I bought more shares.

In addition, ABR recently approved a share repurchase program authorizing the company to repurchase up to $50 million of its outstanding common stock. Finally, I thought that Armchair Income did a great job debunking the Ninji short seller.

FAST Graphs

KKR Real Estate Finance: 14.8% Dividend Yield

KKR Real Estate Finance Trust (KREF) is an externally managed mREIT that originates and acquires senior loans that are secured by commercial real estate. In addition to senior loans, they also offer mezzanine loans, preferred equity and other debt instruments.

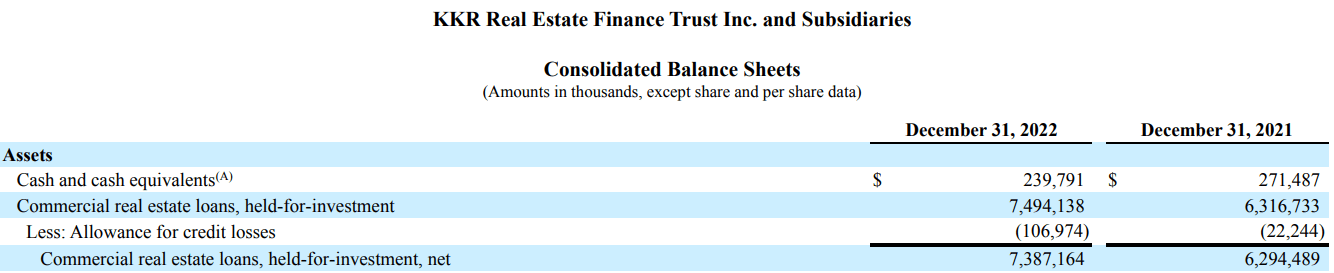

The company started in 2014 before going public in 2017 and as of the end of 2022 had a portfolio of loans totaling $7.9 billion. The majority of the loans in their portfolio consist of senior and mezzanine commercial real estate loans. Their stated investment objective is capital preservation and attractive returns to shareholders primarily through dividends.

KREF

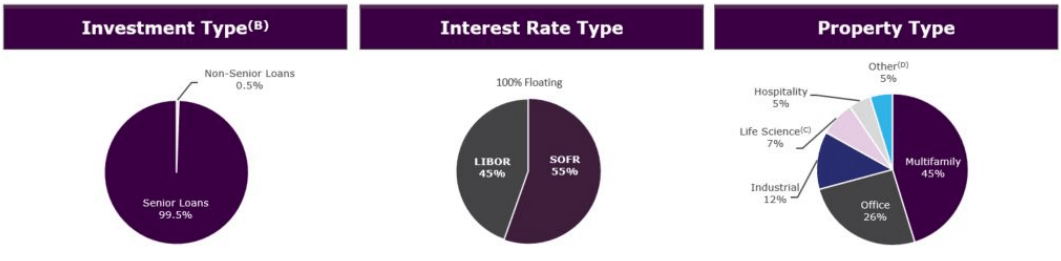

Their loan portfolio consists of 76 loans with a weighted average loan to value (“LTV”) of 66%. Senior loans makes up 99.5% of the loans in their portfolio and 100% of the loans are floating rate. Their average loan size is $123 million and 45% of their loans are for multifamily, followed by 26% for office, and 12% for industrial properties.

KREF – Form 10K

KREF’s loans held for investment increased from $6.3 billion in 2021 to $7.5 billion in 2022. Something to keep an eye on though is their allowance for credit losses. In 2022 it spiked up to $106.9 million, compared to $22.2 million in the previous year.

KREF – Form 10K

Net interest income has increased each year since 2020. It increased 16.66% from 2020 to 2021 and 12.30% from 2021 to 2022. While net interest income is the primary source of their revenue, the increase of 12.3% from 2021 to 2022 did not flow down to their distributable earnings.

KREF – Form 10K

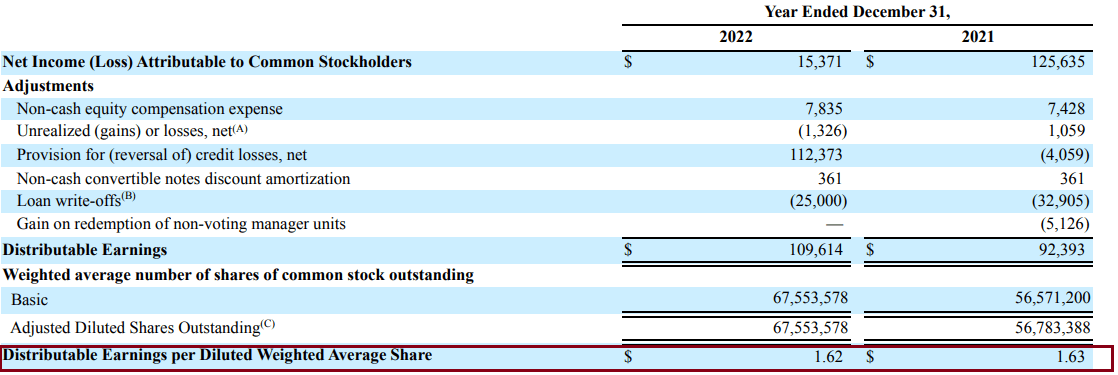

KREF’s distributable earnings decreased in 2022 by a penny. The disconnect between the increase in total revenue but the drop in distributable earnings is in large part due to the increased share dilution in 2022.

The weighted average diluted shares outstanding increased 18.97% from 2021 to 2022 so while revenue and distributable earnings increased in the aggregate, on a per share basis they did not.

KREF – Form 10K

Over the last 2 years KREF’s distributable earnings has not covered the dividend. They had a payout ratio of 105.52% in 2021 and 106.17% in 2022. Analysts expect earnings to come in at $1.95 per share in 2023 and the dividend to remain at $1.72. If analysts’ projections hold up, then it will bring KREF’s payout ratio below 90%, but as it now stands they are paying out more than they are earning.

KREF – Form 10K (compiled by iREIT)

KREF pays a dividend yield of 14.81% and is currently priced at a significant discount with a P/E of 6.88x compared to its normal P/E of 11.04x. While they’ve had mixed results in their operating earnings growth, they have an average growth rate of 3.03% since 2018.

My biggest concern is the high payout ratio. If analysts’ estimates are correct then KREF’s dividend should be fine. However, if KREF’s earnings fall short of expectations it may put the dividend in jeopardy. We think there is potential here, given the steep discount in price and high yield, but we are monitoring the payout ratio closely. At iREIT we rate KKR Real Estate Finance Trust Tier 2 and is on our dividend watch list.

FAST Graphs

In Closing…

To be perfectly clear, a REIT that yields 10% almost always means that investors perceive very low growth, or even worse, a potential dividend cut. And of course, all three of three of the above-referenced mREITs are yielding higher than that – averaging a whopping 14.3%.

At iREIT on Alpha, our focus is fundamental analysis, and this means that we must always pay very close attention to the earnings stream that these companies generate and of course, the sources of revenue is extremely important.

Chasing yield is dangerous and I would encourage all readers to maintain responsible diversification. As Frank Williams wrote,

“The average small trader takes a flyer in the market without forethought, on the theory that if he loses, he is not much out. Gambling in stocks in this happy-go-lucky, hit-or-miss style used by hundreds of thousands is a hopeless waste of time and money.”

Our readers have asked us to analyze these three REITs, and now it’s up to you to decide if “the thrill of victory is worth the agony of defeat.”

No SWANS today folks…just high yield!

Author’s note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.